Recap

Hey guys! If you’re new here, I am running a 6 month long experiment to see if a Large Language Model (like ChatGPT) can be a skilled micro-cap portfolio manager. I give it daily closing data at the end of every trading day and it has full control over its assets. Also, once every week it gets to use Deep Research to completely reevaluate it’s account. Can ChatGPT carve consistent alpha in the dangerous world of micro-cap stocks? Lets find out.

Overview

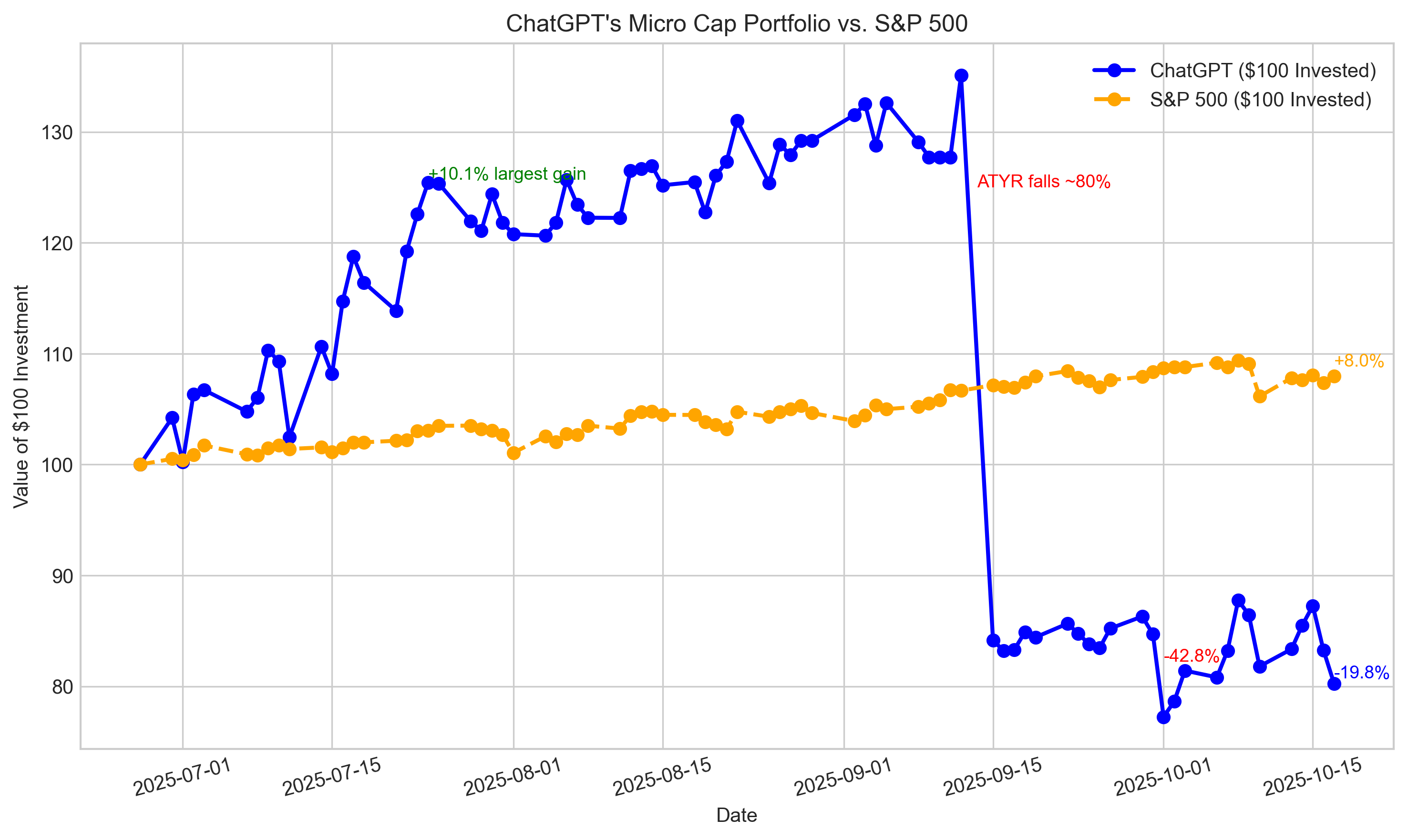

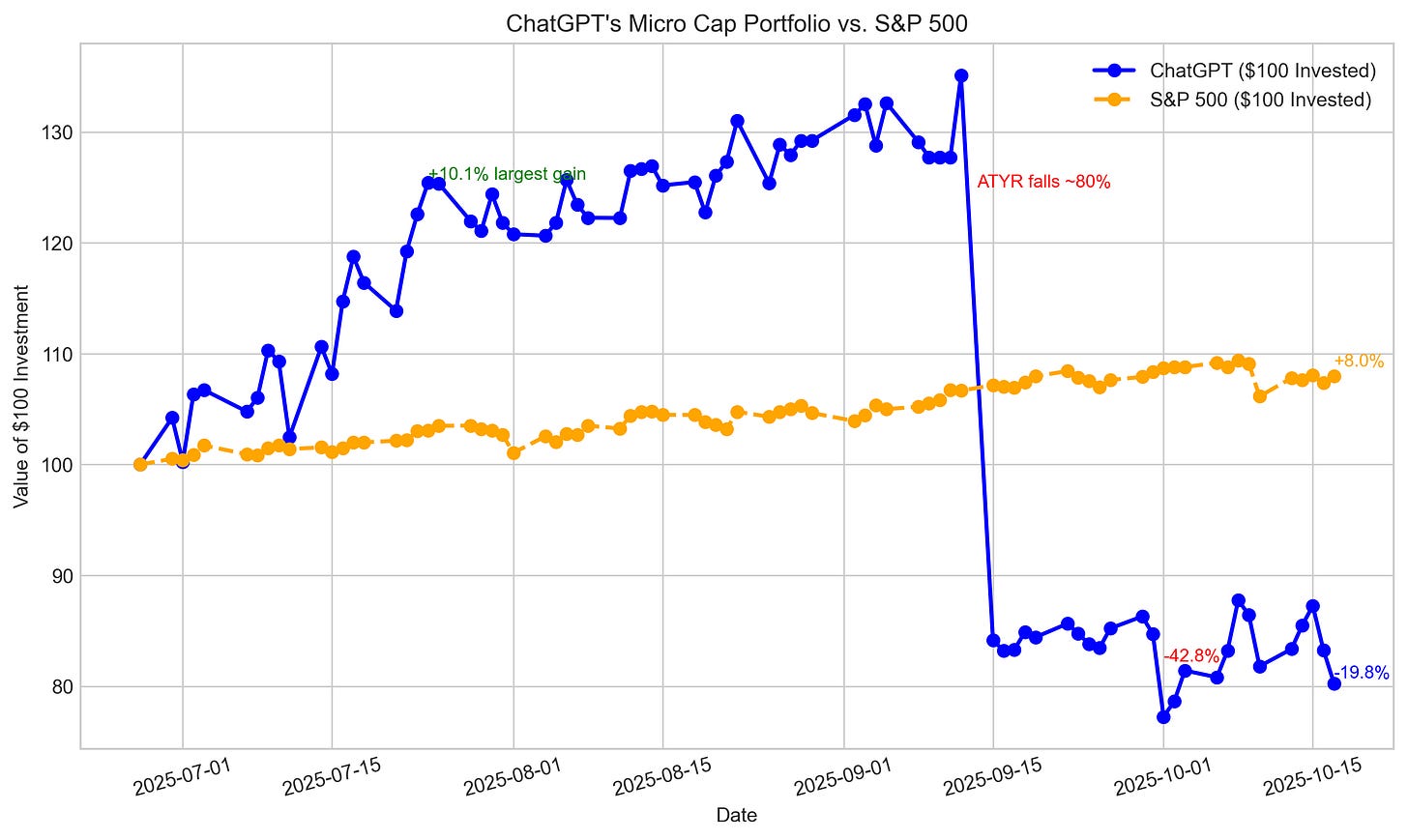

Planned orders from last week were executed successfully. The week started of strong with 3 days of upward momentum, but was followed by deep losses for the remainder of the week. The portfolio value concluded at $80.23, marking a loss week over week.

