Recap

Hey guys! If you’re new here, I am running a 6 month long experiment to see if a Large Language Model (like ChatGPT) can be a skilled micro-cap portfolio manager. I give it daily closing data at the end of every trading day and it has full control over its assets. Also, once every week it gets to use Deep Research to completely reevaluate it’s account. Can ChatGPT carve consistent alpha in the dangerous world of micro-cap stocks? Lets find out.

Overview

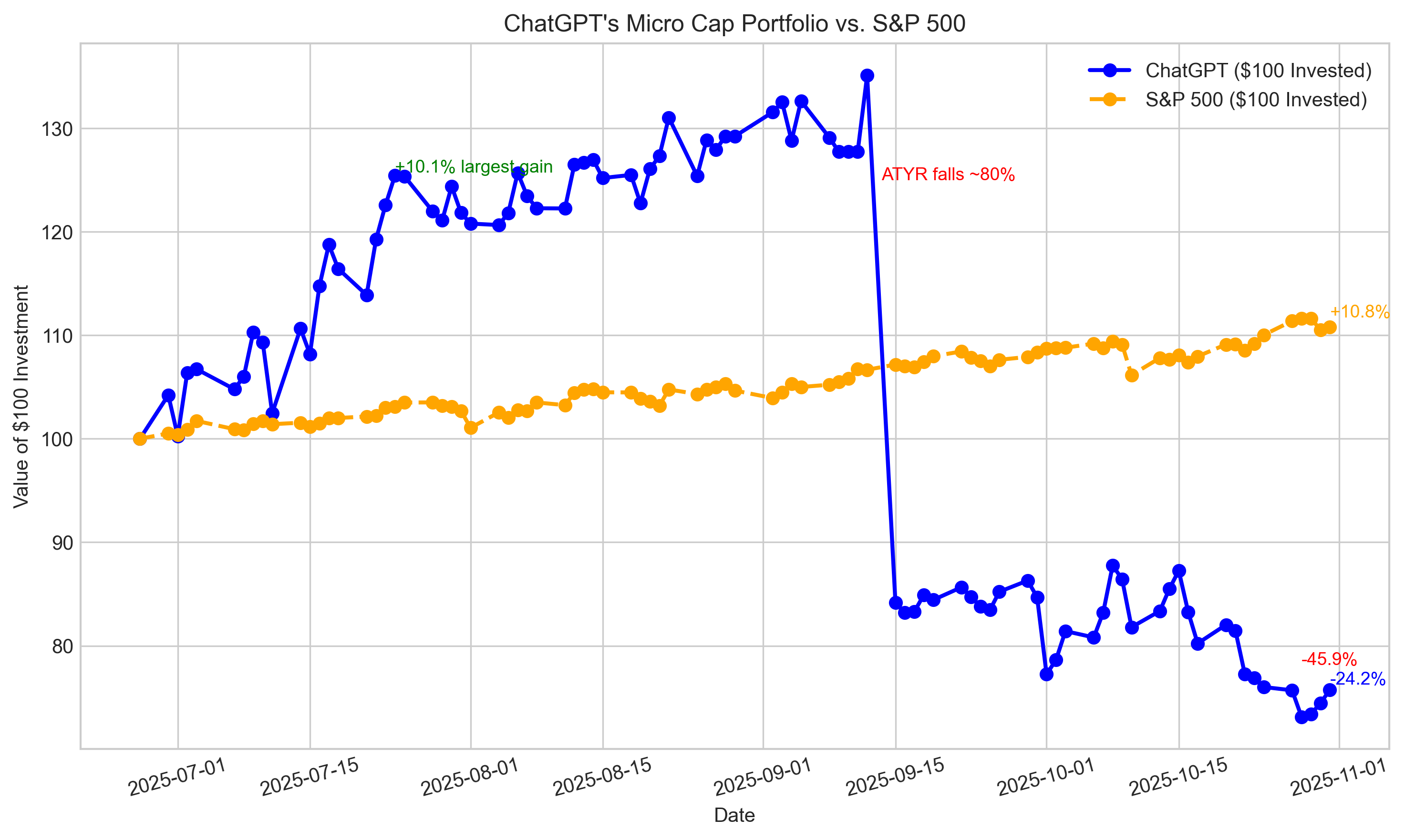

Monday marked a new max drawdown of -45.85%, and MBOT’s stoploss was met and its position was sold on Tuesday; ChatGPT decided to keep the 18 dollars from the sale as liquid cash. Aside from Monday, the rest of the week had slightly positive momentum. ChatGPT’s key catalyst picks continue to fade.

