This article discusses indices in a broad view, without separating them into Index as a list/benchmark (not investable on its own). and Index fund as a financial product you can buy that tracks an index.

Crypto indices are the unsung heroes of the 2025 bull run, offering diversified exposure amid wild narratives like RWAs and meme madness. But are they smart play or just hype? Let's dive into current trends with real examples.

Cryptocurrency indices transform dozens or hundreds of token prices into a single tradable asset, providing a starting point for passive market participation.

The main functions of an index are price determination, tradable benchmarks, calculation rates, and inclusion/weighting rules management. Good indices are auditable, resistant to manipulation, and transparent about their sources.

A simple example is the market capitalization index: a list of coins by circulating supply multiplied by their price, weighted by capitalization. Pros: intuitive, widely used. Cons: concentrates on big winners and is vulnerable to extreme outliers (e.g., a very large coin dominating by weight). Read to the end to find a list of index trade-offs.

Scientists and practitioners use machine learning and network correlation analysis to test index formation approaches.

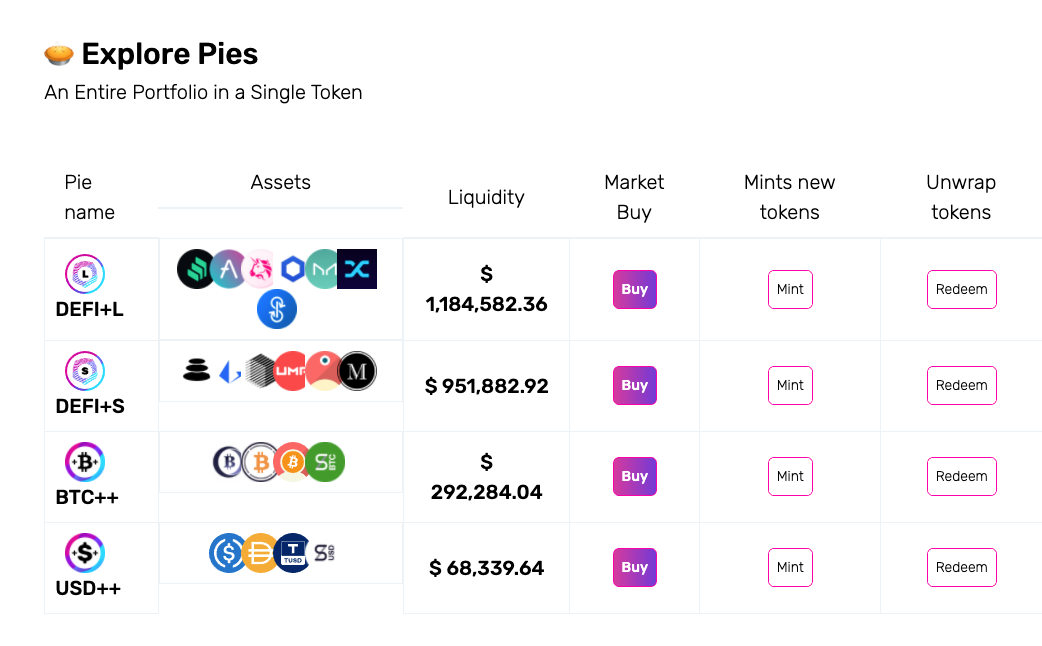

Theme indices? like DeFi index or L1 index — useful for product design and targeted exposure.

Indices must aggregate across many venues (CEXs/DEXs/aggregators) and handle 24/7 markets, stale feeds, and liquidity gaps — technical complexity that traditional equity indices didn’t face at launch. Here, the advantages of non-custodial Web3 indexes are fully realized.

Good crypto indices are not just formulas — they are governance processes that translate chaotic markets into investable products.

Still want to select assets manually?

Crypto Indices history

The development of crypto indices mirrors the broader cryptocurrency ecosystem's evolution, blending technological advancements (e.g., blockchain data aggregation) with economic milestones (e.g., market maturation and institutional adoption).

