Table Of Links

DISCUSSION

The Discussion section aims to contextualize and synthesize the findings of our research, examining their implications for the African startup ecosystem and highlighting potential avenues for further inquiry. In this study, we have unveiled critical insights regarding the impact of various factors on deal amounts in African startup investments, ranging from gender diversity and founder's academic background to the role of incubators, exit strategies, entrepreneurial experience, and sector preferences.

By dissecting these factors and understanding their influence on investment outcomes, we seek to contribute to the ongoing discourse on fostering a sustainable and thriving African startup ecosystem. The following subsections will delve into the implications of each finding, shedding light on potential areas for future research and policy interventions to address the challenges and harness the opportunities identified in this study.

Founder Related Factors:

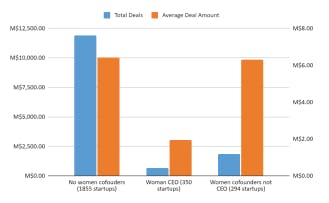

Women Impact on Investment:

Our analysis revealed a significant gender imbalance in the African startup ecosystem, with 75.2% of startups lacking female co-founders and a mere 10% having female CEOs. Interestingly, the presence of female-only founders, women co-founders, and women CEOs displayed a slight negative correlation with the deal amount. This finding raises concerns about the perceived value of gender diversity within the ecosystem and highlights the existence of a considerable gender diversity gap that warrants further investigation and rectification.

Furthermore, when comparing the average deal amounts raised by startups with women CEOs and those with women co-founders, our findings suggest that the increasing policies supporting women entrepreneurs in African countries [9] may inadvertently lead to negative consequences, such as tokenism. To address these issues, policymakers should consider devising targeted interventions that not only foster female entrepreneurship but also promote a genuine appreciation for gender diversity in the startup ecosystem.

Additionally, efforts should be made to ensure that funding decisions are based on merit and the potential for success, rather than merely fulfilling diversity quotas. Future research should investigate the relationship between these policies and the observed discrepancy in deal amounts, to better understand the underlying dynamics and inform more effective policy interventions for promoting genuine gender equality and inclusion.

CEO graduation year:

Our investigation revealed a negative correlation between this variable and the transaction size, indicating that entrepreneurs with greater experience are potentially more adept at securing funding. This finding may be attributed to the difference between necessity and opportunity-driven entrepreneurship [10]. The implications of this observation encompass a wider inquiry into the significance of entrepreneurial experience in the African startup arena and the probable trade-offs between experience and innovation.

Policymakers and investors should endeavor to devise mechanisms that foster the growth of both experienced entrepreneurs and young innovators, recognizing that different types of entrepreneurs may contribute divergently to the ecosystem's advancement and fortitude

CEO university impact: The results of our study demonstrated a higher probability of African startup fundraising by founders with North American academic backgrounds.

Nonetheless, it is vital to emphasize that this correlation does not invariably guarantee startup triumph. This discovery raises inquiries regarding the impact of global exposure and the potential effects of academic history on investment possibilities in Africa. Further investigation is warranted to elucidate whether this tendency is propelled by networking prospects, perceived reputation, or other education-related factors, and how these elements can be harnessed to enhance the African startup ecosystem.

Company Related Factors:

Human capital importance:

Our analysis revealed that both features: the number of founders and the number of employees are highly positively correlated with the deal amount. This finding highlights the significance of human capital in securing funding for African startups, as investors seem to value the presence of a competent and diverse team in their investment decisions.

Startups with more founders and employees may be perceived to have a higher potential for innovation, operational efficiency, and scalability, which could enhance their attractiveness to investors [11]. Hence, it is recommended that policymakers and investors prioritize policies that foster human capital development in startups, including training programs for entrepreneurs and their employees, and policies that encourage diverse founding teams.

Sector impact:

The fintech industry emerged as the most prominent sector; however, it was not a strong predictor of the transaction size. The top five sectors align with the challenges and opportunities for innovation and growth on the continent. This outcome indicates that while some sectors may garner more investment and attention, other sectors may possess the untapped potential for expansion and progress.

A more diversified and equitable approach to investments in specific sectors may contribute to fostering a more resilient and comprehensive startup ecosystem in Africa. Additional research should delve into the constituents that propel the attractiveness of specific sectors and assess how such insights can guide investment strategies and policy interventions.

