I’ve spent the last decade building and analyzing data-driven products in fintech and crypto, watching multiple market cycles from the inside — both as a participant and as someone who has to explain them to boards, clients, and teams. Now I lead Data & Analytics @ The Open Platform / Wallet in Telegram, and it’s not only personal but professional curiosity in the topic. The noise in this space is endless, so I wanted to create one structured analytical piece that cuts through the hype and gives a clear view of what matters right now. In this mid-2025 review, we’ll look at:

HackerNoon Editor’s note: This article is for informational purposes only and does not constitute investment advice. Cryptocurrencies are speculative, complex, and involve high risks. This can mean high prices volatility and potential loss of your initial investment. You should consider your financial situation, investment purposes, and consult with a financial advisor before making any investment decisions. The HackerNoon editorial team has only verified the story for grammatical accuracy and does not endorse or guarantee the accuracy, reliability, or completeness of the information stated in this article. #DYOR

-

Part 1. The big picture for crypto markets and macro conditions.

-

Part 2. Why Bitcoin still sets the tone.

-

Part 3. How DeFi has evolved into real infrastructure.

-

Part 4. Why stablecoins are now core financial rails.

-

Part 5. Circle’s IPO case: what it says about the industry’s maturity.

-

And finally, my view on the trends to watch next (instead of a Postscript)

Part 1. Market & Macro. Crypto hits new peaks. Again.

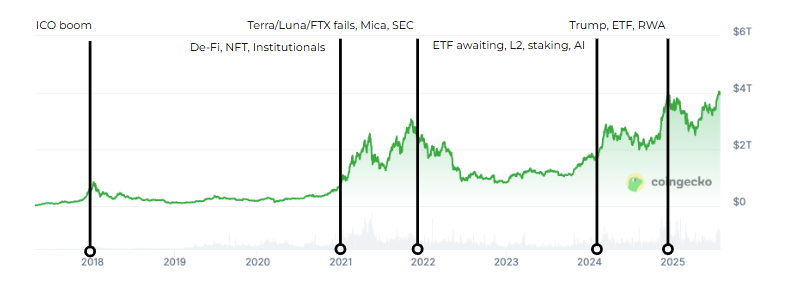

If you blinked between late 2024 and mid-2025, you missed a regime change. Crypto didn’t just “go up”. It grew up. The total market cap punched through $4T not because of one meme coin or one hype cycle, but because the infrastructure and rules got better at the same time retail and institutions finally met in the middle.

Think $4 trillion is just a big number? Put it on the scoreboard: that’s more than the UK makes in a year, about the same size as NVIDIA, and creeping into the weight class of entire economies. The U.S. GDP sits at $29T, China’s at $19T, gold glitters at $22T, and the S&P 500 towers at $54T. Crypto is no longer the weird internet cousin at the finance family dinner - it’s a guest at the grown-ups’ table, ordering steak and negotiating deals.

What Fueled the 2024 Crypto Rally? A cocktail of politics, policy, and product upgrades.

- Regulators blinked first. The SEC approved U.S. spot Bitcoin ETFs on Jan 10, 2024, bringing Bitcoin into mainstream brokerage menus. Spot Ether ETFs followed in July 2024. In July 2025, the SEC went further, permitting in-kind creations/redemptions for crypto ETPs - a big operational unlock for authorized participants.

- Macro turned from headwind to tailwind. The Fed’s 50 bps cut in Sep 2024 kicked off an easing cycle; the tone since has stayed progressively looser even as officials debate pace. Risk assets, including crypto, breathed easier.

- Bitcoin halved, again. The April 20–22, 2024 halving cut issuance from 6.25 to 3.125 BTC. Fewer new coins + ETF demand = structural bid.

- Politics mattered. The 2024 U.S. election delivered a more openly pro-crypto administration — and with it, friendlier rhetoric and legislative momentum. Markets noticed.

- Institutional and corporate demand. Companies and governments continued to accumulate crypto assets. Circle (USDC) had a VERY successful IPO.

- New users and channels. Memecoins and stablecoins drove new waves of crypto adoption, expanding the user base and unlocking novel distribution channels.

What’s happening in Global Economy 2025?

If you look at the bigger picture, crypto’s $4T isn’t random — it looks like a part of a shift. The US economy is slowing, China is adding stimulus, and Europe is picking up speed. Interest rates are coming down, deflation gives central banks more room to cut, and Wall Street isn’t excited but also not scared. That mix — cheaper money, global uncertainty, and people looking for alternatives — is perfect fuel for assets outside the usual playbook. Crypto became such asset.

For me, the signal is clear: we’re in one of those rare moments when the wind is at crypto’s back from all directions. Liquidity is better, the rules are a bit more predictable, and the old “too risky” argument feels out of touch. I’ve been through enough cycles to know nothing is guaranteed — but this time, it’s not just hype driving the market. It feels like the foundation is finally catching up with the vision. If that holds, we’re looking at more than just another rally — we’re watching crypto grow into a real part of the global financial toolkit.