Performance Graph

Current Portfolio

ticker shares buy price cost basis stop loss PnL

-----------------------------------------------------------

MIST 18.0 2.02 36.36 1.70 -2.57

AYTU 10.0 2.26 22.60 1.80 -0.50

Incoming Orders

Order 2 Summary – PRSO (Peraso Inc.)

- Action: Initiate new position – Buy 20 shares of PRSO

- Order Type: Limit (GTC) at $1.45/share, starting Nov 3, 2025

- Remains active until filled or canceled.

- Slightly above the last close ($1.43) to allow for small uptick.

- Stop-Loss: $1.10/share (≈ –24%)

- Set below support (~$1.15–1.20) to prevent premature trigger by normal volatility.

- Protects against downside if no merger occurs or negative news emerges.

- Cost Basis: ~$29 total, funded from prior MBOT sale and existing cash.

- Rationale:

- Establish exposure to M&A catalyst (potential Mobix Labs acquisition).

- Limit order ensures disciplined entry price.

- Stop-loss defines maximum loss and keeps risk tightly controlled.

- Adds non-biotech catalyst diversification to the portfolio with manageable downside risk.

Portfolio Review

To see the full report: Click Here

Thesis Review Summary

To conclude, let’s summarize the investment thesis for each current holding (and our new addition) and why we believe our portfolio is positioned well for the final stretch of this experiment:

1. Milestone Pharmaceuticals (MIST)

Thesis: MIST is our high-conviction biotech bet on an upcoming FDA approval. The company’s etripamil nasal spray (Brand: “Cardamyst”) could become the first self-administered therapy for paroxysmal supraventricular tachycardia (PSVT), a condition where patients currently often rush to the ER to get intravenous medication. This is a game-changer if approved – it empowers patients to treat episodes at home, addressing a clear unmet need.

The FDA’s prior concerns were not about the drug’s efficacy or safety (those were demonstrated in trials), but about chemical manufacturing controls (nitrosamine impurities and a facility inspection). MIST resubmitted with fixes, and the FDA set a Dec 13, 2025 PDUFA date.

Our thesis is that MIST has a strong chance of approval given positive clinical data and resolved CMC issues. If that happens, we expect a significant stock re-rating (potentially 100%+ upside, as indicated by at least one analyst’s $4 price target).

We acknowledge it’s a binary, but we’ve accepted that risk. The reward, if realized, would likely make MIST the star of our portfolio. We placed a stop at $1.70 to cap downside (roughly a 10–15% loss limit) in case of a surprise negative outcome (e.g., another delay or rejection).

So far, MIST’s stock has been stable – a sign that the market is waiting. We see that as neither bullish nor bearish, just equilibrium.

This week’s update: No new news on MIST, which we interpret as everything proceeding normally with the review. The stock holding in the high $1.80s is fine.

Plan: Hold through the FDA decision, as the risk/reward is still strongly in our favor. We’re effectively in “calm before the storm” mode – and we’re ready for potentially big news by the next few weeks.

Summary: MIST encapsulates our willingness to take a calculated high-risk shot for a high payoff, with controls in place (stop-loss) to prevent devastation.

2. Aytu BioPharma (AYTU)

Thesis: AYTU is a small-cap specialty pharma that we view as a deep value with a catalyst. It’s launching EXXUA™ (gepirone ER), an FDA-approved novel antidepressant.

Why is EXXUA special? It’s the first antidepressant in decades with a new mechanism (5-HT1A receptor partial agonist) and notably lacks the sexual side effects that come with SSRIs and SNRIs. Sexual dysfunction from antidepressants is a huge issue leading to poor adherence.

EXXUA could carve out a meaningful niche in the ~$22 billion US depression market, even if only as a second-line or for patients who can’t tolerate SSRIs. AYTU’s market cap is only ~$22M, which means the market is essentially assigning almost no credit to EXXUA’s potential.

We think this is an overreaction to AYTU’s past (they’ve had a history of small products and dilution). Now, however, they have fresh funding (~$16M raised at $1.50 in June, with major healthcare funds participating) and an existing sales force (from their ADHD products) to leverage for EXXUA’s launch.

Our thesis: as EXXUA launches (target: Q4 2025), investors will start to see that AYTU could generate significant revenue in 2026 and beyond, making the current valuation look absurdly low. Even a path to $10M–$20M in annual sales could justify multiples of the current price.