The timeline reflects the main stages that have impacted both custodial and non-custodial solutions.**

**

-

2013: Early price aggregation and indices. Simple price trackers and exchange price feeds emerged (

CoinMarketCap ) -

2013: CoinDesk launches

proprietary Bitcoin Price Index -

2013-2017: Market Expansion and First Indices. Rise of altcoins and exchanges, ICO boom leads to early indices like capitalization-weighted models (Laspeyres/Paasche methods).

-

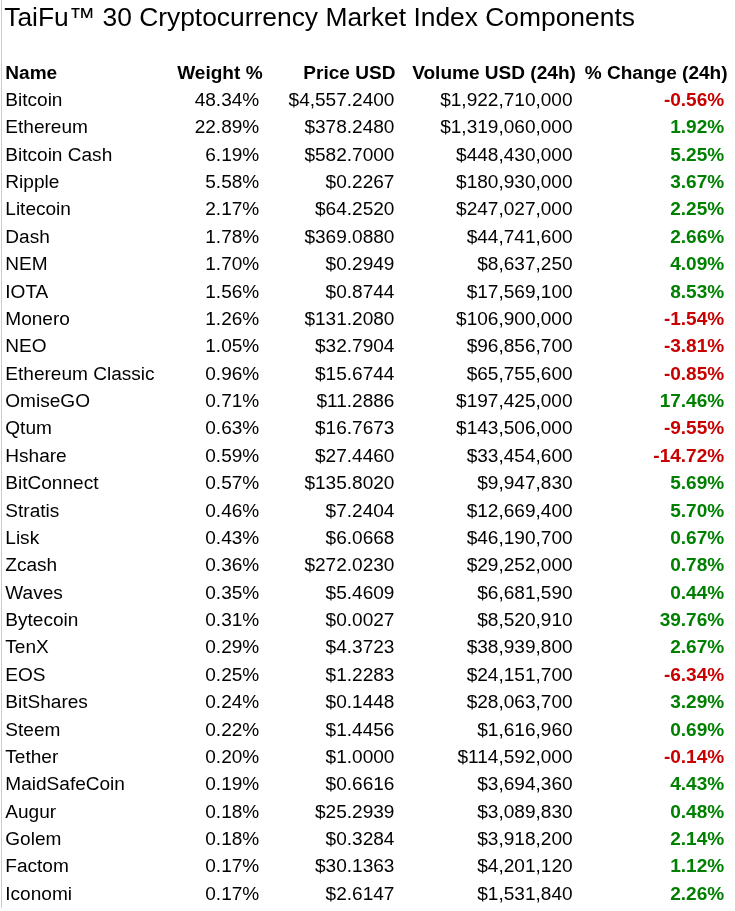

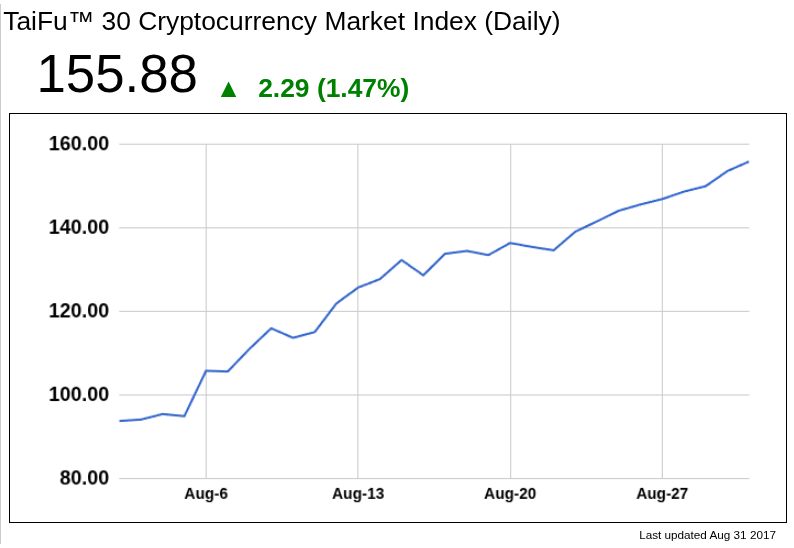

2017: TaiFuIndexes – The World’s 1st Cryptocurrency Market Indexes.