Part 2. BTC in details (it is still king of the hill)

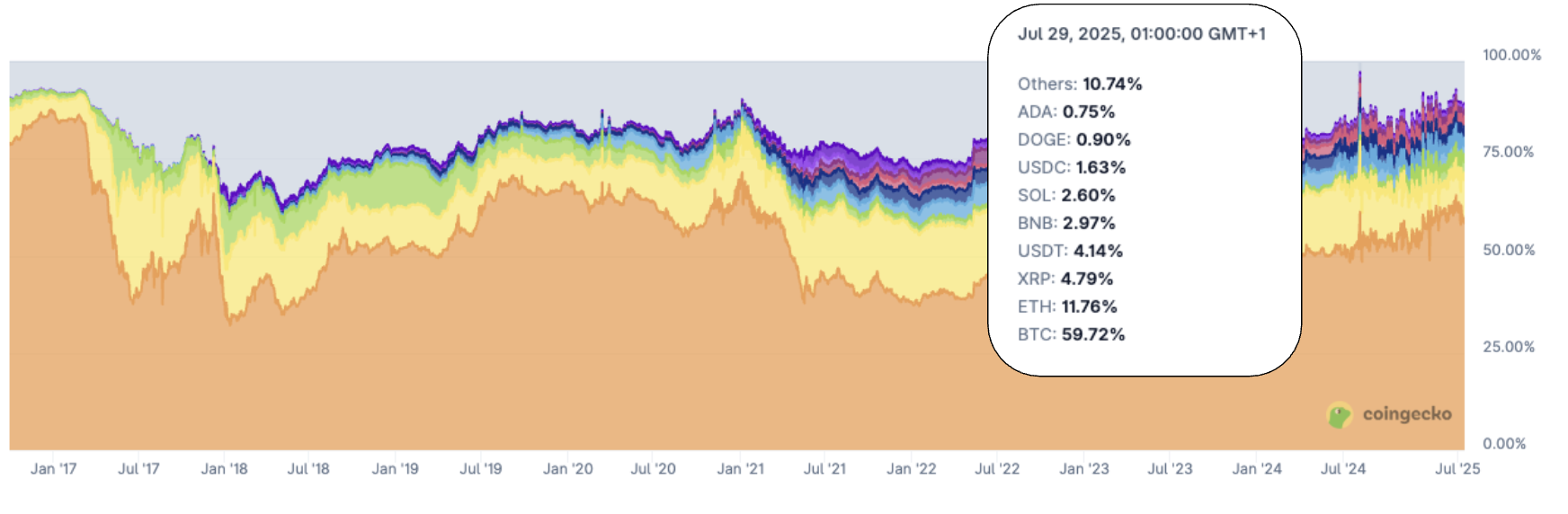

Bitcoin dominance is sitting close to 60% — the highest in years — and it’s not by accident. Every big move in the crypto market still dances to BTC’s rhythm. When Bitcoin goes up, liquidity floods in. When it stalls, the party slows down. That leadership role hasn’t changed, even with all the noise from altcoins, memecoins, and shiny new narratives.

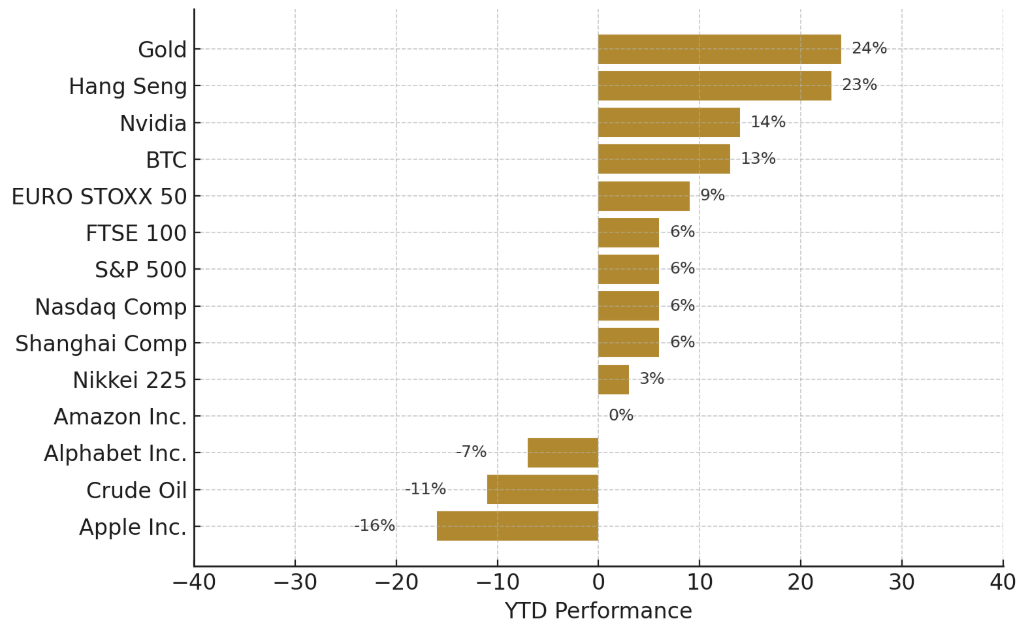

And it’s not just about market share. Despite a year full of macro shocks and uncertainty, BTC delivered +13% YTD by mid-2025 — beating the S&P 500, Nasdaq, and lots of tech giants. Meanwhile, during the recent month some alt coins like ETH almost doubled reaching almost all-time high.

