Table Of Links

1. Introduction and Motivation

- Relevant literature

- Limitations

2. Understanding the AI Supply Chain

- Background history

- Inputs necessary for development of frontier AI models

- Steps of the supply chain

3. Overview of the integration landscape

- Working definitions

- Integration in the AI supply chain

4. Antitrust in the AI supply chain

- Lithography and semiconductors

- Cloud and AI

- Policy: sanctions, tensions, and subsidies

- Synergies

- Strategically harden competition

- Governmental action or industry reaction

- Other reasons

6. Closing remarks and open questions

- Selected Research Questions

1. Introduction and Motivation

The development of artificial intelligence into a general-purpose technology this century could be as transformative as the internet or even the Industrial Revolution (see, e.g., Trammell and Korinek, 2023; Erdil and Besiroglu, 2023; Goldfarb et al, 2023; Elondou et al, 2023). Along with great opportunities, advanced AI systems also pose various risks, including cybersecurity threats, biological vulnerabilities, potential for social manipulation, worsening economic inequality, and reinforcing societal biases (see, e.g., Bengio et al, 2023; Acemoglu, 2021; Brundage et al., 2018).

To address these challenges, most AI policy experts support practices such as pre-deployment risk assessments, third-party model audits, and safety restrictions (Schuett et al., 2023). . Concerns about AI risks have already led to several responses, including President Biden's Executive Order on AI, the European Union's AI Act, the United Kingdom's AI Safety Summit, and the United Nations Secretary-General's creation of an advisory body dedicated to AI governance.

As noted by Cullen (2020) and Belfield and Hua (2022), antitrust considerations may affect or complement regulatory proposals for frontier AI models. This paper aims to provide a comprehensive overview of the current AI supply chain, focusing on companies that may be critical in developing transformative AI systems.

Special emphasis is placed on vertical integration and strategic alliances between these companies. We will focus primarily on foundation models, defined as AI models that are “trained on broad data at scale and are adaptable to a wide range of downstream tasks” (Bommasani et al., 2021). Throughout this report, we will focus on the supply chain required to train large foundation models with general capabilities ranging between GPT-3.5 and GPT-4, which we classify as frontier. We categorize models with capabilities comparable to GPT-3 to GPT-3.5 as non-frontier.

Our analysis primarily considers products perceived by consumers as rough substitutes, as we believe this dimension will be the most important one for both regulatory and antitrust interventions. Tentative relevant market definitions are established for each supply chain step, including lithography companies, cloud providers and chip designers.

This paper focuses primarily on the compute used for the training and deployment of AI models. We have chosen this focus for two main reasons: first, because alongside algorithms and data, compute is one of the three most significant inputs in AI development; and second, because unlike data or algorithms, compute is easily measurable and is a rival and excludable asset, making it easier to implement effective oversight mechanisms.

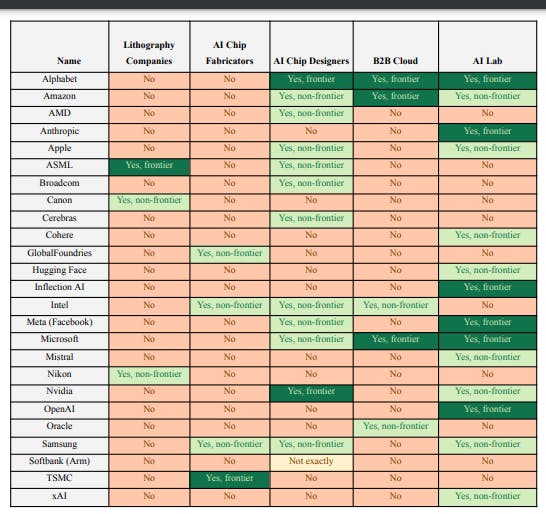

We profiled 25 leading companies in the AI industry and mapped 300 pairs of relationships between these companies and identified approximately 80 actions and mergers worth more than USD 100 million in which these companies were involved. Additionally, we documented other relevant events, such as major investments and disinvestments.

We mapped approximately 50 antitrust cases and conducted three brief case studies on the industry, including the OpenAI and Microsoft partnership and ASML's partnership with Intel, Samsung, and TSMC. Furthermore, we discussed some potential drivers that could explain why integration in the industry might be occurring.

The comprehensive mapping is available in the appendices as well as an online resource. The paper concludes by listing open questions and pointing out gaps in the existing literature accompanied by a preliminary discussion about how to best think about the market structure of different steps of the AI supply chain.

We also identify important open questions that need further exploration by industrial economists, competition lawyers, and regulatory authorities. To highlight potentially fruitful research areas, we start by discussing the market structure of various segments within the AI supply chain and the related trade-offs. Understanding this industry presents significant challenges, similar to the economic puzzles that emerged with the rise of big tech platforms or the development of open-source software in the early 2000s.

1.1 Relevant literature

This paper engages with three main bodies of literature: regulatory frameworks for frontier AI models; competition policy for the technological sector; and the relationship between regulation and antitrust.

1.1.1 AI regulation

When a technology can do significantly good but also significantly harm, the optimal deployment rate may be slower, as society may learn about the risks during deployment (Acemoglu and Lensman, 2023). Deployment should potentially also be delayed until further investments in safety because, when welfare levels rise, the risks become more significant compared to the value of the technology (Jones, 2016; Jones, 2023).

Recently, regulatory proposals have increasingly focused on frontier AI models that require large training runs with AI accelerators — chips specifically designed for training or inference of machine learning models. These training runs are typically characterized by the substantial number of Floating Point Operations (FLOPs) used and are usually benchmarked against existing deployed products and empirical patterns of how performance increases with model size to predict their potential capabilities.