-

2018-2020: Ethereum DeFi protocols emerge

-

2020:

Bitwise launched the 10 Crypto Index Fund . Organized as a trust rather than an ETF, the fund is traded in the OTC market with the symbol BITW. -

2020:

PieDAO brings collective governance to smart token indexes . PieDAO is a decentralized organization allowing its users to vote on the creation and parameters of pooled index funds composed of different ERC20 tokens on the Balancer protocol.

-

2021-2023: Boom, Bust, and Maturation. Layer-2 scaling and oracles improve data feeds for indices. 2021 bull run boosts index funds; 2022 crash exposes risks. Focus on rules-based rebalancing.2021:

Crypto Volatility Index (CVI) was launched . CVI allows Users to Hedge Themselves Against Market Volatility and Impermanent Loss -

2021:

S&P Dow Jones Indices Launches Cryptocurrency Index Series -

2023-2024:

Asset managers filed ETF applications ; regulators required rigorous index methodology and custody details.

- 2024:

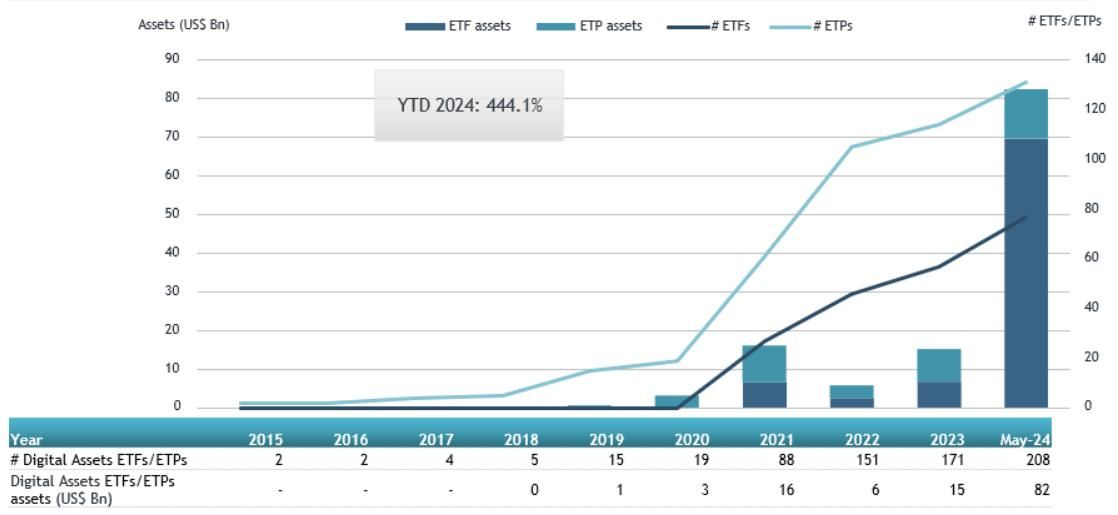

Spot Bitcoin ETFs approved . Approval of spot Bitcoin accelerated demand for compliant indices and reference rates. - 2024–2025: Expansion and mainstreaming. Index providers expanded thematic, multi‑asset indices; tradable products built on indices (ETFs, structured products) gained traction. Large asset managers sought index partners or filed their own crypto index ETF proposals.

- 2025:

A record-breaking 72 crypto ETFs are awaiting SEC approval - 2025: Chainalysis' 2025

Adoption Index shows institutional growth . - 2025: Markets moving toward standardized listing rules, more ETFs across assets, and stronger governance frameworks. (Ongoing developments continue to shape index design and distribution.)

- 2025:

SEC has approved general listing standards for crypto ETFs .

