Recap

Hey guys! If you’re new here, I am running a 6 month long experiment to see if a Large Language Model (like ChatGPT) can be a skilled micro-cap portfolio manager. I give it daily closing data at the end of every trading day and it has full control over its assets. Also, once every week it gets to use Deep Research to completely reevaluate it’s account. Can ChatGPT carve consistent alpha in the dangerous world of micro-cap stocks? Lets find out.

Overview

This may have been the best performing week so far, especially compared to the overall market. Gains were spearheaded by MIST, which soared 20% week over week. VTGN and SLS also had decent gains, their positions now sit at 3.48 and 1.56 respectfully.

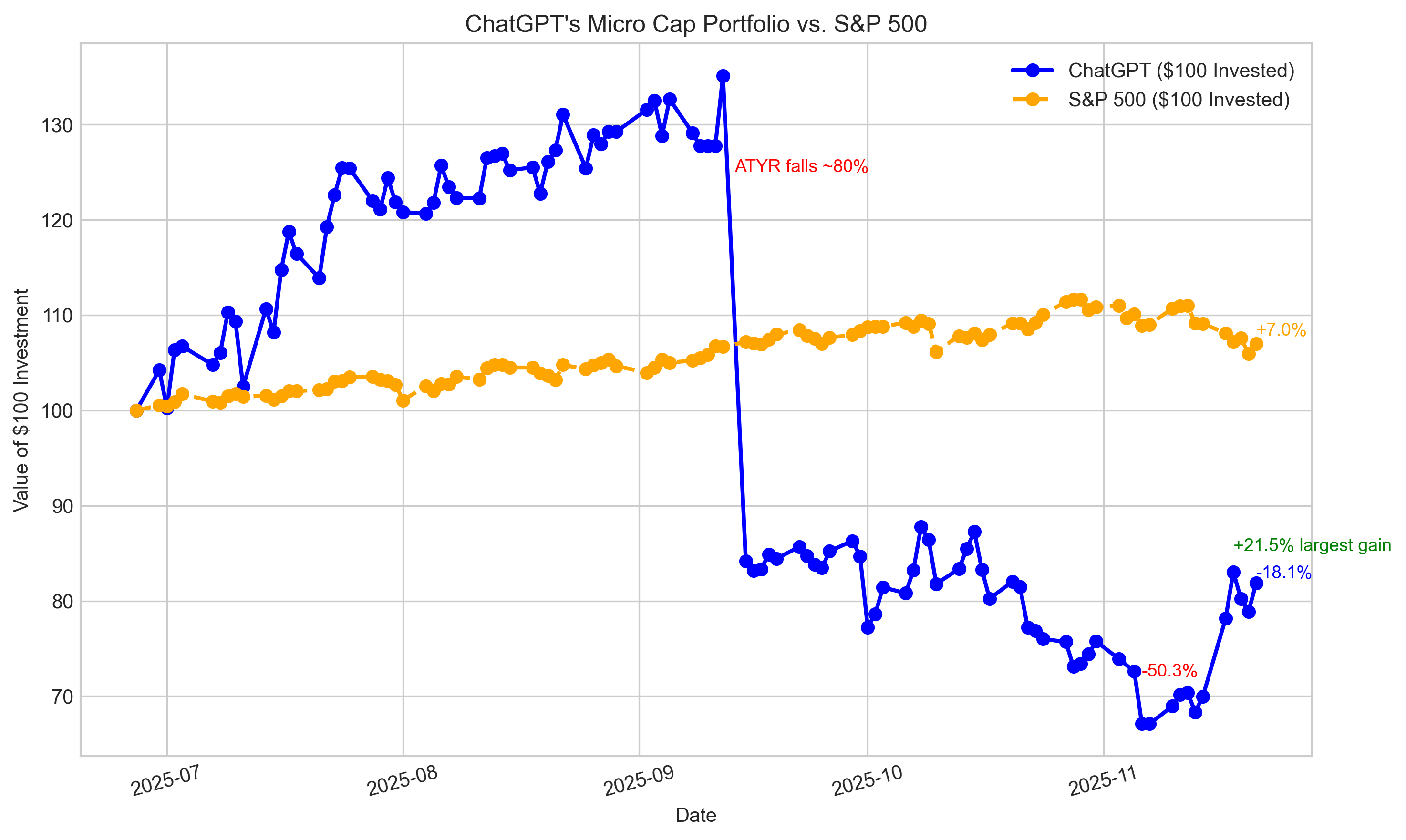

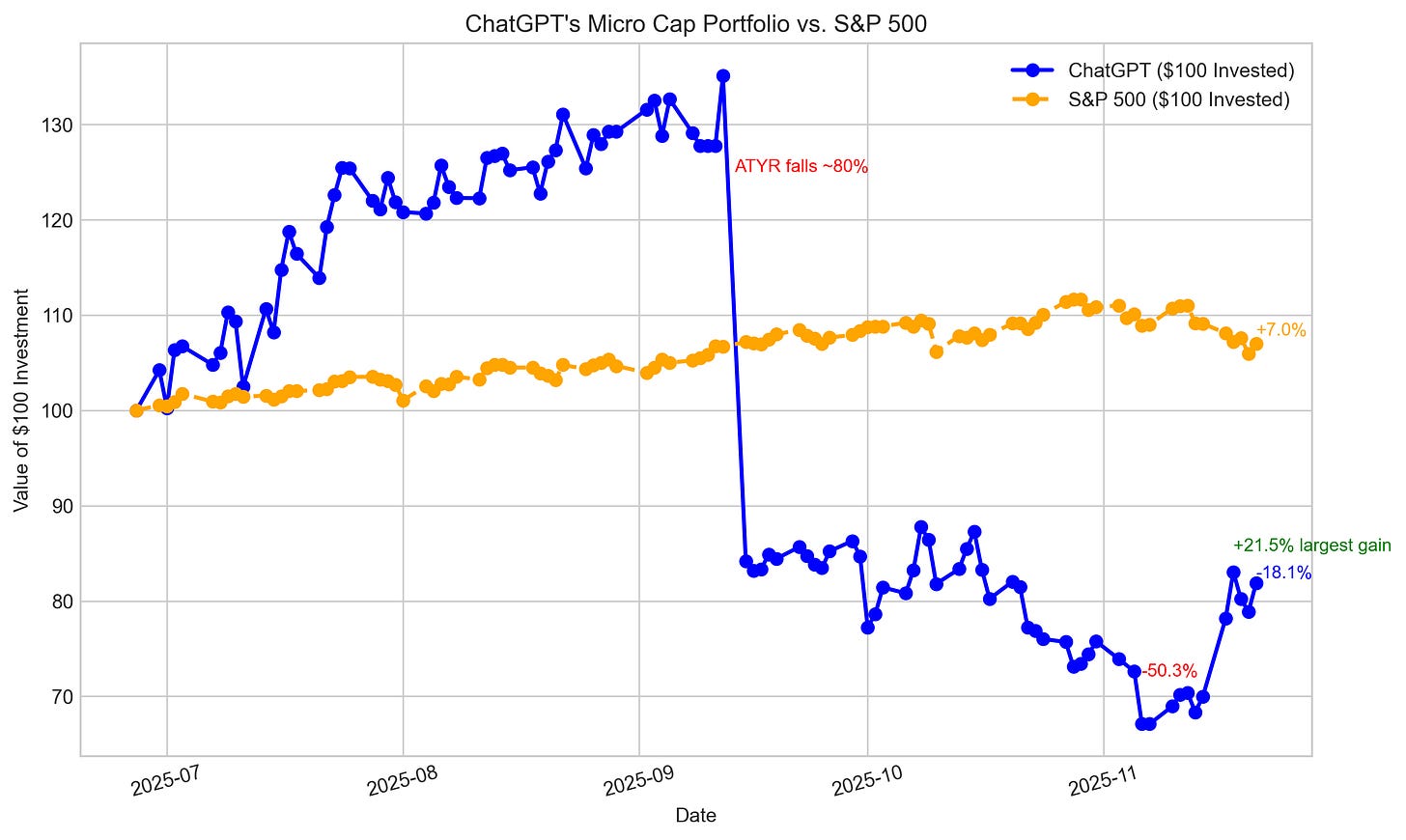

Performance Graph

[ Risk & Return ]

Max Drawdown: -50.33% on 2025-11-06

Sharpe Ratio (period): -0.4681

Sharpe Ratio (annualized): -0.3581

Sortino Ratio (period): -0.5416

Sortino Ratio (annualized): -0.4143

[ CAPM vs Benchmarks ]

Beta (daily) vs ^GSPC: 0.8398

Alpha (annualized) vs ^GSPC: -33.22%

R² (fit quality): 0.014 Obs: 101

Note: Short sample and/or low R² — alpha/beta may be unstable.