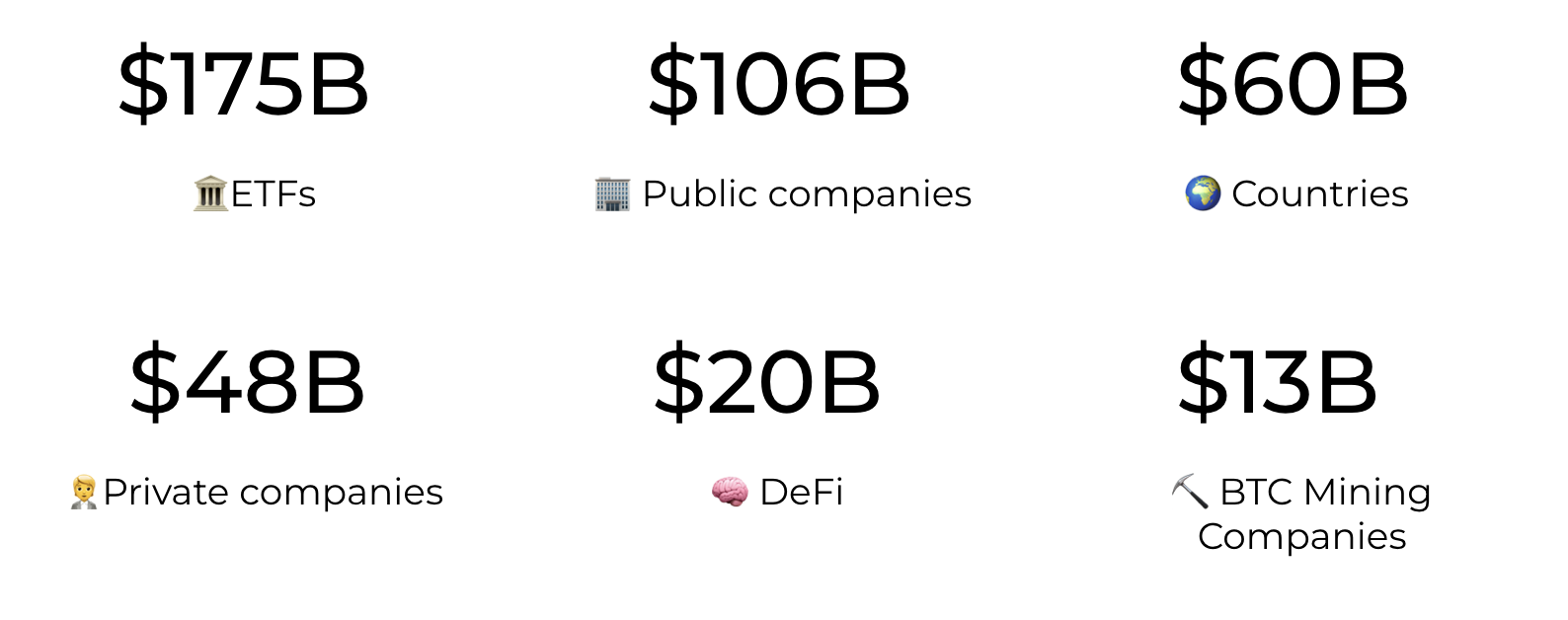

Zooming out geographically, North America remains the largest crypto market by value, with more than 70% of flows coming from institutional players. These aren’t degen traders — we’re talking hedge funds, corporates, and asset managers allocating at scale. ETFs have become the main rail for this capital, and the numbers prove it:

- $175B held via ETFs

- $106B in public company treasuries

- $60B by countries

- Plus billions in private companies, DeFi treasuries, and miners — in total, about $410B of BTC is in the hands of known large entities. That’s roughly the GDP of Norway (which is $484B as of 2024).

One of the best takes I’ve seen on Bitcoin’s role came from Binance Research (citing FRED): BTC isn’t just a store of value anymore — it’s becoming a macro signal. Historically, Bitcoin’s price momentum has led global manufacturing cycles by about 8–12 months. In February 2025, BTC momentum hit bottom and started climbing again, even while PMI data was still soft. If history repeats, we’re in that “mismatch phase” right now — with a full economic recovery lining up for late 2025 to early 2026.

Bitcoin remains the reference point for the entire digital asset space. Its dominance, institutional adoption, and historical links to broader macro trends make it a key asset to watch — not because it’s guaranteed to lead the next leg up, but because its movements often set the tone for risk appetite across crypto. Whether this role strengthens or fades will depend on how the market digests new products, regulations, and macro conditions over the coming year.

