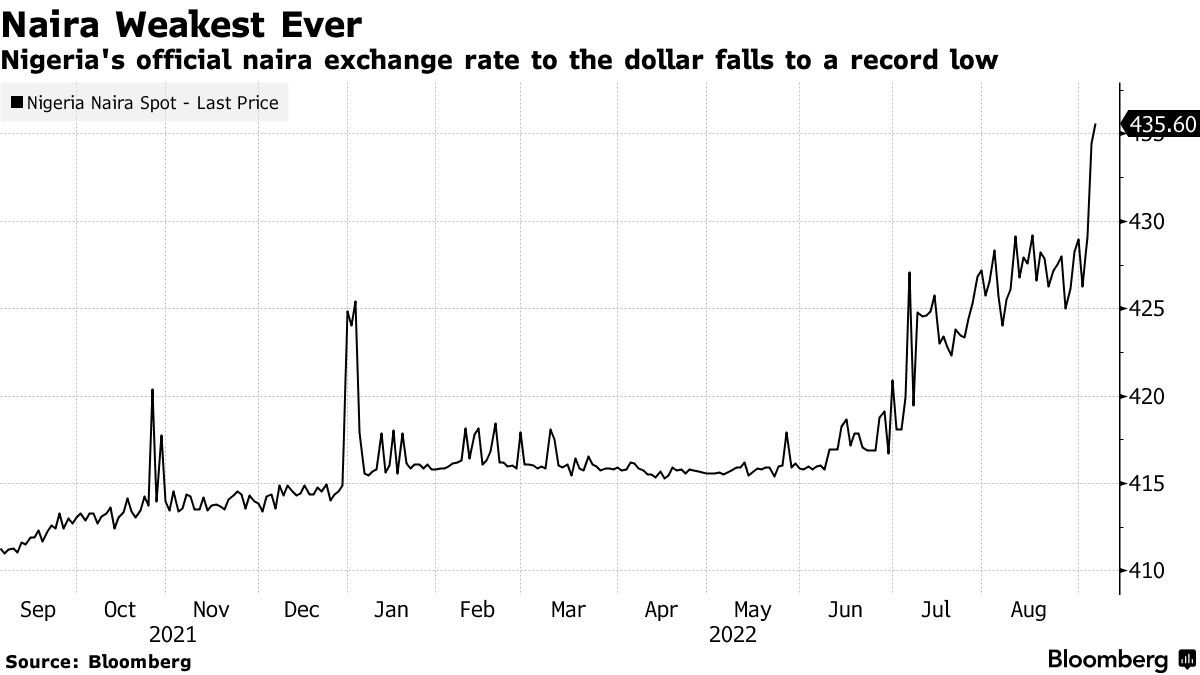

In 2023, a textile exporter in Lagos watched helplessly as the Nigerian naira collapsed against the dollar. She had signed contracts months earlier to deliver fabric to European buyers at fixed naira prices, confident that she could hedge her currency exposure through her bank. But when she approached the bank to lock in exchange rates, she discovered that the minimum transaction size was $100,000, ten times larger than her typical shipment value. Without access to hedging instruments, she absorbed the full force of the currency swing. A 40% devaluation meant that what should have been a profitable quarter became a devastating loss.

Her story is not unique. Across emerging markets, small and medium-sized enterprises (SMEs) face a brutal reality: they operate in the same volatile currency environment as multinational corporations, but they lack access to the same protective tools. While large companies employ treasury teams and sophisticated hedging strategies, SMEs are left exposed to exchange rate fluctuations that can erase their profit margins overnight.