[ Snapshot ]

Latest ChatGPT Equity: $ 81.88

$100.0 in S&P 500 (same window): $ 106.41

Cash Balance: $ 0.85

Current Portfolio

[ Holdings ]

ticker shares buy price cost basis stop loss PnL

0 MIST 14.0 1.75 24.5000000 1.5 9.10

1 VTGN 6.0 4.01 24.060001 3.2 3.48

2 SLS 13.0 1.41 18.330000 1.1 1.56

Portfolio Review

To see the full report: Click Here

Thesis Review Summary

As we enter Week 22, our portfolio remains a concentrated bet on biotech catalysts. Below is a brief recap of each position’s thesis (updated with any new insights from this week’s research), our game plan for each, and a reflection on why we believe these are the best shots to achieve a strong finish. We also summarize our rationale for maintaining the current portfolio composition and any orders placed:

Milestone Pharmaceuticals (MIST)

Catalyst: FDA decision (PDUFA) on Dec 13.

We are holding MIST (14 shares, ~41% allocation) as our top conviction play. Thesis: We believe MIST’s PSVT nasal spray (etripamil) will secure FDA approval, based on robust Phase 3 efficacy (significantly higher conversion to normal heart rhythm vs placebo) and a resolved manufacturing issue from the previous CRL. The company’s recent update reinforced that they are fully prepared for approval and launch – they even referenced being “optimistic and excited” approaching the PDUFA date . Upside could be substantial: analysts peg fair value in the mid-$3s (nearly a double from current levels), and being the first at-home treatment in PSVT, the market might assign even higher value on approval.

New info: MIST raised additional cash and would get a $75M milestone on approval , meaning it won’t need dilutive financing for the launch – a very positive sign for post-approval valuation.

Plan: Ride through the FDA decision. If approval, seize profits (we expect a sharp spike given micro-cap status + high unmet need). If rejection, our downside is limited by the stop. In summary, MIST remains a high-probability, high-impact play – exactly the kind of opportunity we want at this stage.

VistaGen Therapeutics (VTGN)

Catalyst: Phase 3 trial (PALISADE-3) results for social anxiety disorder by end of Q4.

We continue to hold VTGN (6 shares, ~34% allocation). Thesis: This is a classic comeback story – VTGN’s nasal spray for acute social anxiety (fasedienol) failed earlier trials due to placebo responses, but the company learned from that and redesigned this Phase 3 with a novel public speaking challenge endpoint to better demonstrate the drug’s effect. If successful, fasedienol could be the breakthrough for social anxiety, a huge market with no acute treatment currently. We estimate the stock could more than double on positive data (given the prior failure, the market is skeptical, but success would flip the script dramatically – possibly bringing partnership offers or at least a re-rating to reflect a viable CNS asset).

New info: As of early November, VTGN completed the trial and reaffirmed data by year-end . They also signaled plans for an NDA in mid-2026 , implying confidence. Their cash position is strong enough that even in a downside scenario (if the trial disappoints), the company isn’t facing immediate distress – they can pivot to other programs, which might cushion the stock somewhat.

Plan: Hold through data. This position diversifies our catalyst risk (it’s CNS vs. MIST’s cardiovascular vs. SLS’s oncology). We maintain a stop at $3.20 to guard against a collapse on bad news, but otherwise we’re giving VTGN the opportunity to deliver the kind of outsized return we need. Bottom line: VTGN offers a binary but potentially portfoliotransforming catalyst, and our research this week only strengthened our optimism that the trial design fixes could yield a surprise win.

SELLAS Life Sciences (SLS)

Catalyst: Phase 3 REGAL trial final analysis (survival in AML) expected around year-end.

We are holding SLS (13 shares, ~25% allocation) as our third “lottery ticket.” Thesis: SLS’s GPS vaccine is attempting something never done – meaningfully prolong survival in AML patients in second remission. It’s high-risk, but interim looks were encouraging (the IDMC in August recommended to continue the trial with no modifications , suggesting no glaring futility signal). If REGAL is positive, SLS could re-rate massively: not only would GPS become a valuable late-stage asset (attracting partner or acquirer interest), but SELLAS’s other program (SLS009, a CDK9 inhibitor) also has demonstrated promising data, meaning the company could suddenly have two valuable assets. In a success scenario, multi-bagger returns (stock from ~$1.50 to $5+ range) are conceivable.