Country Impact:

Our analysis revealed negligible correlation between country and deal amounts in African startup investments, despite differences in various country-level indices, such as GDP per capita, corruption indices, ease of doing business, and economic development. Additionally, the analysis revealed a strong correspondence between the number of startups and the total sum of deals in each country, with the top four countries—Nigeria, Kenya, South Africa, and Egypt—emerging as prominent technology hubs in Africa.

Interestingly, when examining the average deal amount per country, Algeria emerged as the top country, while Tunisia 3 4 took the lead in terms of the maximum deal amount. These findings prompt questions about the factors that may contribute to the observed discrepancies in deal amounts among different countries and the implications for the broader African startup ecosystem.

One plausible explanation for the higher average and maximum deal amounts in Algeria and Tunisia may be their proximity to Europe, which could facilitate access to European markets, investors, and resources. Moreover, while the 4 African tech-hubs seem to foster more startup investments overall, they may not be providing the necessary infrastructure for these startups to scale significantly.

Based on these findings, policymakers should consider implementing targeted strategies to promote cross-border collaboration and facilitate access to international markets, investors, and resources. By fostering such connections, African countries can better leverage their geographical advantages and enhance the growth and sustainability of their respective startup ecosystems.

Future research should investigate the underlying factors of this lack of correlation and examine the drivers of success in countries with higher average or maximum deal amounts. Identifying these drivers can help stakeholders develop targeted strategies to support the growth and sustainability of Africa's startup ecosystem.

I**nvestment Related Factors:**

Y Combinator's role:

Albeit our findings did not reveal a significant influence of Y Combinator on the transaction size, the US accelerator asserts that its supported startups raise 2.5 times higher valuation after participating in their program and that 4% of their companies became unicorns . This disparity 5 necessitates further exploration to comprehend the function of incubators and accelerators in the African startup milieu.

A productive avenue for research would entail an examination of the constituents that contribute to the success of Y Combinator-sponsored startups and an inquiry into how such insights can inform the development and execution of incubator and accelerator programs in Africa.

Exit impact:

Exit strategies play a crucial role in startup investment, as they provide a mechanism for early-stage investors (notable VC firms) to realize their returns on investment. Our analysis revealed a strong positive correlation between the potential for a lucrative exit and the transaction size. However, our analysis showed that there is a dearth of successful exit deals (less than 1%), creating challenges for startups seeking funding and investors seeking returns.

This may be due to a variety of factors, including a lack of established companies with the resources to acquire startups, limited public market access, and limited infrastructure for initial public offerings (IPOs) or mergers and acquisitions (M&A). Therefore, to foster a more sustainable startup ecosystem in Africa, policymakers and investors should consider implementing strategies that facilitate the creation of a more conducive environment for successful exits.

This may include supporting the growth of large companies and the development of public markets, as well as creating more avenues for mergers and acquisitions or other exit mechanisms. By promoting a more robust exit ecosystem, stakeholders can incentivize investors to fund more startups and provide entrepreneurs with the resources they need to grow their businesses.

Type of investment impact:

During the investigation of the relationship between the type of investment and deal amounts in African startup investments, the present study found limited evidence of a significant impact of investment type on the deal amounts. Surprisingly, the study observed substantial inconsistency in the amounts per type of investment, particularly for the primary types of investments, including Pre-seed, Seed, Series A, Series B, Series C, and Series E. Notably, these investments are typically announced as "venture rounds" rather than being properly labeled with their respective investment types.

This observation raises pertinent questions regarding the potential consequences of such ambiguity on investment decisions and the overall health of the ecosystem. The lack of clarity and consistency in the classification of investment stages may lead to discrepancies in investor expectations, founder valuations, and the allocation of resources. Consequently, this may result in inefficient deployment of capital and suboptimal growth for startups in the African continent.

Future research should investigate the factors contributing to this inconsistency and explore potential solutions to standardize the classification of investment stages in the African startup ecosystem. By promoting a more consistent and transparent approach to investment categorization, stakeholders can facilitate informed decision-making, foster investor confidence, and support the development of a more robust and sustainable startup landscape in Africa.

Author:

This paper is

[story continues]

tags