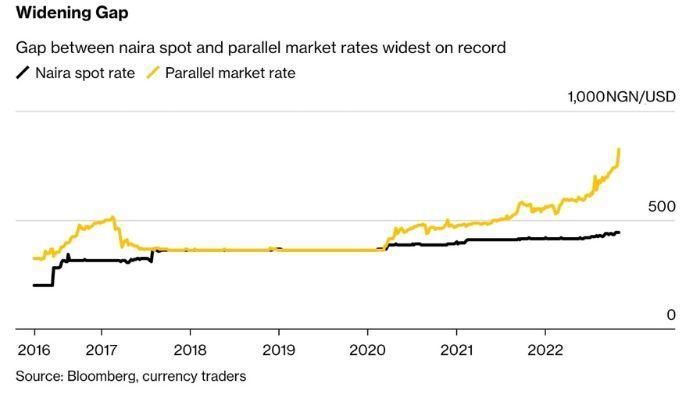

In 2023 alone, Nigerian companies reported N1.7 trillion (approximately $2.1 billion) in foreign exchange losses. Major corporations like Adidas, BBVA, and Dow Chemical collectively lost over $3.3 billion due to the devaluation of the Argentine peso. These headline figures represent just the visible tip of a much larger problem, for every large corporation reporting FX losses, thousands of SMEs suffer similar or worse fates in silence.

The fundamental issue is structural: traditional hedging instruments were designed for large corporations with predictable cash flows and substantial transaction volumes. Banks impose minimum ticket sizes, collateral requirements, and complex pricing structures that effectively exclude SMEs from protection. The result is a two-tiered system where large firms can manage currency risk while small businesses bear it fully.

Gluwa's blockchain-based platform offers a different approach, one that makes micro-hedging accessible to businesses that traditional finance has left behind.

The SME Pain

The barriers that prevent SMEs from hedging currency risk are numerous and interconnected.

Minimum ticket sizes exclude most small transactions. Banks typically require hedging contracts of $50,000 to $100,000 or more. For an SME importing goods worth $10,000 or exporting products worth $25,000, these minimums are insurmountable. The mismatch between transaction size and hedging requirements leaves small businesses with a stark choice: accept full currency exposure or don't trade internationally at all.

Collateral requirements compound the problem. Even when SMEs meet minimum transaction sizes, banks demand collateral, often 10-20% of the contract value, to secure hedging positions. For businesses operating on thin margins and tight cash flow, tying up thousands of dollars in collateral is simply not feasible. The very businesses that most need protection from currency volatility are least able to afford the upfront costs.

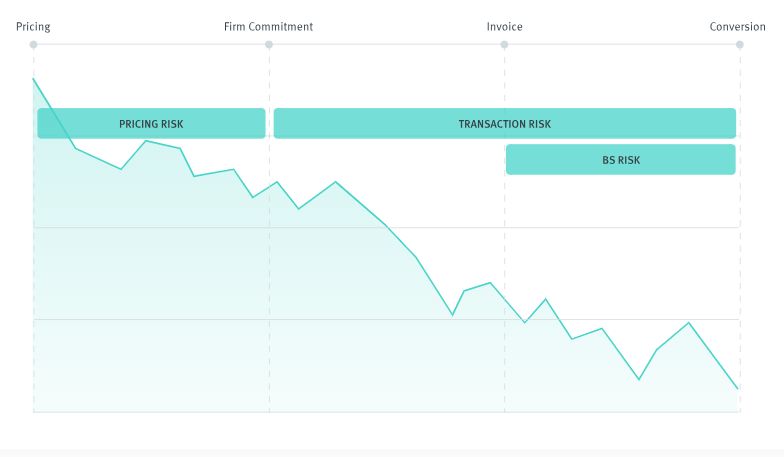

Slow settlements create timing mismatches. Traditional forward contracts and options settle through banking systems that can take 3-5 business days. During this settlement window, exchange rates continue to fluctuate, introducing basis risk, the possibility that the hedge itself becomes misaligned with the underlying exposure. For SMEs with rapid inventory turnover or short payment cycles, these delays undermine the effectiveness of hedging.

