TL;DR —

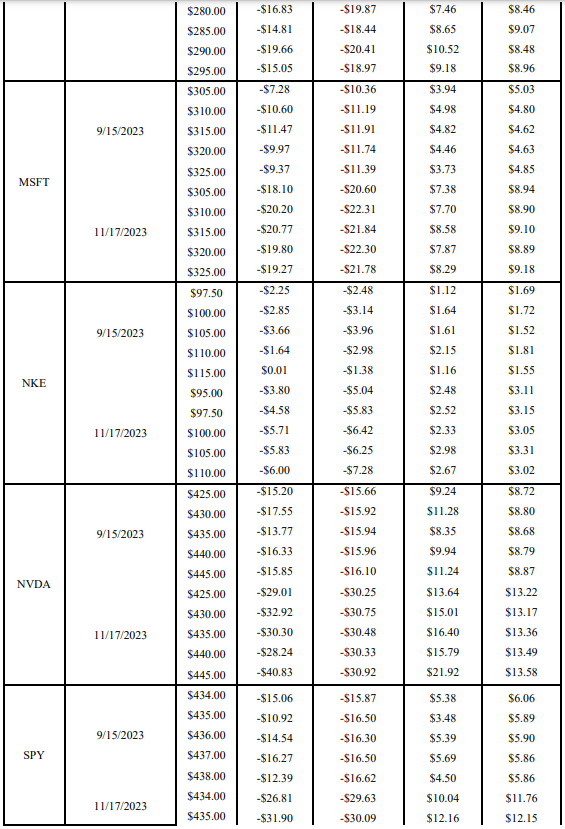

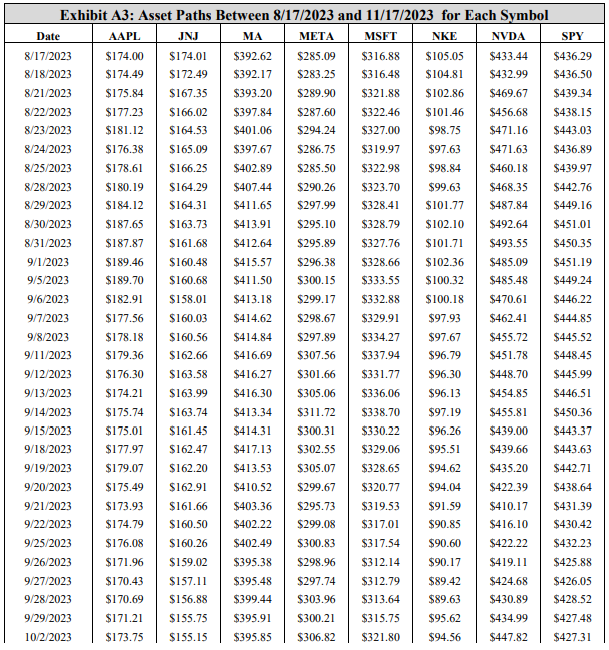

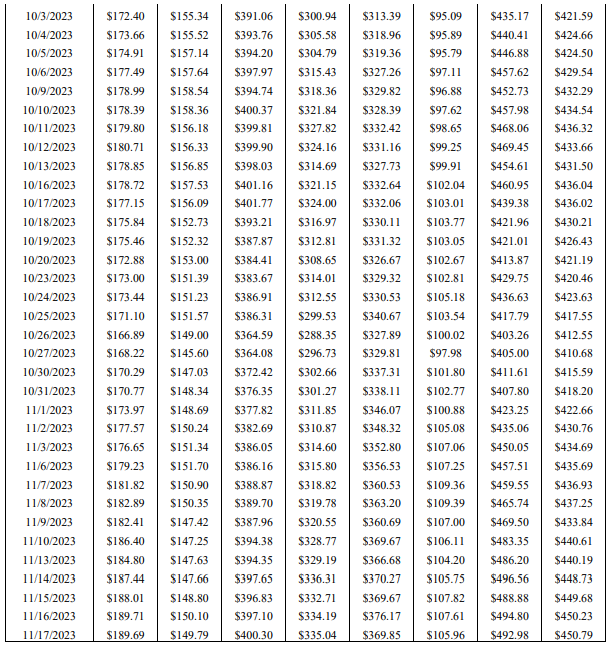

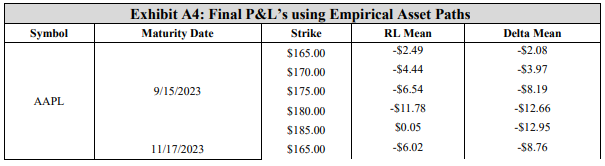

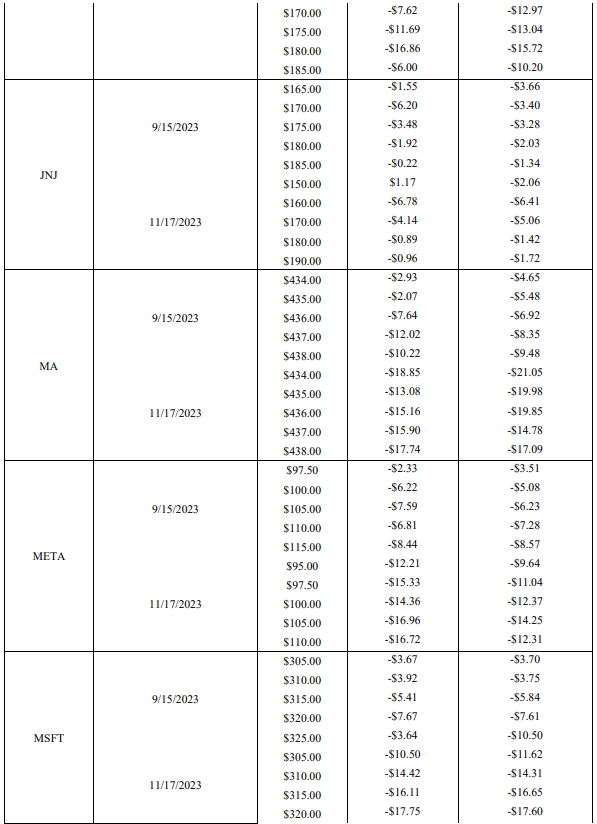

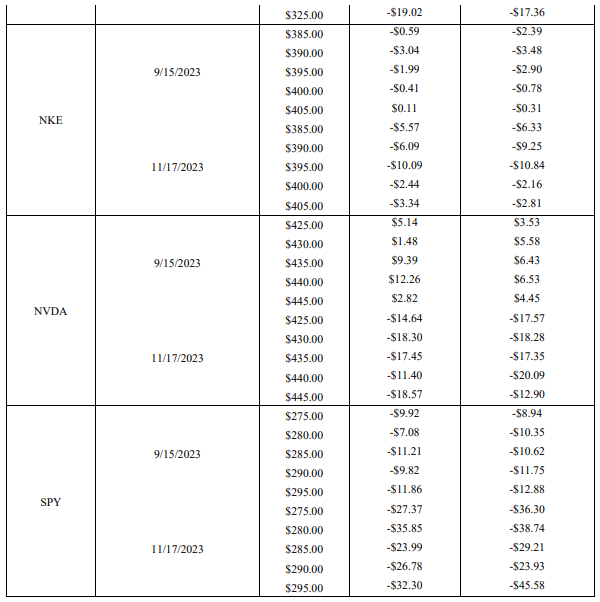

The appendix contains supplementary data tables detailing the final profit and loss (P&L) statistics for both the DRL agent and BS Delta strategies across various options. It also lists the asset paths used for testing, providing essential context and additional results that support the findings of the main paper.