Part 3. DeFi Renaissance

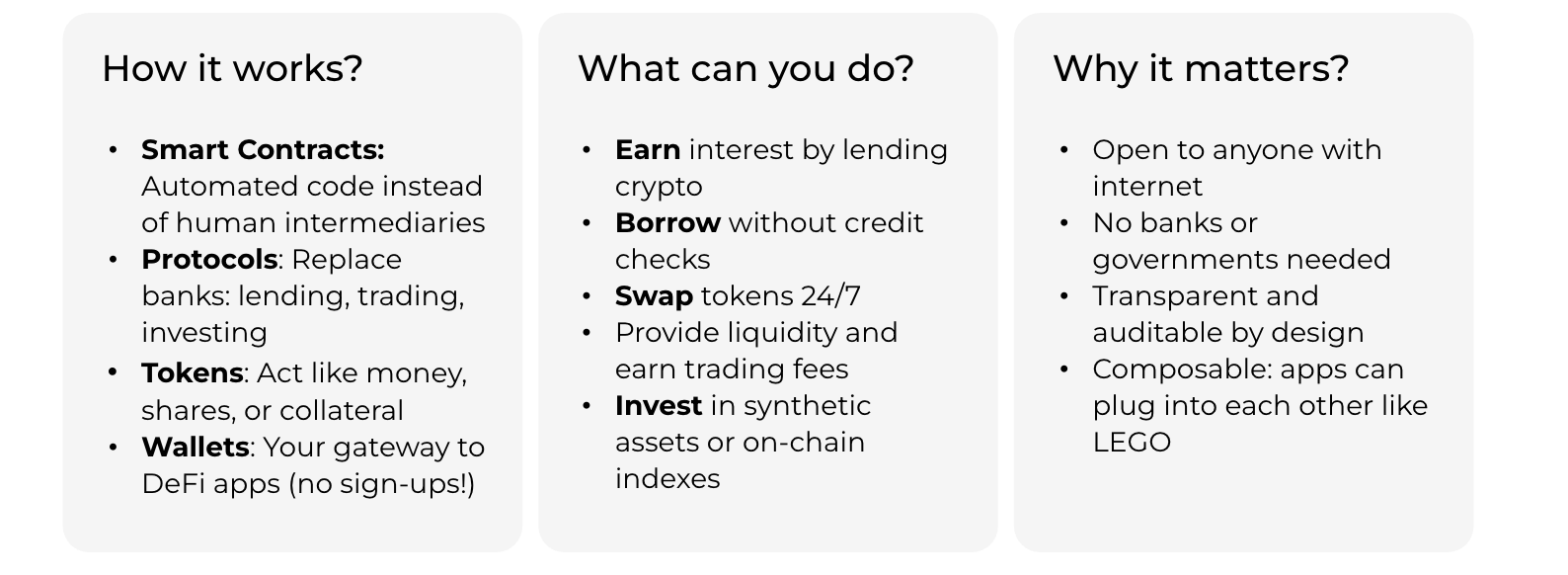

If Bitcoin is the anchor of crypto, DeFi is the lab — a place where new financial systems are built in the open, without banks or middlemen. At its core, DeFi (Decentralized Finance) replaces traditional intermediaries with smart contracts and open protocols, letting anyone with an internet connection lend, borrow, trade, or invest directly on-chain. The fewer steps, the faster people hit first value (on a personal note, it aligns with what we measure in onboarding funnels at Wallet in Telegram).

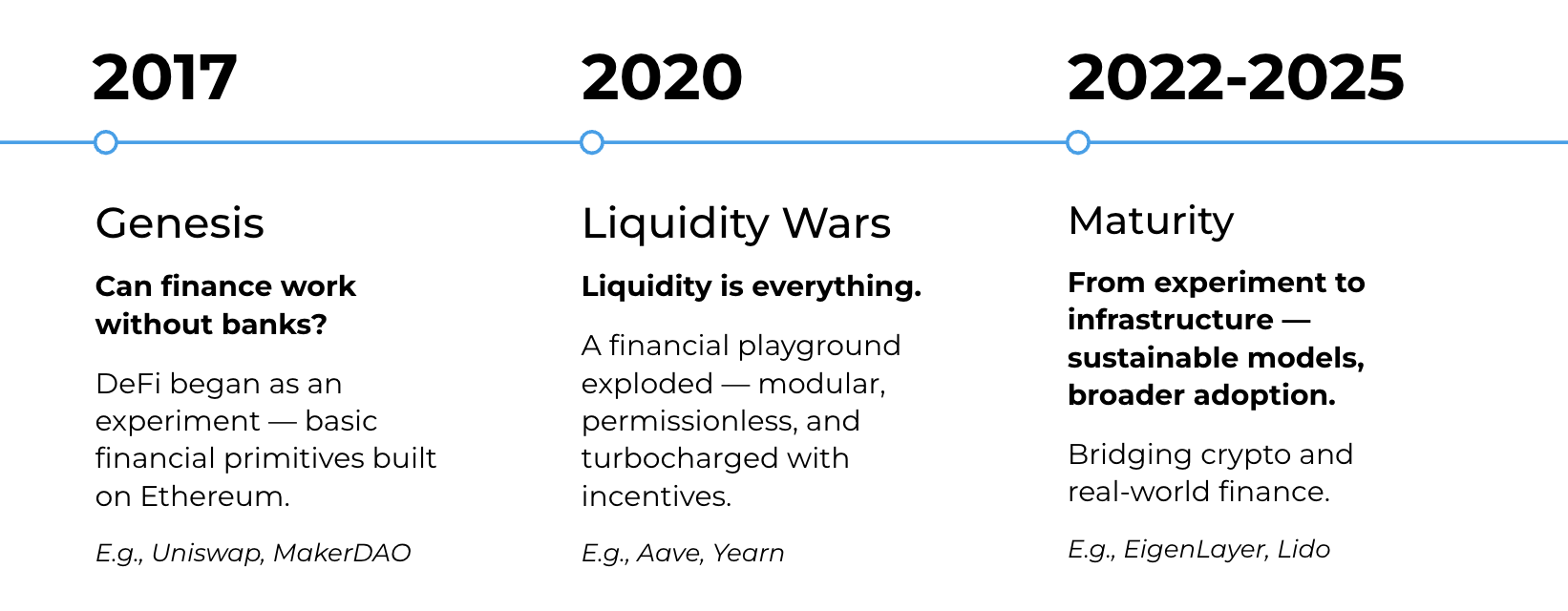

When it first appeared in 2017, DeFi felt like a thought experiment: Can finance work without banks? Projects like Uniswap and MakerDAO laid the groundwork. By 2020, we hit the “Liquidity Wars” — modular protocols like Aave and Yearn competing for deposits with high yields and token rewards. Fast forward to 2025, and DeFi has matured into actual infrastructure: sustainable business models, deeper integrations with real-world assets (RWA), and steady user growth.

The numbers speak for themselves:

- $140B locked in DeFi protocols (TVL) as of July 29, 2025.

- $21B in daily DEX volume.