For example, Biden’s AI executive order defines “dual-use foundation models” as models that used more than 10^23 FLOPs if trained with biological sequence data or 10^26 FLOP otherwise (White House, 2023). AI governance proposals include permitting, which requires actors to meet certain safety criteria to obtain licenses (see, e.g., Higgins, 2023); auditing, involving external reviews of AI systems for regulatory compliance (Mökander et al., 2023); liability regimes, which establish accountability in cases where AI causes harm (see, e.g., Llorca et al., 2023); information sharing and incident reporting (see, e.g., Stafford and Trager, 2022); compute taxation or subsidy mechanisms designed to incentivize resource allocation toward safety-conscious AI development (see, e.g., Jensen et al., 2023); and regulatory markets (Hadfield and Clark, 2023).

1.1.2 Competition policy in the technological sector

The AI supply chain includes one of society’s most complicated technologies, is capital intensive and concentrated. For instance, ASML is the single provider of extreme-ultraviolet machines (EUV) lithography machines needed for AI chip production, TSMC and Samsung are the single companies capable of building the most advanced AI accelerators—specialized chips for AI training —, and NVIDIA is the single market supplier of frontier GPUs.

There are also a lot of vertical integration and strategic partnerships that resemble vertical integration in the frontier AI labs. Microsoft has stakes in two of the most advanced AI labs—Inflection and OpenAI – (Silicon, 2023), while Alphabet is the owner of DeepMind and has a stake in Anthropic (Bloomberg, 2023). They are also major players in the cloud computing market and develop in-house advanced AI applications (Allied Market Research, 2023).

Google, additionally, designs its own AI accelerators called Tensor Processing Units (Reuters, 2023), with Microsoft reportedly following this trend of creating its own chips for deep learning tasks (Reuters, 2023). Apple, Meta, and Amazon are also deeply involved in different steps of the AI supply chain (see, e.g., Rikap, 2023). This indicates that, similar to the hardware and software industries (see, e.g., Shy, 2001; Tirole, 2023), high fixed costs, low marginal costs, network externalities, and product differentiation are prevalent, raising concerns about entrenched market power.

However, there is yet substantial uncertainty about how to best understand the market structure and competition dynamics of different steps of the AI supply chain. Vipra and Korinek (2023) have argued that the cost development of foundation models and the associated necessary infrastructure make it resemble a natural monopoly, suggesting a path towards regulation as a utility like electricity and transit.

However, as this is not a yet consolidated market that the role of, e.g., product differentiation and contestability will have, the scenario remains very uncertain. In a roundtable on competition policy and generative AI, Acemoglu argued for antitrust laws to foster alternatives to dominant tech companies and reduce their social and economic power.

Athey, the current Chief Economist of the Antitrust Division at the U.S. Department of Justice, emphasized the challenge's resemblance to the rise of multi-sided markets and platforms. Lina M. Khan, in her paper "Amazon’s Antitrust Paradox" (2017), argued that conglomerate and vertical integration by big tech should be analyzed for their dynamic effects on market structure.

Since becoming chair of the FTC, Khan has challenged Microsoft's acquisition of Blizzard, Meta's acquisition of a VR startup, and has opened litigation against Google and Amazon. Her leadership marks a significant shift in U.S. antitrust policy, especially regarding the tech sector. The OECD has published a paper on "Theories of Harm for Digital Mergers," highlighting ecosystem-based and privacy-focused theories and incorporating long-term effects in competition policy. How these perspectives will shape competition authorities' approach to foundation model markets remains uncertain.

1.1.3 Interplay between regulation and antitrust

While AI safety considerations would probably fall outside the scope of antitrust enforcement, it is crucial to examine how competition policies could influence regulatory proposals in the AI industry. Market structure, for example, can impact the level of R&D investment in an industry (see, e.g., Armour and Teece, 1980), suggesting that antitrust policies can affect the rate at which frontier AI systems evolve.

The impact of vertical integration on R&D is theoretically ambiguous, demanding empirical investigation into the specificities of the AI supply chain. Information sharing and incident reporting policies between companies in the industry may also raise collusion concerns by competition authorities. Increased vertical integration might, by default, lead to less public information about the industry, strengthen the industry lobby, inflate profit margins, and result in greater power accumulation.

Conversely, a highly vertically integrated market could potentially facilitate the diffusion of safety standards and enhance the capacity for a timely, coordinated response to risks arising from the training or deployment of foundation models. Additionally, the vertical relationships and contracts established between companies in a supply chain with oligopolistic aspects at each level of the chain, as extensively discussed by Lee et al (2021).

This points to the possible necessity of structural remedies in certain regulatory proposals. As suggested by Narechania and Sitaraman (2023), regulations could potentially mandate the separation of various business activities within a single AI firm, such as the design of foundation models and the ownership of the data centers where they are trained. As the relationship between industry integration and safety remains unclear, further research is needed on the topic.

1.2 Limitations

While this paper provides a comprehensive overview of vertical and horizontal integration within the AI supply chain, it has several limitations.

Firstly, the rapidly evolving nature of AI technologies and policies can quickly outdated some of our findings.

Secondly, the paper focuses on major players and high-value transactions, which may not capture the full diversity of the AI landscape, including smaller entities and emerging markets.

Thirdly, we decided to exclude China from our analysis driven by challenges in accessing reliable data, and significant regulatory and policy differences. Fourthly, our study is mostly confined to available data and published research as well as conversations with experts anonymously, and may not reflect undisclosed strategic partnerships or unpublished technical developments.

Author:

Tomás Aguirre

This paper is