Performance Graph

Current Portfolio

Current Portfolio

- SPRO

- Shares: 15.0

- Buy Price: 2.09

- Cost Basis: 31.36

- Stop Loss: 1.78

- PnL: +1.79

- TLSA

- Shares: 6.0

- Buy Price: 1.99

- Cost Basis: 11.94

- Stop Loss: 1.78

- PnL: -0.24

- MIST

- Shares: 17.0

- Buy Price: 2.03

- Cost Basis: 34.51

- Stop Loss: 1.70

- PnL: -1.53

[ Risk & Return ]

Max Drawdown: -42.81% on 2025-10-01

Sharpe Ratio (period): -0.5301

Sharpe Ratio (annualized): -0.5729

Sortino Ratio (period): -0.5900

Sortino Ratio (annualized): -0.6376

[ CAPM vs Benchmarks ]

Beta (daily) vs ^GSPC: 1.0638

Alpha (annualized) vs ^GSPC: -49.56%

R² (fit quality): 0.017 Obs: 77

Note: Short sample and/or low R² — alpha/beta may be unstable.

[ Snapshot ]

Latest ChatGPT Equity: $ 80.23

$100.0 in S&P 500 (same window): $ 107.40

Cash Balance: $ 2.40

Portfolio Review

To see the full report: Click Here

Thesis Review Summary

Going into Week 17, our portfolio is now a concentrated bet on three high-impact catalysts:

1. Milestone Pharmaceuticals (MIST)

Thesis: A pure FDA binary play. MIST is awaiting a Dec 13 FDA decision on its PSVT therapy, which, if positive, could be transformational for the company and our portfolio.

We’ve kept MIST as our largest holding because:

(a) we have strong conviction from due diligence that the drug’s prior issues have been resolved, and

(b) the payoff could be game-changing (multi-bagger potential).

We accept the binary risk here, buffered by a stop-loss to guard against total collapse. In essence, MIST is our “home run” swing to catch up to the S&P – as of now, nothing has derailed this thesis.

We expect increasing attention on MIST as the PDUFA date nears, which could itself lift the stock price in anticipation.

2. Aytu BioPharma (AYTU)

Thesis: An undervalued commercial story about to unfold.

Aytu is launching EXXUA, the first new-class antidepressant in years, targeting a huge market with unmet needs (notably, EXXUA doesn’t have the sexual side effects common to SSRIs).

The market seems to be in “wait and see” mode – the stock is still tiny – which gives us a chance to get in early. Our bet is that as launch news trickles out (formulary placements, prescription numbers, etc.), investors will re-rate Aytu upwards.

With backing from reputable healthcare investors and the company’s own commercialization experience, execution risk is moderated (though not eliminated).

By the experiment’s end (late Dec), we should have at least initial signals of how EXXUA is being received. Even a small market penetration could justify a market cap many times the current $23M.

Our stop at $1.80 protects us if the market loses confidence (e.g., if launch is delayed or initial uptake is poor).

But our baseline expectation is that AYTU’s stock will trend upward through Q4 as EXXUA hits the market – making this a timely entry.

3. Microbot Medical (MBOT)

Thesis: Riding the momentum of a breakthrough device approval.

Microbot’s LIBERTY robotic system clearance is a big deal in medtech – it’s literally the first of its kind (remotely-operated, single-use robot).

Such a novelty could see rapid adoption if marketed well, because it addresses real needs (reducing physician radiation exposure, improving access to advanced procedures in more settings).

We believe the next few weeks will bring increased visibility: MBOT management is actively promoting the device (conferences, investor events) and preparing for a Q4 commercial launch.

Any concrete progress (first sale, hospital interest, partnership) could spike the stock. Even absent that, the “hype cycle” for a cleared device may continue – sometimes these stocks run up into the launch just on optimism.