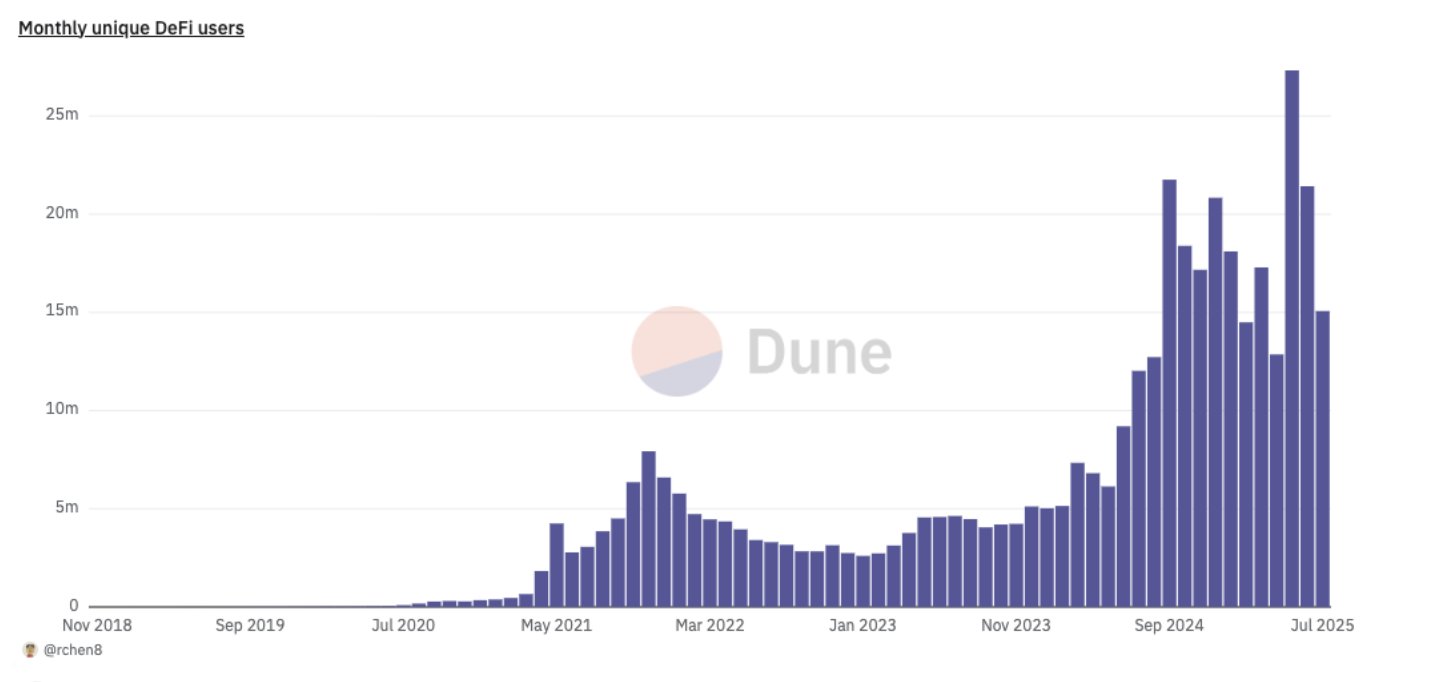

- Monthly active wallets up from 5M in Jan 2024 to 27M in May 2025

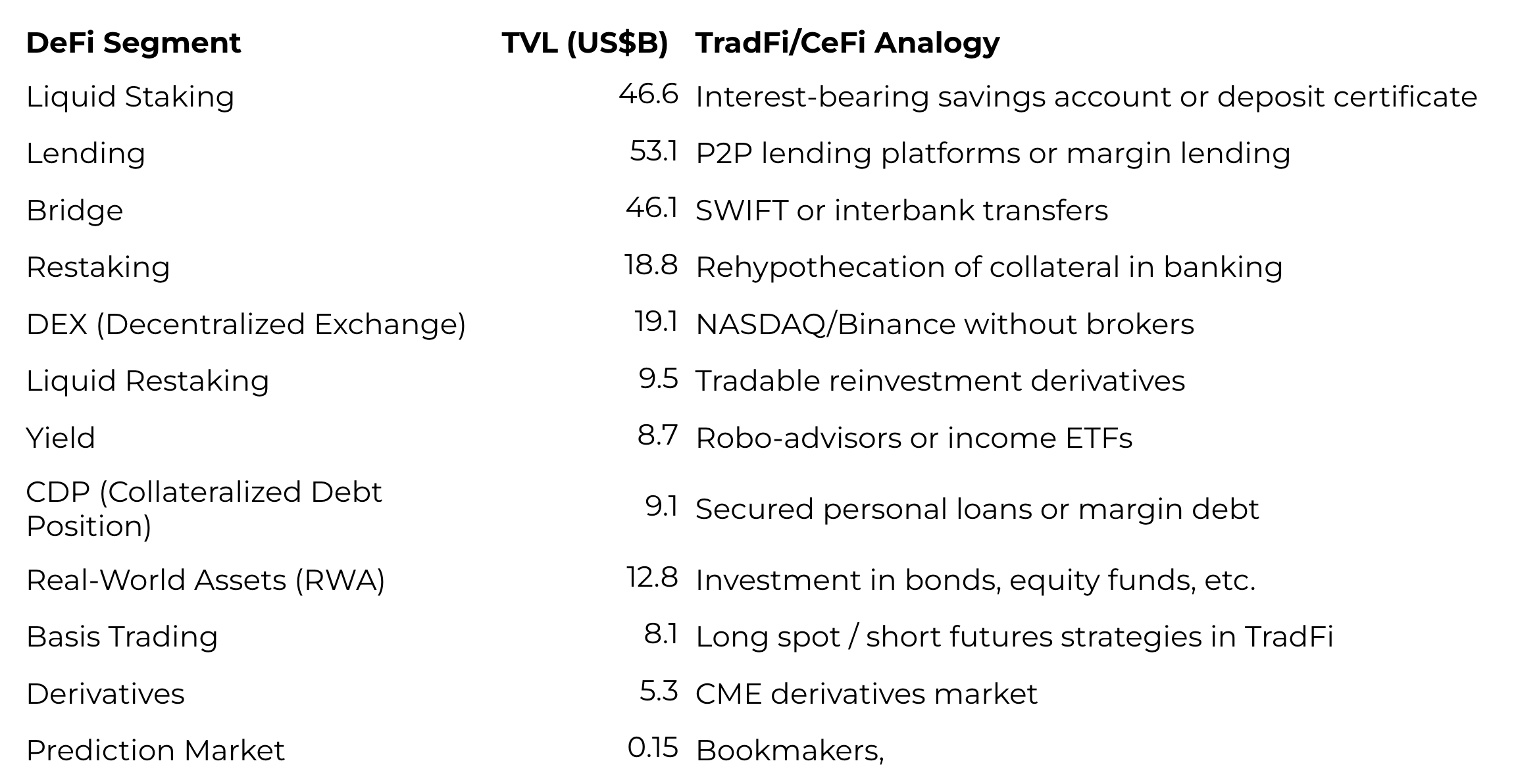

DeFi is no longer just about speculative yield. Segments like liquid staking, lending, bridges, and real-world assets are becoming the backbone of on-chain finance. Each has a TradFi parallel — from savings accounts and interbank transfers to margin lending and bond markets.

Capital flows tell you where conviction is building:

- Lending (53.1B TVL) — +13% YTD

- Bridging (46.1B TVL) — +20% YTD

- RWA (12.8B TVL) — +200% YTD

This shift toward RWA is especially important. Tokenized U.S. Treasuries, credit products, and even equities are finding their way into DeFi, creating new yield sources and making protocols more relevant to mainstream finance.

DeFi is evolving from high-risk playground to a parallel financial system with its own rails, rules, and revenue streams. It’s still not immune to hacks, regulation, or market cycles — but the user growth and capital allocation trends suggest it’s becoming harder to dismiss as a niche experiment.

Part 4. Stablecoins.

If Bitcoin is the store of value and DeFi is the lab, stablecoins are the rails. They’re the dollar’s API — programmable money that moves at internet speed, 24/7, without touching the traditional banking system.

At a glance, stablecoins are simple: a digital token pegged to the value of a fiat currency (most often the US dollar). But behind that simplicity is a market that now settles trillions of dollars a month in on-chain transactions — quietly rivaling, and in some niches surpassing, traditional payment networks.

Why stablecoins matter in 2025

- Ubiquity: They work on almost every major blockchain — from Ethereum and TON to Solana and Tron — making them the most widely supported asset type in crypto.

- Low friction: No bank holidays, no SWIFT delays, no wire cut-off times. Transfers clear in minutes, often low cost.

- Global reach: A small business in Nigeria, a freelancer in the Philippines, or a trading desk in New York can use the same stablecoin, without touching each other’s banking rails.

- Bridge asset: They’ve become the default settlement layer between exchanges, DeFi protocols, and OTC desks.

