In 2017, Equifax, the credit industry’s nerve center was breached and 150 million Americans’ personal data was exposed. The aftermath was catastrophic: huge financial losses and complete collapse of trust in how credit data is stored and protected. Today, that epic fail is a warning: any central repository of sensitive credit data is a single point of failure. Traditional credit bureaus like Experian and Equifax suffer from inadequate assessments due to the hiding of material information, static models, misrepresentation and human bias, often with opaque algorithms.

Consumers frustrated by unexplained score changes and disputes know the feeling all too well: a recent study found the FTC reports one in five credit reports have errors that can harm people’s scores. And worse 1.7 billion adults worldwide have no formal credit history at all, invisible to lenders. The combination of data breaches, system errors and exclusion has created a credit crisis.

The Fragile Credit Score Machine

Traditional credit scores are like black magic. The formulas are secret, so why a score changed is often a mystery. Even regulators admit the system is broken: an EU court recently ruled that fully automated credit scoring must allow human review since “automated decision-making” is normally prohibited under GDPR. In practice, that means if a bank denies you credit based solely on an algorithm, you have the right to challenge it. Put simply, Europe is now demanding consent and transparency for any computer-calculated credit decision, a slap in the face of treating credit scores like an infallible oracle.

Meanwhile, in the US the Fair Credit Reporting Act (FCRA) enshrines consumers’ right to correct errors but on-chain credit data would need new ways to “undo” mistakes. The reality is that credit bureaus were never designed to be user-friendly or inclusive. Errors are common; surveys find 20% of consumers have at least one mistake on their report and millions more fall through the cracks. According to the World Bank and industry reports, about a billion or more people worldwide have little or no formal credit history. In Africa, for example only 20-30% of adults have a credit score. That means the vast majority of borrowers are literally “invisible” to lenders and can’t tap savings or loans. A critic wryly observes that relying on these bureaus is like keeping your valuables under a rock and then being surprised when someone flips the rock open.

Blockchain to the Rescue

Blockchains offer a radical solution; move credit history out of a silo and onto a shared, public ledger. Since blockchain data is immutable, once a transaction or loan repayment is recorded, it can’t be altered or deleted. That means no single hacker can quietly erase or fabricate decades of loan history; every entry is out in the open. In theory, a blockchain-based credit system would let each borrower see exactly how their score is built. In other words, you’d know exactly why timely rent payments or utility bills helped raise your score, rather than being mystified by a “secret sauce” algorithm.