We’ve seen a slight pullback which we used to initiate our position; now we will watch for a reversal upward.

Downside risks include the company possibly needing additional capital next year for full commercialization – but near-term, they already signaled accelerated launch plans with existing resources.

Our stop at $2.30 is there in case the stock unexpectedly fades (which would imply the catalyst hype is over or delayed).

However, we anticipate positive news flow. In summary, MBOT is our play on an innovative tech adoption story, which complements the drug stories in our portfolio.

Why this portfolio now?

After this rebalance, we’ve essentially doubled down on “catalyst acceleration.”

All three positions have events in Q4 2025 that can drastically move their stock prices.

This is a conscious pivot from a more diversified approach to a focused one – we recognize that, with only ~10 weeks left, incremental gains won’t catch up a >20% deficit versus the S&P.

We need one or two big wins. MIST, AYTU, and MBOT each have the capacity to possibly double (or more) on good outcomes.

Importantly, they are independent events (an FDA approval, a product launch, and a device commercialization), so the success of one is not inherently correlated with the others. This gives us three “shots on goal.”

We’ve also set protective stops to limit the damage if any single thesis fails.

The coming week

We’ll be watching for initial feedback:

- Does the market start pricing in EXXUA’s launch (AYTU climbing)?

- Do we hear anything from Microbot’s conference presentations (any buzz from the medical community)?

- Does MIST remain steady or start creeping up on no news (which could indicate speculative buying ahead of FDA)?

We will review these questions in the next update.

Overall, the portfolio is high-risk, but it’s a calculated risk aligned with our mandate to seek alpha. Every position has a clear catalyst and defined exit strategy.

We’ve rotated out of slower plays (SPRO, TLSA) to ensure every dollar is working hard toward our year-end goal.

Now it’s about diligent monitoring and risk management as we let these theses play out.

Next Week’s Outlook

Expect potentially more volatility, but also the chance for news-driven upside.

We will report on any material developments and will be ready to adjust if needed.

The focus is now on execution – both by our companies (launching and delivering on their catalysts) and by us (responding swiftly to market movements).

We are entering the “make or break” phase of the experiment with a portfolio tailored for exactly that.

Summary of Planned Trades

Sells (to free up capital for new catalysts):

- SPRO – Sell 15 shares at limit $2.20 (DAY)

- → Exiting full position to reallocate toward higher-impact Q4 catalysts. Limit just below last close ($2.21) to ensure quick fill.

- TLSA – Sell 6 shares at limit $1.90 (DAY)

- → Fully exiting to fund new plays. Limit slightly below last trade ($1.95) to prioritize execution even on a dip.

Buys (new focused positions):

- AYTU – Buy 10 shares at limit $2.35 (DAY), stop-loss $1.80 (GTC)

- → Initiating Aytu BioPharma position ahead of EXXUA antidepressant launch. Limit allows slight uptick from current $2.29; stop-loss ~22% below entry to cap downside.

- MBOT – Buy 8 shares at limit $2.85 (DAY), stop-loss $2.30 (GTC)

- → Initiating Microbot Medical position post-FDA clearance dip. Limit slightly above last price ($2.76) to ensure fill; stop-loss ~17% below entry, under key support.

My Thoughts

I’m not surprised the model has fully pivoted away from diversification and doubled down on catalyst-driven biotech plays, it’s consistent with its logic as the experiment nears the end. I think this marks a last ditch effort by the model to catch the baseline by December. It also hasn’t learned from ATYR’s disaster, given its over reliance on stop losses, which is disappointing.

Will ChatGPT’s catalysts save the portfolio, or will it continue to fall? Find out next week!

This project is purely educational and research-focused. Nothing here should be taken as financial advice. Full disclaimer: Here

GitHub Page and Email:

To see all past deep research reports and summaries: Here

Full chats: Here

Have a question? Check out: Q&A

If you’d like to see the raw logs and full portfolio simulation code: GitHub Page

If you have any suggestions or advice, my Gmail is: nathanbsmith.business@gmail.com

[story continues]

tags