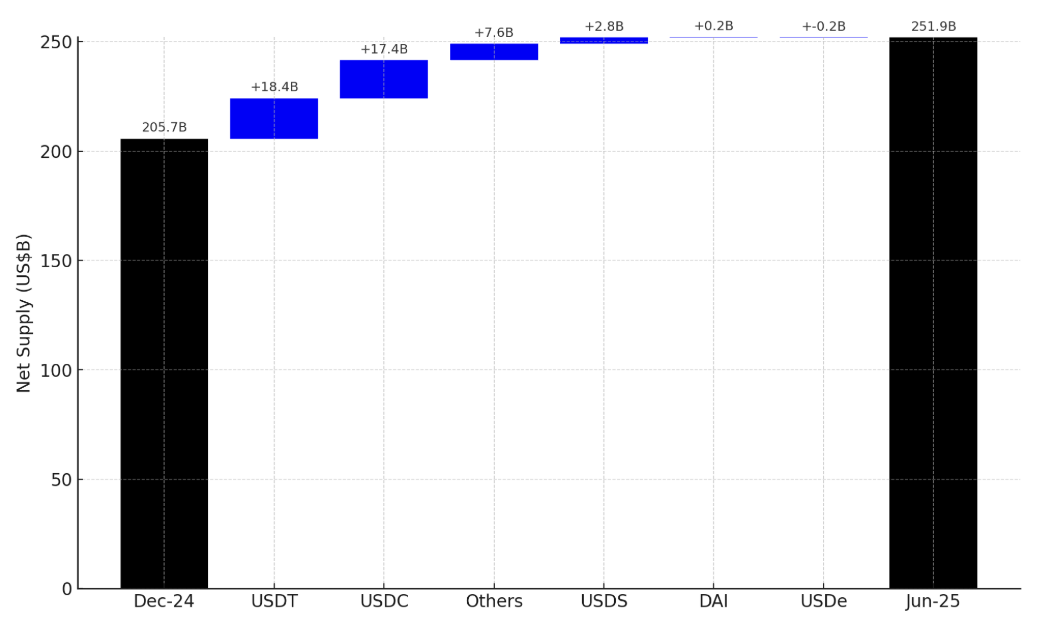

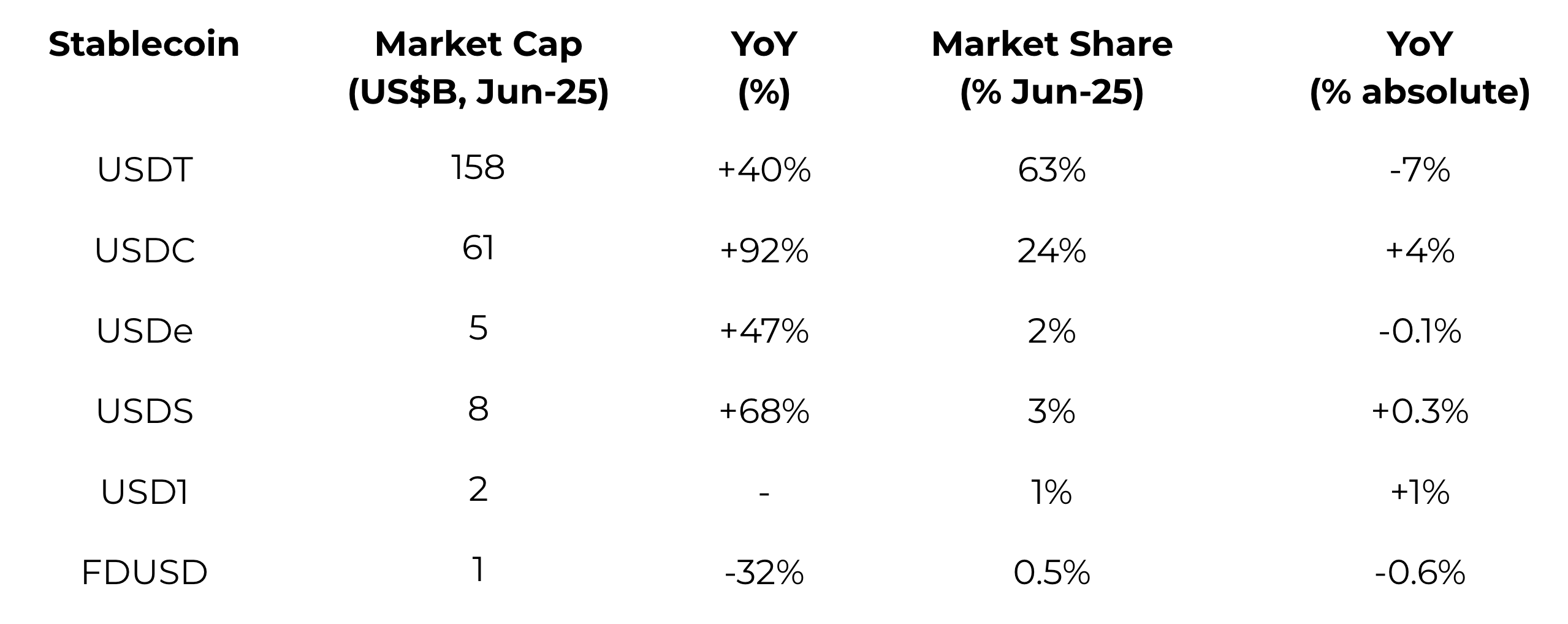

As of mid-2025, $250B+ in circulating supply, close to all-time highs and USDT remains the leader, with USDC, DAI, and newer entrants competing for share.

Looking at the leaderboard, USDT still dominates with a 63% market share and $158B in circulation — but it’s slowly losing ground (-7% absolute share YoY) as rivals catch up. USDC is the clear gainer, up 92% YoY to $61B and now holding nearly a quarter of the market. Smaller players like USDS (+68% YoY) and USD1 (+1% share gain) are carving out niches, often by targeting specific ecosystems or compliance-first use cases. On the other side, FDUSD shrank by a third, showing that not every stablecoin can sustain momentum in a crowded market.

The takeaway: while USDT is still the default choice for most of the world, stablecoin competition is heating up — and the winners will likely be those who can balance liquidity, trust, and multi-chain presence.

And these aren’t just big market caps sitting idle. In the past 30 days, stablecoins processed $4 trillion worth of transactions. Strip out the wash trading, bot loops, and weird on-chain noise, and you still get $903 billion in actual economic activity. That’s almost a trillion dollars moving without banks, SWIFT codes, or Monday-to-Friday business hours.

From my side, these are numbers I keep coming back to. Because it’s not about whether you’re bullish or bearish on crypto — it’s about acknowledging that stablecoins have quietly become infrastructure. They’re the pipes money now flows through, whether for trading on-chain, settling DeFi loans, or wiring funds across continents at 2 AM. And once you have pipes this big, you can’t just turn them off. From my own professional experience at Wallet in Telegram, USDT on TON became the default for P2P payments among many people, the pattern is simple: if a transfer clears in seconds and costs almost 0, people repeat it.