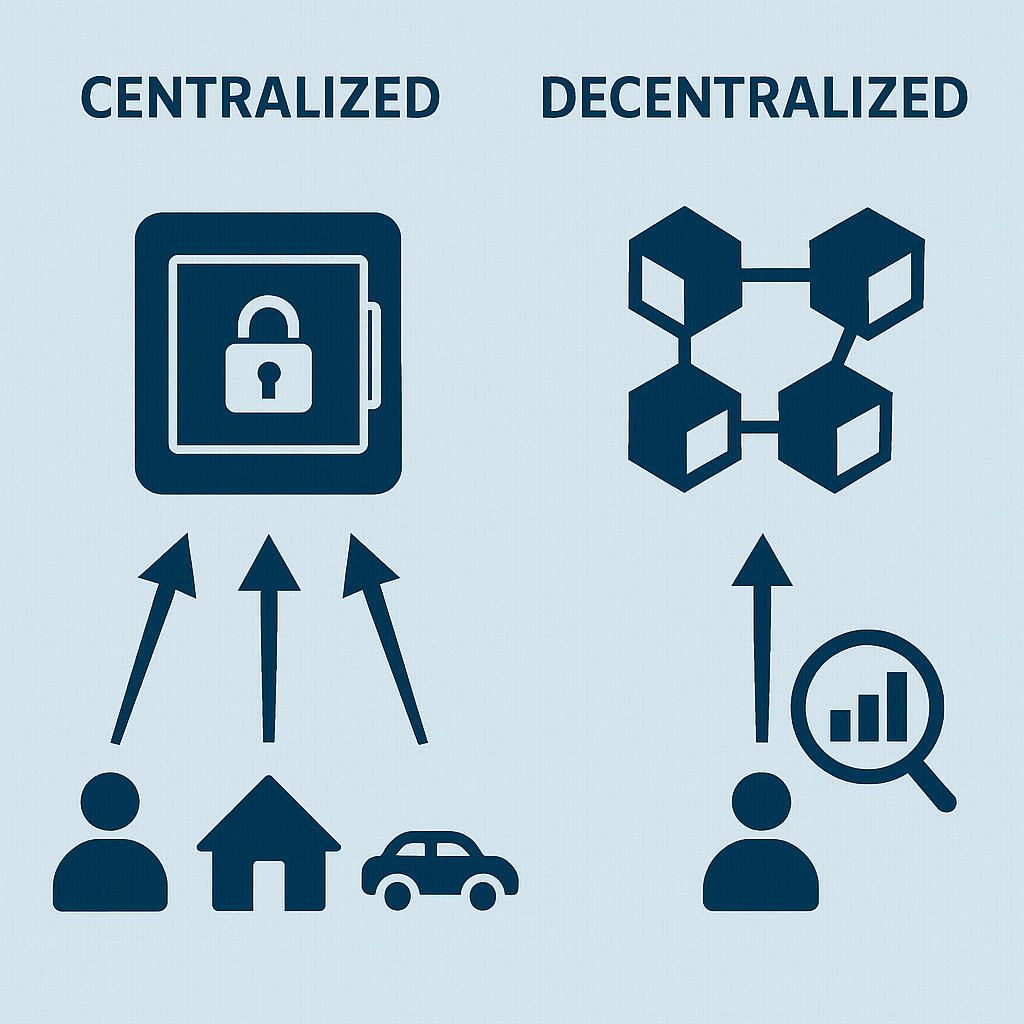

This infographic shows a centralized credit bureau as a vault icon with a single lock and a decentralized blockchain ledger as a network of connected blocks. Arrows illustrate how data from multiple sources flows into each system, highlighting that while centralized bureaus store data in one closed repository, decentralized ledgers distribute and record it transparently on a public, permission-based network.

Most importantly, a smart credit ledger could include alternative data sources. Utility bills, phone bills and even peer-to-peer lending payments can be logged on-chain. This lets us “build credit” from everyday financial behaviour, a boon for those without bank accounts. Imagine a young migrant worker who pays rent and wraps up microloans on a phone app; on a blockchain, each payment becomes part of a public credit file. The result is a more inclusive scoring model that “opens up credit” to those the old system ignored. And because the scoring logic can be open or auditable, it alleviates regulatory concerns about hidden biases.

Building a Decentralized Credit Identity

Of course, immutable records aren’t enough; you also need to know who those records belong to, without sacrificing privacy. That’s where decentralized identity comes in. In a blockchain credit system, users can have a digital identity wallet that verifies their real-world credentials without revealing everything. For example, Gluwa’s platform uses services like 1Kosmos BlockID to link on-chain profiles to verified identities under KYC rules. Consent is key: each person decides what personal info (e.g. name, income) to share before their loans or repayments are recorded on the ledger. Some innovators even propose using “soulbound” NFTs or cryptographic credentials to anchor identity to credit profiles. In effect, you’d carry a digital passport that references your blockchain credit history. This would satisfy regulators: you get the transparency, but still control over personal data.

The flipside is that regulators are watching closely. As I mentioned, the EU already considers credit scoring as automated decision-making, so any blockchain scoring must allow human oversight or opt-in consent. And privacy laws (like the GDPR “right to be forgotten”) are fundamentally at odds with an unchangeable ledger. In practice, a compliant system would keep sensitive data off-chain (or encrypt it) and only record proofs or hashes on-chain, and let borrowers request corrections off-chain. These are all open technical challenges. But with smart design, blockchain credit systems could actually give users more legal protections: after all, every decision is documented and auditable.

Spotlight on Gluwa and Creditcoin

Gluwa is one of the teams building this future. Founded in 2016 by Tae Oh, Gluwa’s mission was to give emerging-market users access to reliable finance. The company says about 1.4 billion people globally were “financially excluded” by old systems. In response, Gluwa launched Creditcoin in 2019, a layer-1 blockchain specifically for lending. As the Creditcoin blog explains, it’s “a public ledger for recording loan performance, thus a shared record of publicly verifiable credit histories”. By partnering with local fintech lenders (e.g. Nigeria’s Aella Finance), Gluwa records each loan and repayment on the Creditcoin chain.

