If you’re still waiting for a crash, you’ve missed the exit. The collapse of legacy finance isn’t loud — it’s quiet. Predictable. Systemic.

In Turkey, the lira continues its downward spiral amid double-digit inflation. In Argentina, year-on-year inflation passed 140% in early 2025. In the U.S., a

debt load topping $35 trillion and ongoing rate manipulations have eroded trust in the dollar. This isn’t a localized crisis. It’s a global erosion of confidence.The institutions we once trusted — banks, central banks, sovereign treasuries — now appear less like guardians and more like liabilities. People around the world are searching for a financial system that isn’t hostage to politics, printing presses, or inflationary cycles.

One asset keeps emerging as the alternative: Bitcoin.

The end of trust-as-a-model

For most of the 20th century, economic policy was anchored in trust. Trust in central banks to manage inflation. Trust in commercial banks to guard deposits. Trust in policymakers to steer economies out of crisis.

But trust is fragile. And in the digital age, it’s increasingly optional.

According to the

The outcome is familiar:

- Currencies lose purchasing power

- Savings decay

- Asset bubbles inflate

- Systemic risk increases

In this context, Bitcoin is not just a speculative asset. It’s an engineered alternative — an escape route.

Bitcoin: engineered for distrust

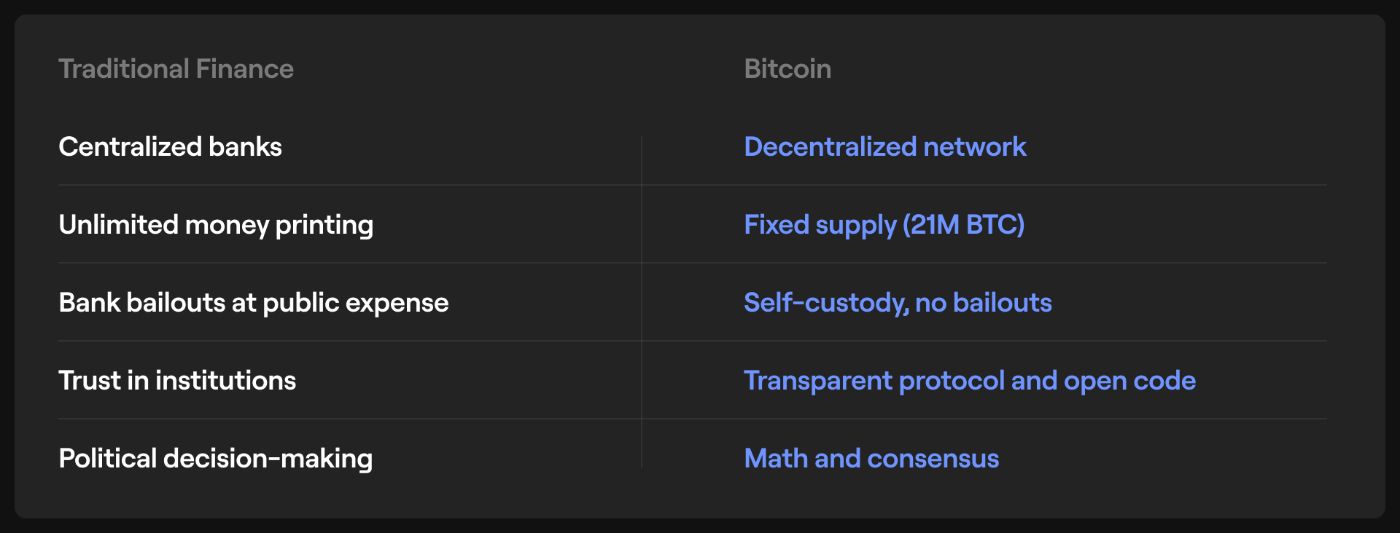

Launched in 2009, Bitcoin isn’t a financial product. It’s a protocol — a decentralized alternative to trust-based money. Its supply is fixed. Its governance is distributed. Its ledger is public.

As of mid-2025, Bitcoin commands over 50% of the total digital asset market, with a market cap nearing $1.4 trillion. Institutional flows reached $8.2 billion in Q1 2025, with investments from BlackRock, Fidelity, and Franklin Templeton.

Bitcoin is no longer just a bet on volatility. It’s becoming a hedge against coordinated monetary dysfunction.

Quiet exits, global moves

The shift has already begun — quietly, but undeniably.

El Salvador adopted Bitcoin as legal tender in 2021. By 2025, over 30% of households have used it for remittances, savings, or everyday transactions.

In Nigeria, banking freezes and currency controls have accelerated peer-to-peer Bitcoin adoption.

Corporates like MicroStrategy now hold over 200,000 BTC on their balance sheet. Tesla has resumed Bitcoin payments. Public companies increasingly treat BTC not as a gamble, but as a treasury standard.

They didn’t wait for permission. They moved early. As noted in Fidelity’s 2025 report, allocation to Bitcoin is now ‘less about growth and more about sovereignty.’

From system dependency to protocol logic

Traditional finance is built on layers of dependency — bank permissions, legal restrictions, central control. Bitcoin is built on consensus, code, and a fixed supply. When trust collapses, protocol logic takes over.

Bitcoin wasn’t built to replace your bank. It was built so you don’t need to ask one

So the question isn’t whether crypto will survive. It’s whether fiat dominance can.

Whether you're in Lagos or London, Buenos Aires or Berlin — the future of money isn’t something you wait for. It’s something you build.

This isn’t a trend. It’s a redesign. And it’s already underway.

Have you already begun your quiet exit from the legacy financial system? Or are you just getting started?

Or maybe you still believe in the old model — if so, share why you think it deserves to stay.

[story continues]

tags