Opaque pricing makes it difficult to evaluate costs. Banks bundle hedging fees into exchange rate spreads, making it nearly impossible for SMEs to determine the true cost of protection. A forward contract might be quoted at a rate that appears reasonable, but hidden markups of 2-4% are common. Without transparency, SMEs cannot make informed decisions about whether hedging is economically viable.

The cumulative effect of these barriers is stark: less than 10% of SMEs use any form of currency hedging, compared to 92% of Fortune 500 companies. This disparity leaves small businesses disproportionately vulnerable to exchange rate volatility, a vulnerability that has only intensified as global currency markets have become more turbulent.

Gluwa's Micro-Hedge Toolkit

Gluwa's platform addresses these barriers through blockchain infrastructure that enables fractional hedging at scales previously impossible.

Hold stable value between invoice and settlement: At the core of Gluwa's approach is the use of stablecoins, cryptocurrencies pegged 1:1 to major fiat currencies like the US dollar. When an SME receives payment or prepares to make payment in foreign currency, they can immediately convert to stablecoins, effectively locking in the exchange rate at that moment. This eliminates the exposure window during which traditional banking settlements occur.

Consider a Nigerian exporter who invoices a European buyer in euros. Rather than waiting for the euro payment to arrive via wire transfer (3-5 days), convert to naira (with bank spreads of 3-5%), and then hope the exchange rate hasn't moved adversely, the exporter can receive payment in euro-pegged stablecoins and immediately convert to dollar-pegged stablecoins. The entire process takes minutes rather than days, and the exchange rate is locked at the moment of conversion.

Schedule tranches for time-based hedging: Gluwa's platform allows SMEs to schedule currency conversions in advance, creating a form of automated hedging. An importer who knows they'll need to pay suppliers in 30, 60, and 90 days can lock in portions of their currency exposure at different intervals, averaging out exchange rate risk over time.

This tranche-based approach mimics the sophisticated hedging strategies used by large corporations, but at scales accessible to small businesses. Rather than hedging a $1 million exposure all at once, an SME can hedge $10,000 exposures across multiple time periods, building a layered protection strategy that matches their actual cash flow patterns.

Auto-convert on trigger rules: The platform supports programmable conversion rules that execute automatically when certain conditions are met. An exporter might set a rule: "Convert to stablecoins if the naira weakens beyond 800 to the dollar." A rule-based system removes the need for constant monitoring and eliminates the emotional decision-making that often leads to poor timing.

These trigger rules can be as simple or complex as needed. A business might combine multiple conditions: "Convert 50% of holdings if the exchange rate moves 5% in either direction, and convert the remaining 50% if it moves 10%." This creates a graduated hedging strategy that provides partial protection while maintaining flexibility.

Vendor payouts in local currency via partners: While stablecoins provide the hedging mechanism, Gluwa recognizes that most SMEs ultimately need to transact in local fiat currencies. The platform integrates with local payment partners who convert stablecoins to local currency and disburse through familiar channels; bank transfers, mobile money, or cash pickup.

This hybrid approach combines the speed and transparency of blockchain settlement with the accessibility of local payment rails. An importer in Ghana can hold funds in dollar-pegged stablecoins until the moment they need to pay a supplier, then convert to cedis and disburse through mobile money, all within a single platform.

Unified ledger for invoices and hedges. Gluwa provides a single ledger that tracks both commercial transactions (invoices, purchase orders) and hedging activities (conversions, holdings). This unified view eliminates the reconciliation headaches that plague businesses trying to match hedging contracts with underlying exposures across multiple banking systems.

Finance teams can see at a glance: which invoices are hedged, what exchange rates were locked in, when conversions occurred, and what fees were paid. This transparency enables better decision-making and simplifies accounting and tax reporting.

