Table of Links

-

Introduction

1.1 Periodic auction and continuous limit order book

1.2 Comparison and main flaws of limit order book

1.3 Optimal policies to cure auction’s inefficiencies and related works

-

Auctions market modeling with transaction fees and randomization

2.1 The market characteristics

2.3 Strategic Trader’s optimization and market quality

2.4 Data and numerical analysis

2.5 Strategic trader with full information: efficient but unfair market

-

Monitoring policies: transaction fees and clearing time randomization

3.1 Bilevel optimization between the exchange and the strategic trader

3.2 Randomization without fees

3.3 Optimal transaction fees indexed on time to improve price impact for the trader

A. Appendix: Numerical Methods

A.1 Problem of a Strategic Seller

A.2 Appendix: Problem of the Regulator

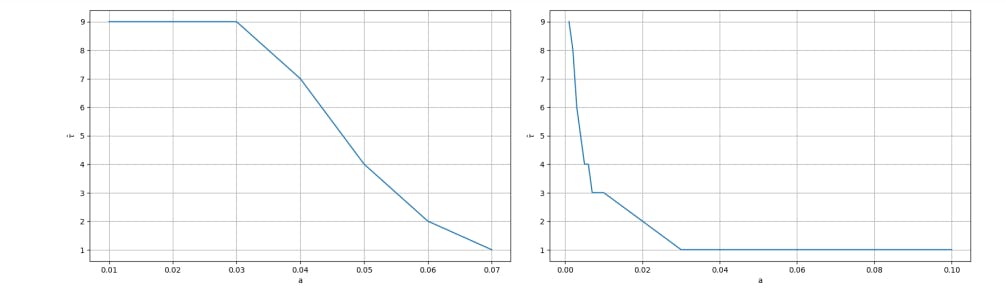

B Appendix: Illustrate Remark 2.4

2.1 The market characteristics

We consider an auction to trade a risky asset starting at time 0 with duration 𝑇

0 T>0. We denote by 𝑃 𝑇 𝑐 𝑙 P T cl the clearing price of the auction determined by the exchange to maximize the number of trades at the clearing time 𝑇 T. During the auction’s duration, limit orders arrived such that each limit order 𝑖 i is characterized by a limit price 𝑃 𝑖 P i at which a trader is willing to buy or sell the asset and a volume determined by a supply function 𝑄 𝑖

𝐾 ( 𝑃 𝑇 𝑐 𝑙 − 𝑃 𝑖 ) Q i =K(P T cl −P i ). The parameter 𝐾

0 K>0 is the slope of the supply function assumed to be fixed for each limit order. We assume that ( 𝑃 𝑖 ) 𝑖 ≥ 1 (P i ) i≥1 is a family of independent normally distributed random variables with mean 𝜇 𝑚 𝑚 μ mm and standard deviation 𝜎 𝑚 𝑚 σ mm .

Note that if 𝑄 𝑖 ≤ 0 Q i ≤0, the order is a buying order; if 𝑄 𝑖 ≥ 0 Q i ≥0, the order is a selling order. We assume that the efficient price of the risky asset denoted by 𝑃 ∗ P ∗ is a normal random variable with mean 𝜇 ∗ μ ∗ and standard deviation 𝜎 ∗ σ ∗ . We assume 𝜇 𝑚 𝑚

𝜇 ∗ μ mm =μ ∗ and 𝜎 𝑚 𝑚

𝜎 ∗ 𝜎 σ mm =σ ∗ =σ, for some 𝜎

0 σ>0. We model the arrival of these limit orders by a Poisson process 𝑀 M with intensity 𝜆 𝑡

𝜆 × 𝑡 λ t =λ×t where 𝜆 λ is a positive constant. In other words, 𝑁 𝑡 :

𝑀 𝑡 + 1 N t :=M t +1 denotes the number of market makers active in the auction up to time 𝑡 t. We model this process as limit orders pre-existing in a CLOB, set by market makers and sent continuously in the coexistence system of CLOB and auction market. These limit orders have been set in the CLOB and are transferred to the auction for execution as block trades.

We define a family of 𝜎 σ-algebras 𝐹

{ 𝐹 𝑡 } 0 ≤ 𝑡 ≤ 𝑇 F={F t } 0≤t≤T generated by the available information up to time 𝑡 t and composed with the number of limit orders arrived in the auction and their limit prices 𝑃 𝑖 P i , that is

𝐹 𝑡 : 𝜎 { 𝑁 𝑡 , ( 𝑃 𝑖 ) 𝑖 1 𝑁 𝑡 } . F t :=σ{N t ,(P i ) i=1 N t }.

