Let's begin with an ancient problem

Borrower engagement remains frictional, especially if the borrower is an SME. Will digital engagement ever be non-frictional? Probably if you are listening to Spotify. Anything to do with commerce or money will need us to jump through a few hoops. But maybe we should not be thinking UI first. When we do so, our focus is on "how sleek my app is" or "hey, look, I spent a ton of design sprints on this and now....?" This is not thinking user first.

Walk into the stack

This is the way I believe the engagement should work. Every borrower should be able to walk into the stack. What does that mean?

Today the loan application process is one where the functions are abstracted into forms that potential borrowers fill in. There may be some documents you have to scan and upload. Before that, you need to onboard the application. This is time consuming and fragmented.

Of course, if you are seeking a personal loan from your bank and especially if you are card holder with a good credit history, things may be a bit faster. But we are talking about SMEs here.

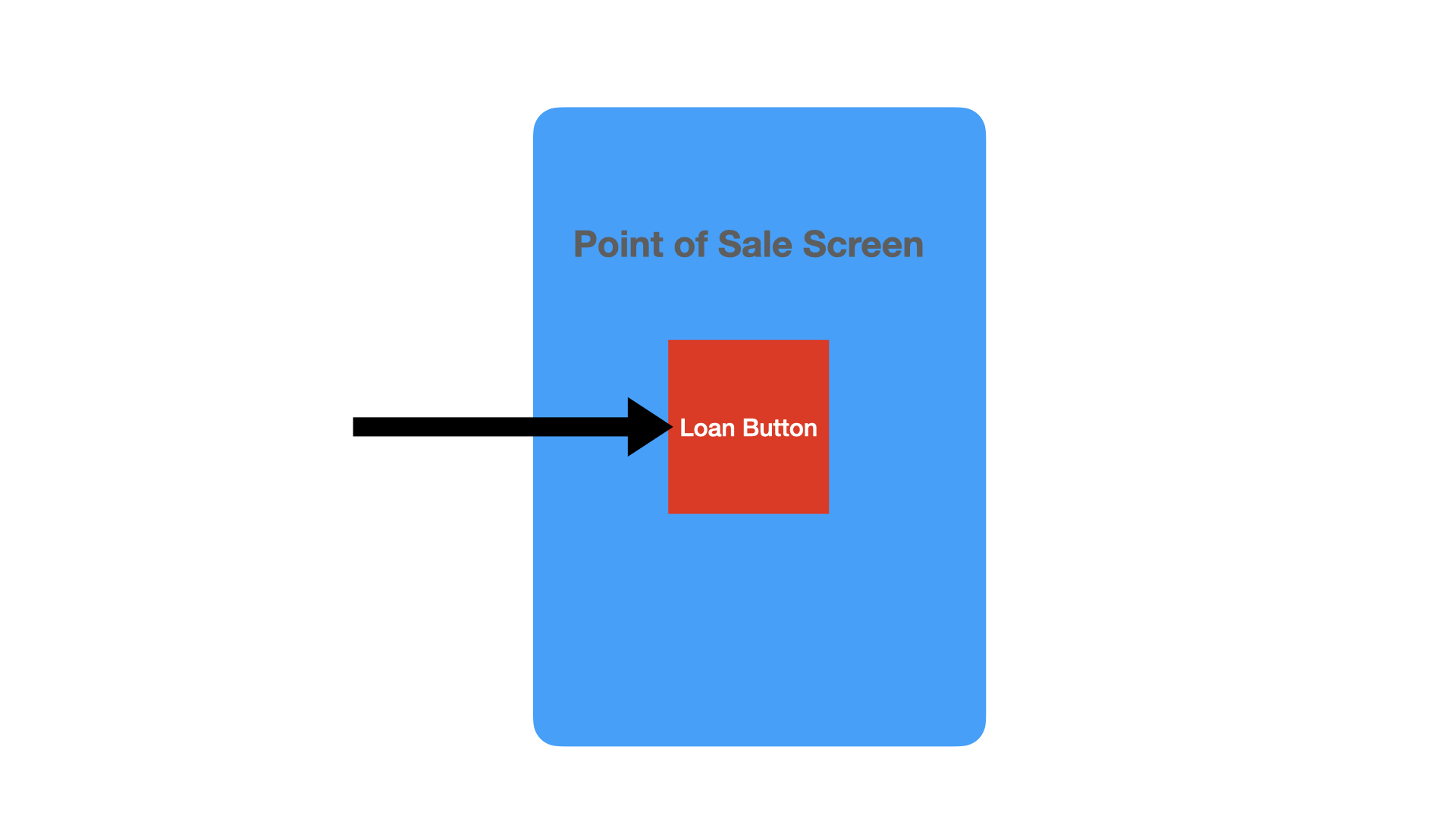

The SME should be able to enter the application directly from a bank terminal located at its end. Let me explain. Almost all merchants have a merchant app located on premise. Usually it is a hardware terminal which can be scanned to pay by QR or tapped to pay by card. In upcountry markets, that would mostly be a QR scan. Some value-added functions are also available such as voice alerts about payment.

A typical small upcountry business in Asia looks like this:-

And payments in many cases happen like this:-

Therefore, what a POS machine is like in a retail environment may differ quite a bit, based on country, city or town and the nature of business. My submission is that the entire lending process for SMEs should be embedded into existing POS and where necessary, new hardware rolled out. I have written about the reasons in a previous post here on Hackernoon.

Triggering a loan request

The SME owner should be able to log in to the terminal from his/her computer, enter a request for a loan and it should be processed. This would be a merchant view. There are some pre-requisites. The terminal should be hardwired to the SME computer or there should be an API that can be called. In most cases, the terminal would be connected to the POS machine of the merchant. A function on the POS terminal would suffice.

Once the application goes through, the lending algorithm should deliver the outcome in milli-seconds. In a previous Hackernoon post, I had mentioned how the approval might happen. The key thing here is this. If the merchant is using the POS and terminal, there should be no need to fill in long forms and upload documents. Just write the amount requested and the purpose of the loan in 2 boxes and push “Request”. The terminal is immediately recognised by the lender.

Precautions

Is there scope for misuse? There may be extreme cases of hijacking and enforced situations. If someone has stuck a gun at your head, you might be forced to apply for a loan. It is possible for the bank to put additional safeguards into place. For example, there can be a mandatory forty eight hour cooling period for the money to come into the account. The loan officer may place a mandatory call to the SME owner. This can lead to alerting the authorities in case something feels “off”. One might argue, of course, that a cooling-off period defeats the purpose of urgent financing. That is indeed true. A bank may choose to sanction a basic amount right away and then send the remaining amount after the cooling-off period. There can be other precautionary measures based on the resources of the bank.

Conclusions

Now, what rails would the loan application follow? If the local bank is the acquirer, then in that case it can be the acquiring rail itself. The coding has to ensure that a payment approval request is different from a merchant loan approval request and is sequestered accordingly. We will describe the merchant lending rail in another post.

An interesting sidebar to this would be in case of a merchant which accepts cards. It should be possible to set up merchant-side(B2B) financing using the same terminal that is used for customers. However, I am not going into the kernel engineering side of things here and what the costs might be. We will come back here as things expand.

[story continues]

tags