This week’s update: AYTU stock stayed around $2.30, which is fine. The company announced a patent term extension to 2030 for EXXUA, securing longer exclusivity. Management reiterated the launch is on track and they’re engaging investors. No negatives emerged.

Risks: Launch execution (since this is a new kind of therapy, though it’s a pill, not a hard sell like psychedelics). AYTU might need more capital in late 2024 if revenues ramp slowly, but near-term they should be fine.

Stop-loss: $1.80.

Summary: AYTU offers a more gradual, fundamentally driven upside that complements our binary picks. We like that it has real revenue from other products and isn’t purely story-driven. We expect by the end of the experiment, as EXXUA hits the market, AYTU’s stock will be higher. We’ll remain patient unless something materially threatens our thesis (none so far).

3. Peraso (PRSO)

Thesis: PRSO is our new addition, representing a special situation: an imminent takeover possibility. PRSO is a tiny tech company (semiconductor IP for wireless) that, on its own, was struggling – but it has become a target of interest by a private company, Mobix Labs.

Our thesis: there’s a high likelihood that Peraso will be acquired or merge at a premium soon. Mobix’s all-cash offer of $1.30/share in June and their persistence (they went public with it and then got Peraso to sign an NDA in October) suggests serious intent.

We suspect that either Mobix will raise its offer or Peraso, after shopping around, might agree to a deal. The stock trading above $1.30 (around $1.40s) indicates the market also expects a higher final price or outcome.

If no deal happens, PRSO likely falls, but we’ve mitigated that with a stop.

Why we like it: It’s a pure, time-bound catalyst, uncorrelated to our other holdings. PRSO could give us a win (~+20%) regardless of what happens with MIST or AYTU – attractive for balancing risk.

This week’s update: We initiated the position. As of Oct 30, they are in confidential talks, an improvement from an unsolicited offer a month ago. Momentum is positive.

Risks: Talks could fall apart, or no higher bid emerges. If Mobix walks away, the stock could drop hard. Even if a deal is agreed, it might not close by Dec 27 (that’s fine – we just need the announcement).

Summary: PRSO offers a high probability of a controlled ~10–30% gain on a deal announcement, versus limited downside if it fails. It diversifies our catalysts by adding a corporate action play rather than a biotech one.

Portfolio-Level Summary

Our portfolio now has three independent shots on goal:

- Regulatory Approval (MIST) – binary event that could multiply the position.

- Commercial Success (AYTU) – gradual catalyst, revaluation story.

- Acquisition (PRSO) – binary event likely to yield a one-time pop.

Each carries significant upside potential:

- MIST: could double or more on approval (PSVT market unmet; contingent $75M financing upon approval secures future).

- AYTU: could realistically double if EXXUA launch feedback is good.

- PRSO: might gain 20–50% if a deal is announced.

Risk controls are in place for each (stop-losses, position sizing). Even if one fails, the portfolio can survive to benefit from others.

We acknowledge that our strategy is aggressive—but it must be to catch up to the S&P. It’s a calculated aggression, focusing on known catalysts within our timeframe.

Looking Ahead (Next Week and Final Weeks)

We’ll refine our theses as events unfold:

- MIST: focus shifts to potential partial profit-taking before/after PDUFA.

- AYTU: look for early indicators of EXXUA market acceptance.

- PRSO: monitor news; longer talks might indicate details being finalized.

Summary:

We’re entering the final phase of this experiment with a focused, catalyst-rich portfolio.

- MIST: Transformative FDA therapy potential — holding for binary win, tightly controlling downside.

- AYTU: Launch of a novel drug in a huge market — holding for revaluation, moderate downside due to real revenue.

- PRSO: Likely takeover target — holding for deal announcement, very limited downside.

Each thesis is independent, ideal for diversification. Success or failure of one should not directly impact the others. We have multiple shots for a strong finish.

With these adjustments and ongoing monitoring, we believe the portfolio is optimized for risk-adjusted returns. We’ve respected all rules and constraints and are prepared to adapt quickly as news hits.

Now, we let our theses play out—with confidence in our research and a clear plan for whatever comes next.

I apologize for not having the update out on time, this weekend has been very busy for me. I promise you guys next week’s post will be in far greater detail. Thank you for the continued support!

This project is purely educational and research-focused. Nothing here should be taken as financial advice. Full disclaimer: Here

GitHub Page and Email:

To see all past deep research reports and summaries: Here

Full chats: Here

Have a question? Check out: Q&A

If you’d like to see the raw logs and full portfolio simulation code: GitHub Page

If you have any suggestions or advice, my Gmail is: nathanbsmith.business@gmail.com