How to create crypto index

Creating crypto indices involves systematic methodologies to aggregate and weight assets, ensuring they reflect market dynamics. Key approaches include:

Weighting Methods:

- Market Capitalization-Weighted: Most common (e.g., like the S&P 500 for stocks). Assets like BTC and ETH get higher weights based on total value (price × circulating supply). Pros: Reflects economic size. Cons: Prone to dominance by large caps.

- Equal-Weighted: Each asset gets the same allocation (e.g., Crypto20 Index). Ideal for diversification but ignores size differences.

- Price-Weighted: Based on asset price (rare in crypto due to volatility; e.g., early Bitcoin indices).

- Fundamental or Liquidity-Weighted: Factors in metrics like trading volume, on-chain activity, or developer activity (e.g., Messari's indices). Used for sector-specific ones like DeFi.

Selection Criteria:

- Top performers by market cap, volume, or narrative relevance (e.g., AI tokens for 2025 AI indices).

- Rebalancing: Quarterly or monthly adjustments to adapt to market shifts.

Research Methods:

- Data Collection: Aggregate from multiple exchanges via APIs to mitigate single-source bias. On-chain analytics from tools like

Dune Analytics for metrics like TVL (Total Value Locked) in DeFi. - Quantitative Analysis: Statistical models like

Sharpe ratio for risk-adjusted returns, correlation matrices to ensure diversification, and volatility forecasting viaGARCH models . Backtesting simulates historical performance. - Qualitative Research: Narrative analysis. Surveys or expert panels validate sector relevance.

- Hybrid Approaches: Machine learning for anomaly detection (e.g., spotting pump-and-dumps) and dynamic indexing.

These methods draw from established finance (e.g., adapted from

Governance & compliance frameworks:

Published rulebooks for inclusion/exclusion, reconstitution frequency, and audit trails; certification to regulatory standards for providers.

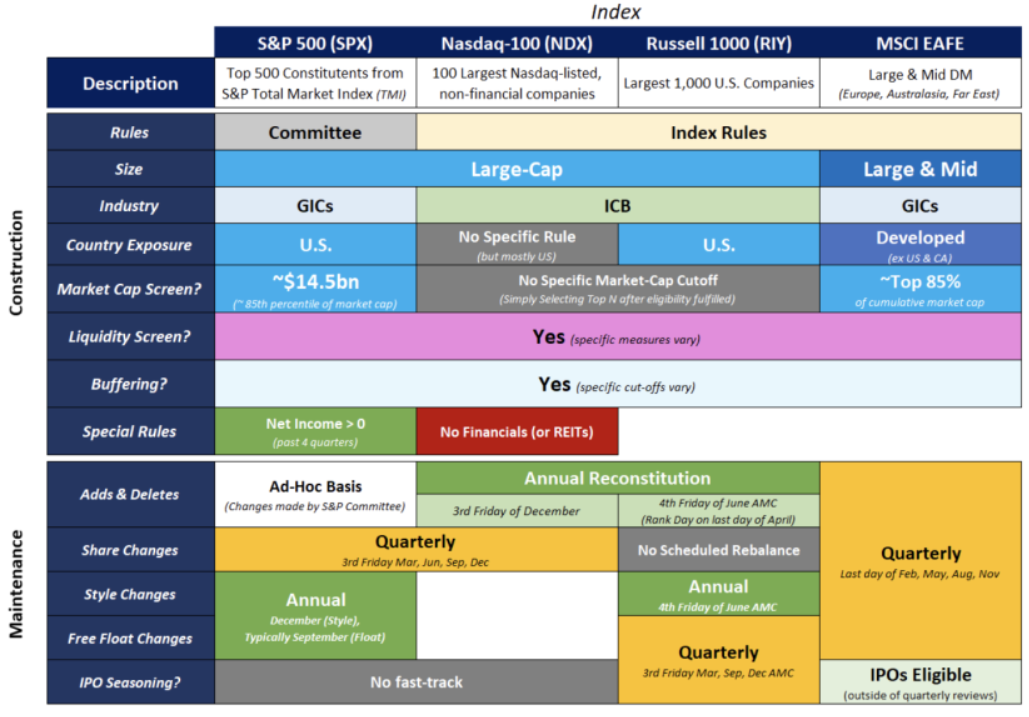

Classic Tradeoffs in Financial Index Design

These tradeoffs are fundamental when constructing or investing in indexes, and they directly shape its design, benchmark selection, and asset allocation decisions

