Authors:

(1) Jiefei Yang, †Department of Mathematics, University of Hong Kong, Pokfulam, Hong Kong (jiefeiy@connect.hku.hk);

(2) Guanglian Li, Department of Mathematics, University of Hong Kong, Pokfulam, Hong Kong (lotusli@maths.hku.hk).

Table of Links

- Bermudan option pricing and hedging

- Sparse Hermite polynomial expansion and gradient

- Algorithm and complexity

- Convergence analysis

- Numerical examples

- Conclusions and outlook, Acknowledgments, and References

Abstract. We propose an efficient and easy-to-implement gradient-enhanced least squares Monte Carlo method for computing price and Greeks (i.e., derivatives of the price function) of high-dimensional American options. It employs the sparse Hermite polynomial expansion as a surrogate model for the continuation value function, and essentially exploits the fast evaluation of gradients. The expansion coefficients are computed by solving a linear least squares problem that is enhanced by gradient information of simulated paths. We analyze the convergence of the proposed method, and establish an error estimate in terms of the best approximation error in the weighted H1 space, the statistical error of solving discrete least squares problems, and the time step size. We present comprehensive numerical experiments to illustrate the performance of the proposed method. The results show that it outperforms the state-of-the-art least squares Monte Carlo method with more accurate price, Greeks, and optimal exercise strategies in high dimensions but with nearly identical computational cost, and it can deliver comparable results with recent neural network-based methods up to dimension 100.

1. Introduction

The early exercise feature of American or Bermudan options gives holders the right to buy (call) or sell (put) underlying assets before the expiration date, and their accurate numerical calculation is of great practical importance. Meanwhile, the efficient estimation of Greeks (i.e., derivatives of the price function, e.g., delta and gamma) is vital for hedging and risk management, since the theory of option pricing builds on the assumption of the absence of arbitrage. For example, when the asset price is on the rise, the gain in the long position of a call writer’s asset may offset the potential loss of the call option.

Nonetheless, the early exercise feature of American options poses significant challenges for computing price and Greeks, especially in high dimensions. One of the most popular methods for high-dimensional American option pricing is the least squares Monte Carlo (LSM) method [15, 22]. Computing Greeks in high dimensions is more involved, and further developments with LSM have been proposed [24, 5]. In this work, building on LSM, we shall develop a simple, fast, and accurate algorithm, termed as gradient-enhanced least squares Monte Carlo (G-LSM) method, c.f. Algorithm 4.1, for computing price and Greeks simultaneously at all time steps for dimensions up to 100. The key methodological innovations includes using sparse Hermite polynomial space with a hyperbolic cross index set as the ansatz space for approximating the continuation value functions (CVFs), and incorporating the gradient information for computing the expansion coefficients.

Now we situate the present study in existing works. Currently, there are two popular classes of methods to price American options in high dimensions: (i) least-squares Monte Carlo-based (LSM) methods and (ii) DNN-based methods. The LSM method has shown tremendous success for pricing American or Bermudan options with more than one stochastic factors. The original LSM [15] uses polynomials to approximate the CVF, and other choices have also been explored, e.g., Gaussian process [16] and DNNs [14, 4]. Recently, LSM with the hierarchical tensor train technique has been studied in [2], which demonstrates the success of polynomial approximation for CVFs in very high dimensions. The proposed G-LSM is a variant of LSM that incorporates gradient information that comes nearly for free. Due to the excellent capability for high-dimensional approximation of DNNs, several methods based on DNNs have been proposed for pricing American or Bermudan options, based on optimal stopping problem (parameterizing the stopping time by DNNs and then maximizing the expected reward [3]), free boundary PDEs (parameterizing PDE solutions with DNNs [21]), or BSDEs (parameterizing the solution pair of the associated reflected BSDE [8] by DNNs [12]). Within the framework of BSDEs, Chen and Wan [6] suggest approximating the difference of the CVF between adjacent time steps by averaging several trained neural networks, which has a quadratic complexity in the number of time steps. Wang et al. [23] extend the deep BSDE method [7] from European option pricing to Bermudan one, with the loss function being the variance of the initial value, and Gao et al. [10] analyze its convergence. In comparison with DNN-based methods, G-LSM enjoys high efficiency and robustness, which involves only least-squares problems and is easy to implement.

The structure of this article is organized as follows. In section 2, we describe the mathematical framework of pricing and hedging high-dimensional American or Bermudan options, and in section 3, we recall several useful properties of generalized Hermite polynomials and approximation with sparse hyperbolic cross index set. Then in section 4, we derive the main algorithm, i.e., gradient-enhanced least squares Monte Carlo (G-LSM) method, and establish its local and global error estimates in section 5. In section 6, we present extensive numerical results including prices, Greeks, optimal stopping time, and computing time. We also present a comparative study with existing methods. Finally, we conclude in section 7 with further discussions.