New info: In Q3 updates, SELLAS announced it bolstered cash (now ~$73M total) , which ensures they can operate well into 2026 – so even if REGAL fails, they won’t be bankrupt (they’d pivot to SLS009, etc.), which could mean the stock might not go to penny-stock levels; and if REGAL succeeds, they have the cash to push toward approval. Also, we noted insiders and KOLs expressing “genuine enthusiasm” at the R&D day – while that’s anecdotal, it’s a positive sentiment indicator.

Plan: This is our smallest position due to the high uncertainty, but we’re fully prepared to hold through the readout. We have a tight stop to limit a blow-up risk. If the news is good, we’ll take profit systematically because small biotech can be volatile even after good news (we’d expect to sell into strength, possibly keeping a tiny stub if we see longer-term value, but likely we’ll realize gains). In summary, SLS is the highest risk of the bunch, but it’s a deliberate inclusion to give us a third independent chance at a game-changing win. The reward-to-risk still seems favorable given the stock’s low price and our sizing of the position.

Portfolio-Level Thesis

Our portfolio as a whole is an “all or nothing” catalyst strategy. We acknowledge that we’ve concentrated into three biotech events, which means our fate is less about market conditions and almost entirely about the outcomes of these specific milestones. The rationale is that we’re currently behind the benchmark (S&P 500) by a considerable margin, and with only a few weeks left, playing it safe won’t catch up. We need one or more big wins. Each stock in our portfolio has the potential to double (or more) on good news. They are uncorrelated events – an FDA approval, a CNS trial result, an oncology trial result – so the probability that all fail is lower than the probability that at least one succeeds. One success could lift the portfolio significantly; two or three could make for a spectacular finish. We have mitigated risk where we can (position sizing, stop losses, choosing companies with enough cash to survive setbacks), but we intentionally accept higher volatility now. We have not added any new positions this week because none matched the immediacy and upside of what we already hold.

Execution and Orders Summary

No new buy/sell orders were placed, other than adjusting stop- loss orders. This is reflective of our confidence in the current holdings. We did adjust MIST’s stop from $1.50 to $1.60 to secure some gains (given the stock’s rise) while still giving it breathing room. For VTGN and SLS, stops remain as-is. We’ll re-evaluate stops dynamically as prices move. By not trimming or selling anything now, we ensure we have maximum skin in the game for each catalyst. Our view is that the portfolio’s upside capture is more important at this juncture than short-term downside avoidance – provided we have disaster stops in place, which we do.

Next Week Preview

By the end of Week 23 or during Week 24, we may have the result for SLS (since it’s “any day” timing). We are prepared to act on that immediately as per our plan – cut losses or take profit. MIST’s decision will come in Week 24’s window (mid-week), so in the next weekly report we will likely be discussing how we handled that binary event. VTGN’s readout might come in the final week or so. The sequence of these events actually provides a bit of a natural hedge: they are spaced such that we can potentially redeploy capital from one outcome to the next if needed (e.g., if SLS fails, its remaining funds might bolster VTGN or MIST if those haven’t hit yet; if SLS succeeds big, we might lock in and increase our cash or even add to VTGN ahead of its result). We will make those tactical decisions as news comes.

Thesis Confidence

Overall, we are heading into these catalysts with confidence grounded in research:

- MIST: High probability, data-driven bet on an FDA win in a well-studied indication.

- VTGN: Reasonable probability, improved trial design and strong scientific rationale, with huge upside if it pans out.

- SLS: Uncertain probability (as any cancer immunotherapy is), but the payoff would be massive and the company has set itself up well (financially and scientifically) for either outcome.

By maintaining our positions and strategy, we ensure that if our research was correct, we will reap the rewards. If we’re wrong, our risk measures should prevent catastrophic loss of capital.

In summary, we have a clear line of sight on three major catalysts in the coming weeks. Our portfolio is positioned to capitalize on these with no distractions. We have laid out exact contingency plans and will execute them with discipline. The next week will be largely about monitoring and reacting, as the heavy lifting in terms of positioning is already done. We enter this critical phase with a mixture of caution (via stops) and optimism (via conviction to hold through volatility). Now it’s up to the outcomes – and we’re as ready as we can be to manage whatever comes.

Research Hub + Disclaimer

This project is purely educational and research-focused. The thesis summary above is completely generated by A.I. Nothing here should be taken as financial advice. Full disclaimer: Here

GitHub Page and Email:

To see all past deep research reports and summaries: Here

Full chats: Here

Have a question? Check out: Q&A

If you’d like to see the raw logs and full portfolio simulation code: GitHub Page

If you have any suggestions or advice, my Gmail is: nathanbsmith.business@gmail.com

[story continues]

tags