- Market-Cap Weighting vs. Equal Weighting. Market-cap weighting is efficient, low-cost, and widely used, but it overweights overvalued stocks. Equal weighting reduces concentration risk but increases turnover and costs.

- Price-Weighted vs. Value-Weighted Indexes. Price-weighted indexes (e.g., Dow Jones Industrial Average) are simple but arbitrary, overweighting high-priced stocks. Value-weighted (market cap) better reflects economic size, but can be distorted by bubbles.

- Broad Diversification vs. Concentration. Broad indexes (MSCI ACWI, S&P 1500) reduce idiosyncratic risk but dilute exposure to strong performers. Narrower indexes (e.g., Nasdaq-100, sector indices) offer focused exposure but with higher volatility.

- Passive vs. Smart Beta / Factor Indexing. Passive cap-weighted indexes are cheap and transparent. Factor or “smart beta” indexes (value, momentum, quality) aim for excess returns but introduce model risk, turnover, and concentration.

- Liquidity vs. Representation. Indexes often exclude illiquid small-cap assets to ensure investability. But this exclusion biases the index away from the full economic universe.

Key Research:

Optimal Versus Naive Diversification: How Inefficient is the 1/N Portfolio Strategy?

Cap-Weighted Portfolios are Sub-Optimal Portfolios.

Perold (2007), “Fundamentally Flawed Indexing”

Roll (1977), “A Critique of the Asset Pricing Theory’s Tests”

Statman (1987), “How Many Stocks Make a Diversified Portfolio?”

Campbell, Lettau, Malkiel & Xu (2001), “Have Individual Stocks Become More Volatile?”

Fama & French (1993), “Common Risk Factors in the Returns on Stocks and Bonds”

Arnott, Hsu & Moore (2005), “Fundamental Indexation”

Amihud & Mendelson (1986), “Asset Pricing and the Bid-Ask Spread”

Chen, Noronha & Singal (2004), “The Price Response to S&P 500 Index Additions and Deletions”

Index Market Challenges and Unresolved Problems

Below is a general list of potential weaknesses of indices. Some of them are general, others are specific and apply only to Web 2 indices or only to indices consisting of small-cap assets.

- Volatility and Market Uncertainty: Extreme price swings make indices unpredictable. Sentiment, economic, and political factors predict but don't prevent crashes.

- Regulatory and Compliance Issues: Unclear rules on stablecoins/token classification; fines and licensing hurdles. Global inconsistencies, especially in EMEs; crypto as "toxic" money substitutes.

- Liquidity fragmentation across chains. Many indices track illiquid altcoins, causing tracking errors in real products. Economic challenge: High fees for rebalancing.

- User and Adoption Barriers: Need for better UX and decentralized clearing. Lack of understanding, emotional trading, and inconsistent data. Broad exposure without picking individual tokens; low-fee index funds/ETPs for retail. Access to cleaned historical constituent data, methodology transparency.

- Model risk and overfitting. Heavy reliance on historical correlations or ML models can fail in regime shifts. Academic work shows correlations spike during crises, limiting diversification benefits.

- Data Integrity and Manipulation: Reliance on exchange data invites issues like wash trading or fake volume (e.g., 2023 FTX revelations). Lack of standardized auditing.

What’s next

Indices are not the holy grail of finance, but they offer clear advantages to long-term investors. Furthermore, this financial instrument continues to evolve, and non-custodial indices are free from many of the drawbacks of traditional solutions and offer the greatest flexibility and stability.