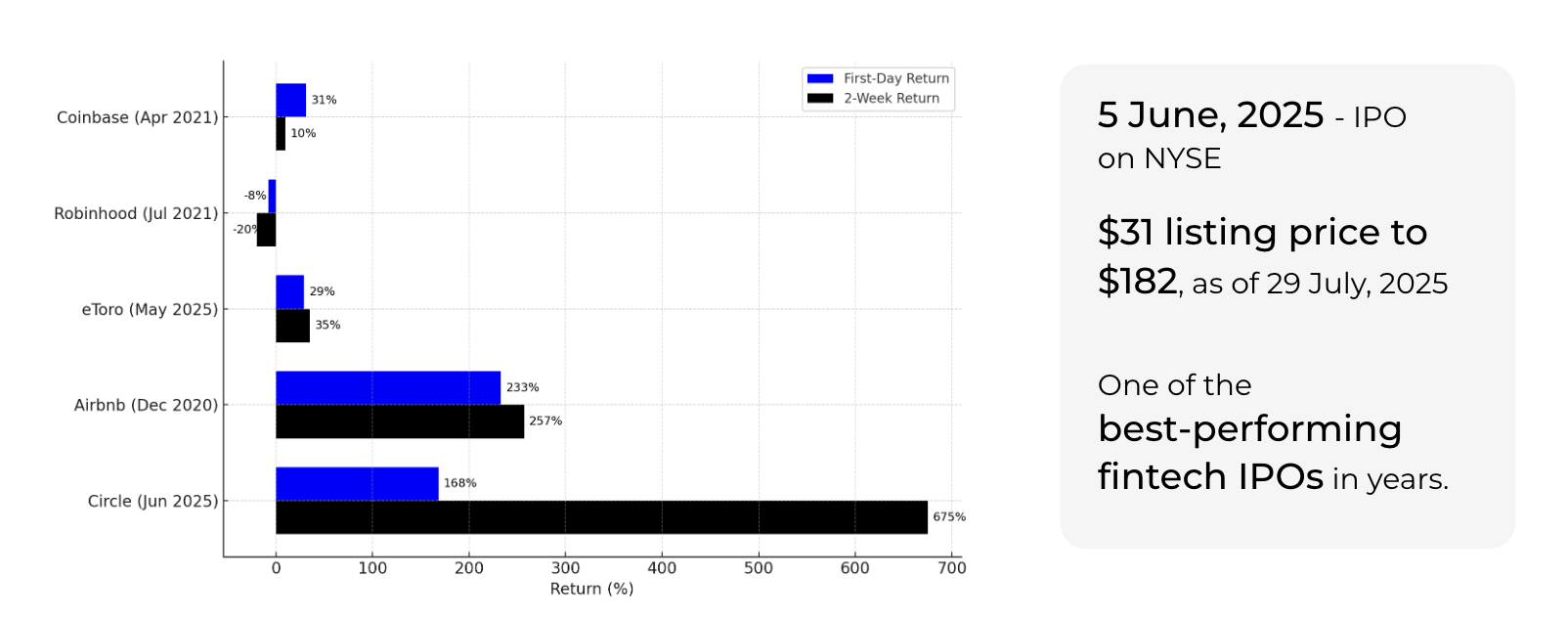

Part 5. Optional one. Circle’s IPO. Stablecoins Go Public

Circle, the issuer behind USDC, staged one of the most explosive fintech debuts in years. Priced at $31 a share on June 5, 2025, the IPO raised over $1.05 billion, valuing the company at around $8 billion. The stock didn’t just open — it blasted off. It began trading at $69, surged as high as $103.75 by the end of the day, and closed around $83 — a jaw-dropping 168% first-day gain. Three weeks later, it peaked near $299, translating to a ~700% total return from the IPO price.

This ride wasn’t driven only by crypto hype. Circle showed real financials: in Q1 before the IPO, it posted net income of $65 million on revenue of $579 million. That, combined with growing regulatory clarity — including the GENIUS Act and bank charter discussions — fueled investor confidence.

But not everyone was entirely cheerful. Some analysts sounded alarms on valuation: warnings of “overvaluation” and set a downbeat targets way lower. e.g., $85, flagging competition and margin risk. As of today, sentiment remains mixed — with some “Buy” ratings in place, but caution from others ahead of its first earnings post-IPO.

Instead of a Postscript: what’s next?

When you zoom out, crypto in mid-2025 feels less like a niche bet and more like a maturing financial layer that’s starting to plug directly into the global economy. If the last few years were about survival and experimentation, the next few might be about integration and scale. Here’s what I think is next — and why it matters.

-

Fed Pivot + Fiscal Tailwinds = Risk-On Setup

If interest rates ease and governments add a bit of fiscal stimulus, risk assets — stocks, crypto, even some commodities — tend to rally. We saw this in previous BTC cycles, where macro liquidity was as much a driver as any blockchain upgrade. In that sense, Bitcoin’s “macro signal” role (remember the PMI lag story from earlier) could line up perfectly with a friendlier policy environment.

-

US Shifts from Enforcement to Legislation

For years, crypto in the US has been about fighting court cases and reading between the lines of enforcement actions. Now, lawmakers are actually passing bills — on stablecoins, tokenized assets, and even tax clarity. If this continues, the next Circle-style IPO won’t need to tiptoe around regulatory risk in its S-1 filing.

-

TradFi-Crypto Convergence

When I covered Circle’s IPO earlier, I called it a turning point for stablecoin legitimacy. That’s part of a bigger story: traditional finance isn’t just “dabbling” anymore. It’s buying in — acquiring crypto companies, launching tokenized treasuries, and putting blockchain rails under real-world payments. Each deal pulls the two worlds closer until “crypto” is just “finance.”

-

Stablecoins as Real Payment Infrastructure

Looking back at the $900B+ in adjusted monthly stablecoin volumes we discussed, it’s clear this isn’t just traders swapping on DEXes. Stablecoins are paying suppliers in Asia, settling DeFi loans, and moving salaries across borders. The more real-world use cases we see, the harder it becomes to dismiss them as “just a trading chip.”

-

Tokenized RWAs

Real-world assets on-chain used to mean the occasional gold token or exotic bond. Now we’re seeing serious scale: treasuries, private credit, real estate shares — all tokenized and tradable. If secondary liquidity deepens, it could change how institutions think about asset allocation entirely. Imagine swapping a bond for a stablecoin in seconds, without going through five intermediaries.

-

AI-Native Crypto UX Emerges

We’ve talked a lot about infrastructure and regulation, but the user experience is quietly going through its own revolution. AI agents that can trade, rebalance, and even negotiate terms in DeFi are becoming real products. This isn’t just about making crypto “easier” — it’s about making it invisible, baked into the apps people already use. And yes, I’m watching this space very closely for my own work, because it’s where mass adoption will either click… or stall.

If I had to sum it up, I’d say: the market feels like it’s moving from why to how. The narrative is no longer “should we use crypto?” but “how do we plug it in without breaking what we have?” And that’s when things tend to accelerate.

Please feel free to reach out, I’m happy to discuss it in more detail. Stay tuned for the next review.

[story continues]

tags