It’s not "digital cash"—it's a control system designed to monitor your spending, enforce expiration dates on your savings, and blacklist dissenters.

A recent EU-wide survey by the European Central Bank (ECB) and the German Bundesbank revealed a clear lack of public support for a digital euro.

The majority of citizens are either unaware of the project or actively opposed to it. For example, in Germany, 59% are unaware, and in Slovakia, over 70% aren't open to it.

The message from Europe's citizens is a unified,

"Don't do it!"

Yet, the EU is pressing forward. The ECB has announced the first version of the Central Bank Digital Currency (CBDC) will be released as early as the fourth quarter of this year.

Digital Euro: Lipstick on a Pig

The ECB's marketing pitch is simple: the digital euro means modernization and innovation. It's described as "digital cash," allowing transactions via your phone.

But wait—is that true?

EU citizens have been using digital euros for decades. The vast majority of transactions are already managed online; very few of us rely solely on physical cash or ATMs anymore.

This isn't about "digital cash," and it certainly isn't about innovation. The digital euro is built on the same infrastructure as the current euro. The changes are purely cosmetic. It will be run, and presumably printed to oblivion, by the same bureaucrats who control the old euro.

In short, the digital euro is lipstick on a pig.

The Official Narrative vs. Reality: The Debt Problem

So, what is the real agenda behind this urgent push?

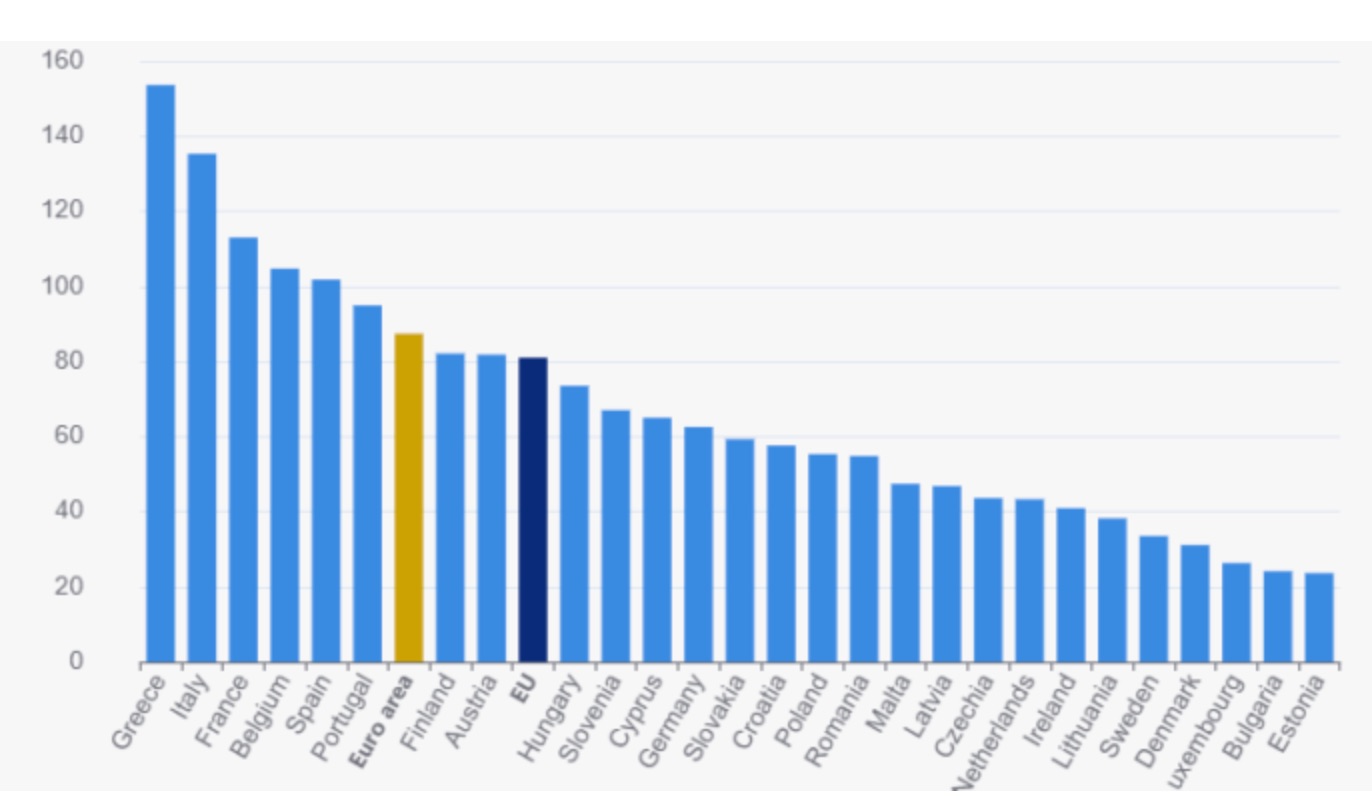

Look no further than Europe’s debt. The Euro area’s public debt was nearly 88% of GDP in Q1 2025.

Countries like Greece (152.5%), Italy (138%), and France (114%) are swimming far past the old "Maastricht comfort levels."

When debt and deficits strain economies, capital flight becomes the greatest enemy of the state.

They need to control your transactions.

This control could manifest through features designed to keep your money exactly where the state wants it:

- Holding Limits: Restricting the total amount of money you can possess.

- Geo-Fencing: Restricting spending outside a specific geographical area.

- Time-Based Rules: Imposing expiration dates on your savings or funds.

- Real-Time Monitoring: Complete, instant surveillance of every single transaction.

In other words, the digital euro gives the ECB a "switchboard" to control your money, like an app controlling your household lights.

A Digital Prison Disguised as Convenience

Under the guise of the "fast, convenient, and sexy" new euro, the ECB is pushing a Chinese-style social credit system in the EU.

This system allows them to write the rules and get instant, enforced compliance.

Imagine this:

- Climate change compliance? "Sorry, your carbon footprint budget has been used up for this week. No more purchases allowed."

- You criticized the government? "Sorry, your wallet account is closed."

It’s a digital prison disguised as modernization. Welcome to the future you never asked for.

Sound far-fetched?

In China, the primary inspiration for the ECB, more than 24 million people are already blacklisted by the social credit system for ambiguous reasons. They can no longer send or receive money, or even buy a train ticket.

It's precisely these concerns that led the US government to move to ban CBDCs through the Anti-CBDC Surveillance State Act. But the EU is going forward anyway.

The Only Way Out: Bitcoin

There is only one robust way out right now:

Bitcoin.

With Bitcoin, you can escape money expiration, censorship, and bypass the inflation caused by new banking bailouts. You can transact without permission, and unelected officials at the ECB cannot freeze your funds.

Bitcoin is an authentic form of real resistance against digital dictatorship. It is free speech money, a parallel financial rail that stays open all the time.

Final Thought

The question is, are you interested in giving more power to unelected bureaucrats for your perceived convenience, or are you interested in sustaining your freedoms?

The choice is yours.

[story continues]

tags