Typical Journeys

Importer locks 30/60/90-day tranches. A furniture importer in Kenya buys from China with net 30, 60, and 90-day terms. Instead of waiting for due dates and current rates, they use Gluwa to lock rates when orders are placed. They convert shillings to stablecoins for the 30-day payment and set up automatic conversions for 60 and 90 days, hedging exchange rate risk. If the shilling weakens, they're protected. If it strengthens, they miss gains but gain pricing certainty. For SMEs, predictability is more valuable than currency changes. Exporter invoices in USD, auto-settles to NGN/GHS on receipt. A Nigerian software firm invoices US clients in dollars. Instead of wire transfers with delays and conversion spreads, they use Gluwa to receive payments in stablecoins.

The platform's rule is: "Convert 70% to naira for expenses, hold 20% in dollars, and convert 10% to naira if rates are favorable." This keeps enough local currency for expenses and reserves dollars, while the 10% conversion captures good rates. Marketplace escrow with milestone releases and hedging. A freelance platform uses Gluwa's escrow to hold payments until milestones are met. Funds are converted to stablecoins and released as milestones are completed, ensuring fair pay despite currency changes. Designers can lock in conversion rates at the project's start for a small fee (0.5-1%), choosing between currency risk or protection.

Benefits

Gluwa's micro-hedging offers more than currency protection.

- Margin protection allows SMEs to lock in exchange rates at contract signing, ensuring stable pricing and avoiding losses from currency changes.

- Settlement delays cost SMEs 0.6% to 2.1% of transaction value daily.

- For $500,000 in annual cross-border transactions, avoiding delays can save $3,000 to $10,500 yearly.

- Cash-flow predictability helps businesses plan better, manage working capital, and reduce the need for costly overdrafts or emergency financing.

- Fewer failed payments occur because exchange rates are fixed.

- In traditional systems, payments can fail if currency changes reduce the received amount. For example, an importer expecting $10,000 might get only $9,500 due to currency depreciation, affecting their ability to pay suppliers.

- Gluwa's system locks in values at commitment, removing this risk.

- Simpler books mean less accounting complexity, as traditional hedging requires tracking various contracts and valuations.

- Gluwa's unified ledger consolidates all activities, providing clear records and reducing accounting costs, making audits easier.

Success Metrics

Measuring micro-hedging effectiveness involves tracking key indicators. FX cost reduction vs. baseline shows that Gluwa's platform cuts currency conversion costs from 3-5% to 0.5-1.5%, saving 50-70%. For $200,000 in annual transactions, this saves $5,000 to $9,000, enough to hire an employee or invest in growth. Hedge uptake rate tracks how many eligible transactions are hedged. Gluwa's easy interface and low minimums achieve 60-80% uptake, compared to less than 10% in traditional banking.

Invoice DSO decrease (Days Sales Outstanding) shows how fast businesses get paid. By removing the 3-5 day wait of traditional wire transfers, Gluwa reduces DSO by about 4 days. This is important for businesses with tight cash flow, as it can mean paying employees on time instead of needing extra financing. Dispute rate checks how often payment disputes happen due to exchange rates or amounts received. Traditional cross-border payments often have disputes in 5-10% of transactions because the received amount can differ from expectations due to hidden fees or exchange rate changes. Gluwa's clear pricing and fixed rates lower dispute rates to under 1%.

Scale Path

Expanding access to micro-hedging requires strategic partnerships and adapting to different markets. Bank/PSP partnerships connect Gluwa's technology with current financial systems, letting businesses keep their banking relationships while adding blockchain-based hedging as a service, which speeds up adoption. Corridor-by-corridor liquidity programs make sure the platform can handle large currency pairs, starting with major ones like USD-NGN, USD-GHS, and EUR-KES, and then moving to smaller pairs as these grow, aiming for global reach. SME education modules help close the knowledge gap that stops businesses from using hedging tools by offering educational content, calculators, and simulation tools to help businesses understand currency risks and assess hedging strategies.

These education efforts are delivered through multiple channels: in-platform tutorials, webinars with local business associations, and partnerships with SME development organizations. The goal is not just to sell a product but to build financial literacy that enables better decision-making.

[story continues]

tags