We consider a strategic seller joining the auction at a deterministic time 𝜏 τ between 0 and 𝑇 T aiming at optimally liquidating her position in the risky asset. The strategic seller controls the exact time 𝜏 τ she arrives in the auction together with the price 𝑃 P at which she is willing to sell the asset, and the direction of the trade (which is selling). In this case, the volume sent by this strategic seller is 𝑄

𝐾 ( 𝑃 𝑇 𝑐 𝑙 − 𝑃 ) Q=K(P T cl −P). We assume that the price 𝑃

𝑃 𝜏 𝜇 P=P τ μ, sent at time 𝜏 τ in the auction, is a normal distribution with mean 𝜇 μ where 𝜇 μ is a random variable controlled by the seller and variance 𝜎 2 σ 2 fixed measurable with respect to the information available for the trader. Note that while the variance for the market makers and the strategic seller are the same for the sake of simplicity, the strategic trader knows up to time 𝑡 t the number of arrivals 𝑁 𝑡 N t and the prices of these orders { 𝑃 𝑖 } 𝑖

1 𝑁 𝑡 {P i } i=1 N t

In particular, the strategic trader may be imperfectly informed about the efficient price of the asset since 𝜇 μ is determined through 𝐹 F which does not take into account the efficient price. The seller uses the information available at time 𝑡 t to determine 𝜇 𝑡 μ t , so 𝜇 μ could be viewed as a function 𝜇 𝑡

𝜇 ( 𝑡 , 𝑁 𝑡 , { 𝑃 𝑖 } 𝑖 1 𝑁 𝑡 ) μ t =μ(t,N t ,{P i } i=1 N t ).

By denoting 𝑃 𝑡 𝜇 P t μ the price the seller proposes entering in the auction at time 𝑡 t, we assume that 𝑃 𝑡 𝜇 P t μ is a normal distribution 𝑁 ( 𝜇 ( 𝑡 , 𝑁 𝑡 , { 𝑃 𝑖 } 𝑖

1 𝑁 𝑡 ) , 𝜎 2 ) N(μ(t,N t ,{P i } i=1 N t ),σ 2 ) where the function 𝜇 μ is controlled by the strategic seller when she enters at time 𝑡 t and sees 𝑁 𝑡 N t arrivals with associated price { 𝑃 𝑖 } 𝑖

1 𝑁 𝑡 {P i } i=1 N t

Since the strategic seller controls the direction she trades, her order would not be executed if 𝑃 𝑇 𝑐 𝑙 < 𝑃 𝑡 𝜇 P T cl <P t μ . However, since all other market makers do not control the directions of their trades, their orders will be executed for sure. The quantity the strategic seller trades is thus given by 𝐾 ( 𝑃 𝑇 𝑐 𝑙 − 𝑃 𝑡 𝜇 ) K(P T cl −P t μ ) if 𝑃 𝑇 𝑐 𝑙

𝑃 𝑡 𝜇 P T cl

P t μ , and 0 otherwise.

The strategic trader does not necessarily know exactly the mean 𝜇 ∗ μ ∗ of the efficient price and the mean 𝜇 𝑚 𝑚 μ mm of other transferred limit orders. We denote by 𝜇 𝑔 ∗ μ g ∗ and 𝜇 𝑔 𝑚 𝑚 μ g mm the estimations the strategic trader of 𝜇 ∗ μ ∗ and 𝜇 𝑚 𝑚 μ mm respectively. We denote by 𝐸 𝑔 E g the expectation when the mean of 𝑃 ∗ P ∗ and 𝑃 𝑖 P i corresponds to these estimations and we denote by 𝐸 E the expectation in the case 𝜇 𝑔

𝜇 ∗ μ g =μ ∗ and 𝜇 𝑔 𝑚 𝑚

𝜇 𝑚 𝑚 μ g mm =μ mm.

2.2 Clearing Price rule

The clearing price of an auction is set to maximize trading volumes. When there is no strategic trader, corresponding to the case when no traders control the direction of the proposed prices, this clearing price is the equilibrium between supply and demand, see [Du and Zhu (2017)] or [Jusselin et al. (2021), Section 2.3]. That is

which sets the clearing price to eliminate any imbalance between buy and sell orders.

Proposition 2.1. The clearing price of the auction is determined by

The clearing price (2.2) could also be written as:

Authors:

(1) Thibaut Mastrolia, UC Berkeley, Department of Industrial Engineering and Operations Research ([email protected]);

(2) Tianrui Xu, UC Berkeley, Department of Mathematics ([email protected]).

This paper is

[1] Here, "+1" practically means that there is at least one trader in the auction market for it to be open and theoretically to avoid division by zero. This assumption is consistent with the existence of liquidity in a CLOB transferred to an auction at for example the end of the day, see [Jusselin et al. (2021)].

[2] We could similarly assume that the strategic trader is a buyer but only consider the seller case motivated by optimal liquidation problem for the sake of simplicity.