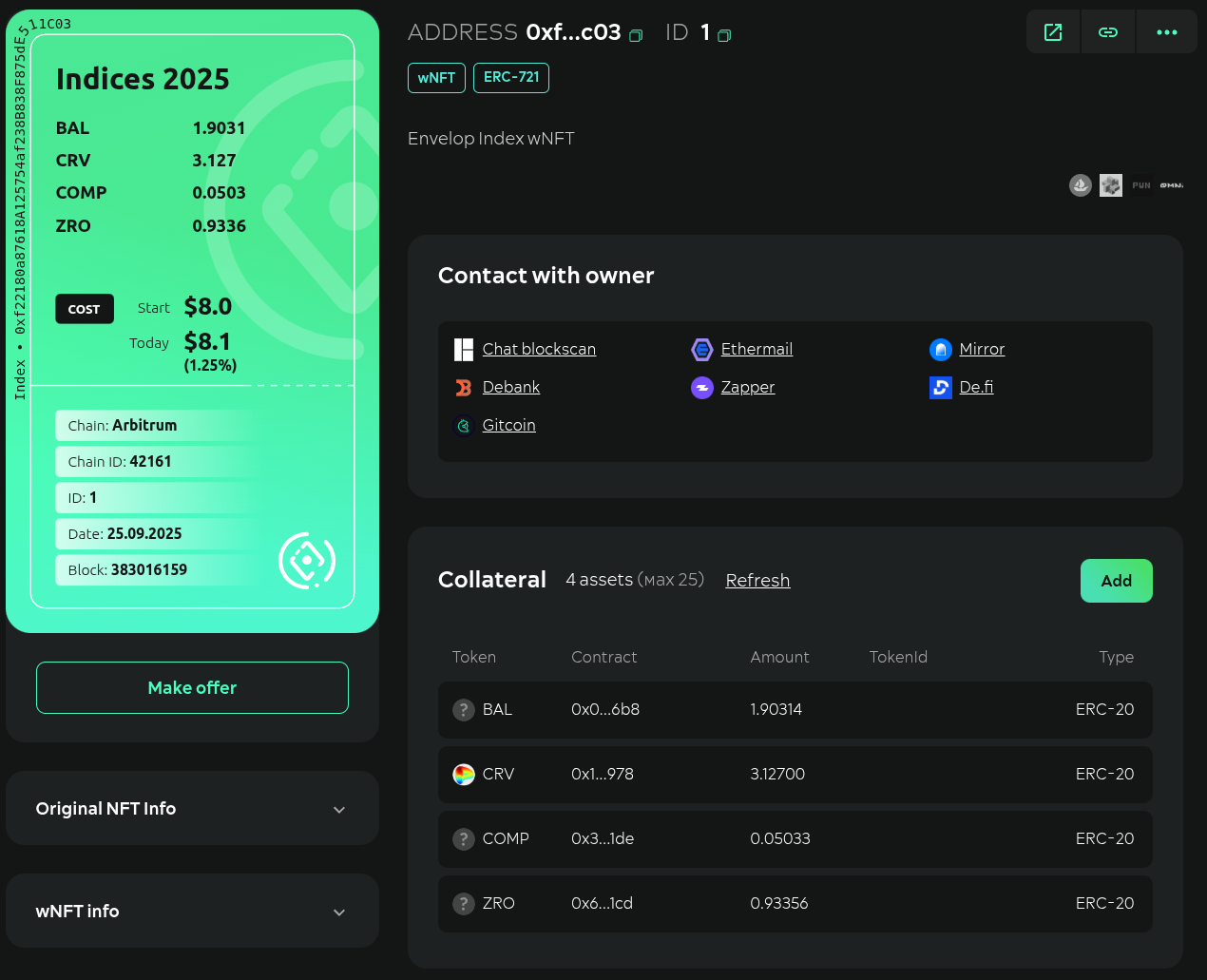

Many projects have attempted to implement this idea in the past, and many more will do so in the future. Currently, it’s worth noting the Envelop protocol v2.

The next step in evolution will be omnichain indices of income strategies and agents.

[story continues]

tags