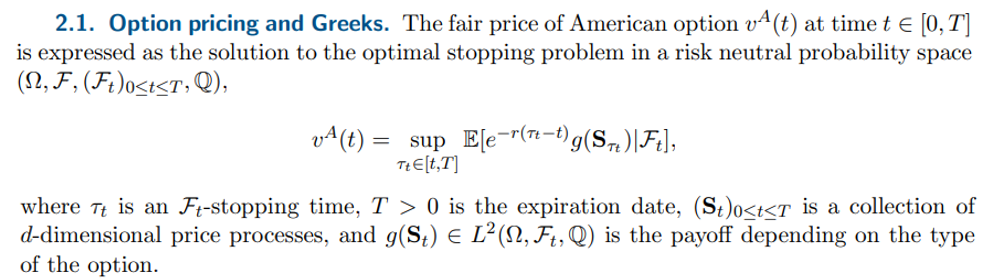

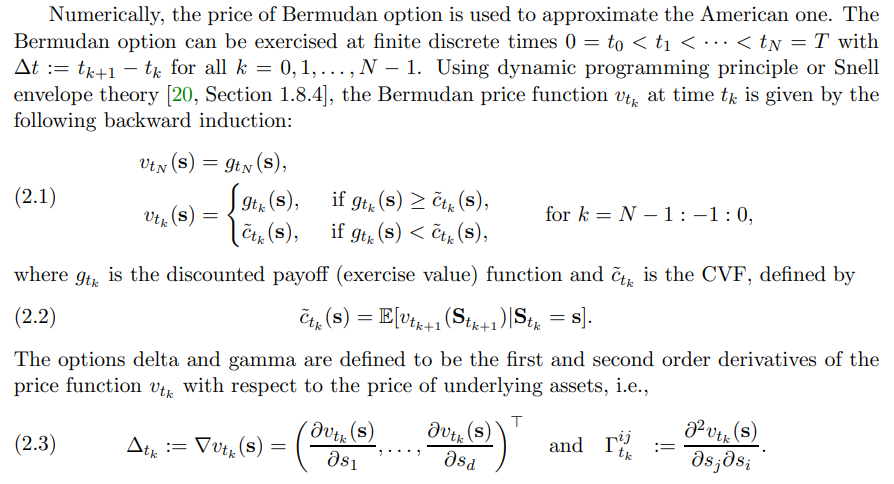

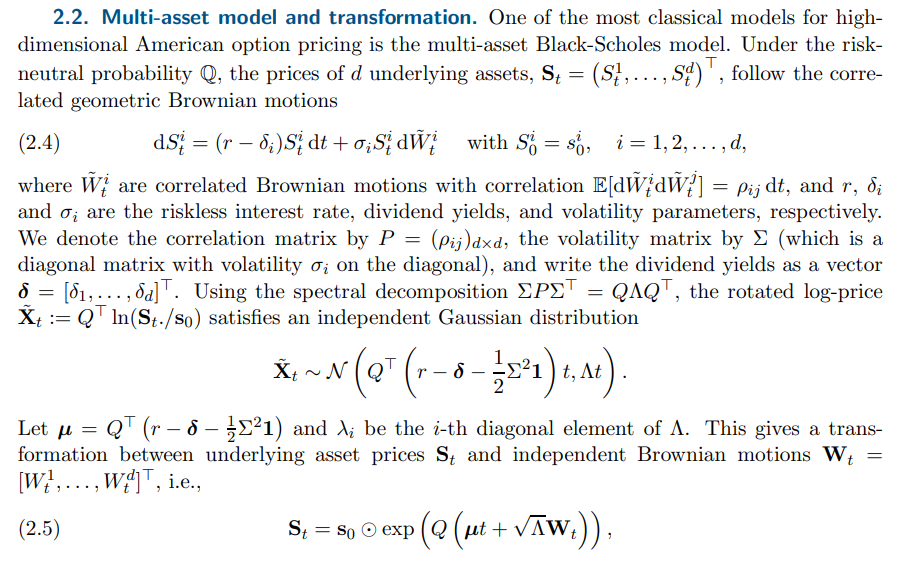

2. Bermudan option pricing and hedging

Now we describe the valuation framework for American or Bermudan option pricing and hedging.

We consider all exercise and continuation values of Bermudan option discounted to the time t = 0.

where ⊙ denotes componentwise product.

3. Sparse Hermite polynomial expansion and gradient. Sparse polynomial chaos expansion can serve as a surrogate model of unknown stochastic variables with finite second-order moments. The motivations of using sparse Hermite polynomial expansion for pricing and hedging American options are twofold:

This paper is

[story continues]

tags