Table of Links

-

Introduction

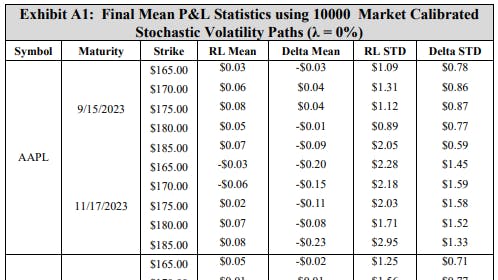

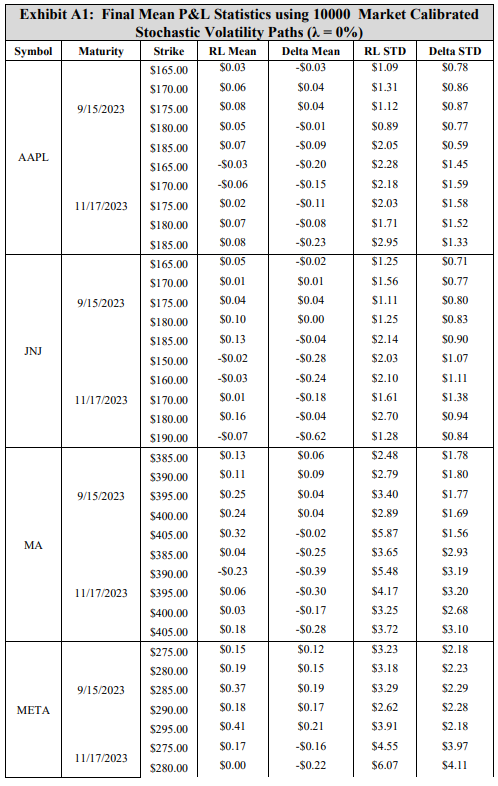

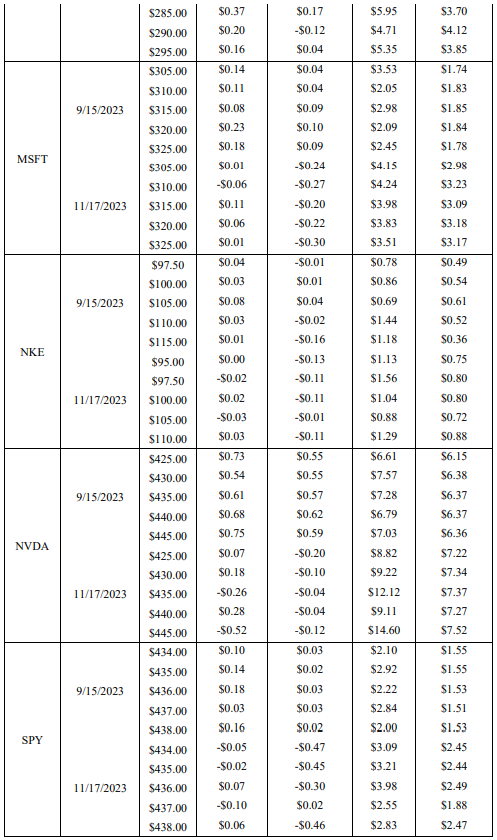

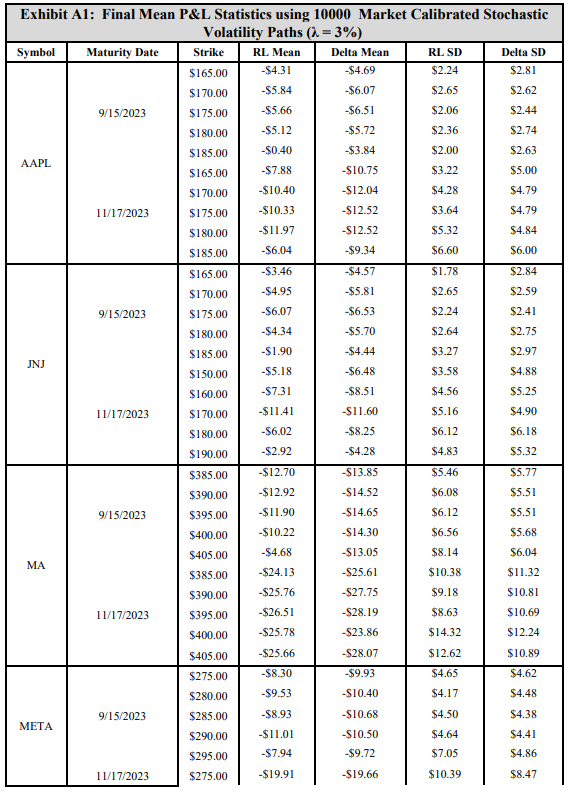

Appendix A

Authors:

(1) Reilly Pickard, Department of Mechanical and Industrial Engineering, University of Toronto, Toronto, ON M5S 3G8, Canada (reilly.pickard@mail.utoronto.ca);

(2) Finn Wredenhagen, Ernst & Young LLP, Toronto, ON, M5H 0B3, Canada;

(3) Julio DeJesus, Ernst & Young LLP, Toronto, ON, M5H 0B3, Canada;

(4) Mario Schlener, Ernst & Young LLP, Toronto, ON, M5H 0B3, Canada;

(5) Yuri Lawryshyn, Department of Chemical Engineering and Applied Chemistry, University of Toronto, Toronto, ON M5S 3E5, Canada.

This paper is

[story continues]

Written by

@hedging

Economic Hedging Technology is building an international and open source community dedicated to limiting economic risk.

Topics and

tags

tags

deep-reinforcement-learning|american-put-options|option-hedging|ddpg-algorithm|stochastic-volatility-models|geometric-brownian-motion|black-scholes-model|transaction-costs

This story on HackerNoon has a decentralized backup on Sia.

Transaction ID: fKT2ODOUB1lJ6Ji_527Vx3p5oVY7eI0GTmRU-hgqCFg