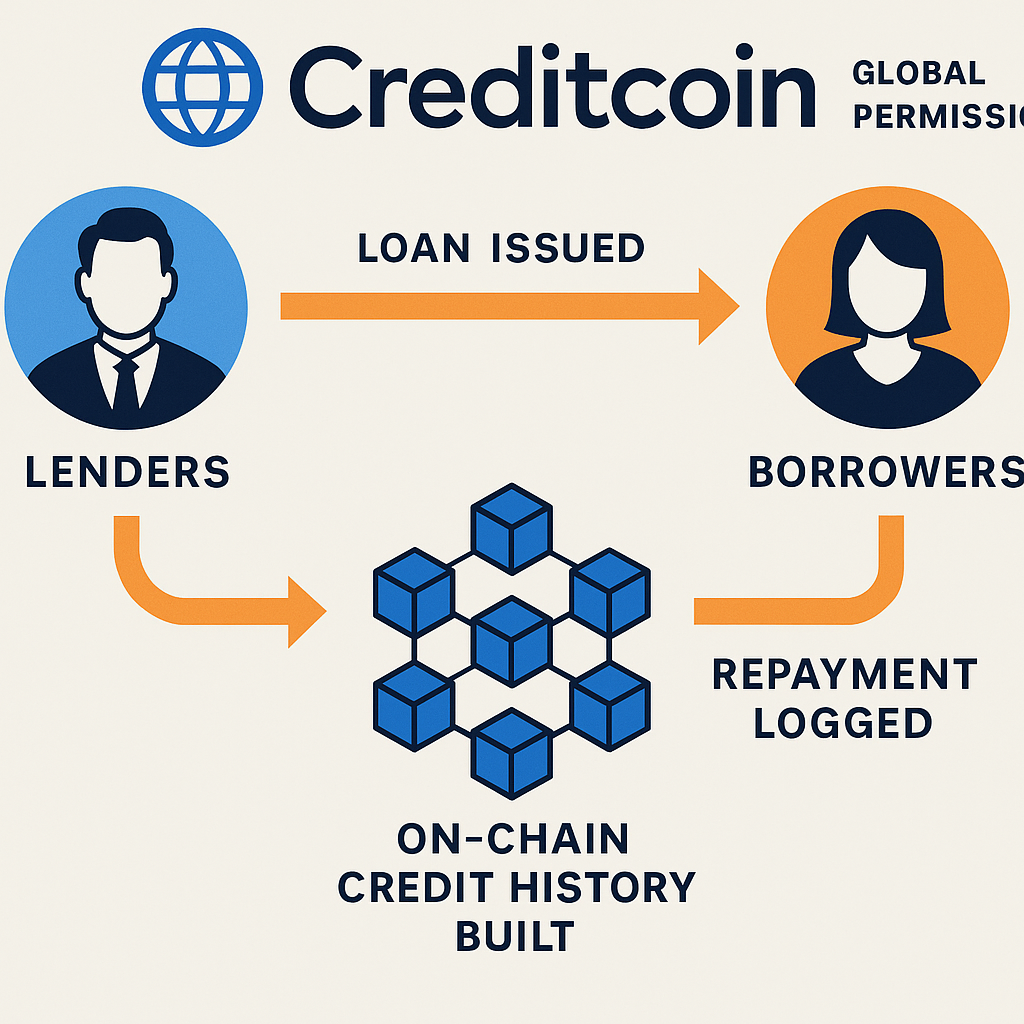

This infographic shows Gluwa’s Creditcoin network flow: lenders issue loans to borrowers, repayments are logged, and each transaction is recorded on the blockchain to build an on-chain credit history. It highlights Creditcoin’s global and permissioned design, showing how decentralized finance connects lenders and borrowers securely and transparently.

This has real-world impact. To date, Gluwa’s Creditcoin network has already logged millions of loan transactions. In fact, a recent report says over 4.27 million loans (about $80 million total) have been processed on Gluwa’s system, creating credit histories for over 337,000 users. Each entry on the ledger is a credit reference: if a borrower repays on time, that performance permanently boosts their trustworthiness, accessible (with permission) by any global investor.

Loan repayments are processed via Creditcoin, generating a transparent, publicly accessible record of each borrower’s transaction history. In plain terms, this means that everyday people, shop owners, farmers, and gig workers can build a financial reputation on blockchain where none existed. A lot of underserved, underbanked or completely unbanked users have difficulty getting credit because they live in an emerging country that lacks the required infrastructure.

The tech is worth a look. Gluwa uses stablecoins pegged 1:1 to local currencies for lending. So receiving $DGT tokens in Nigeria is essentially getting Naira, but with the repayment safely tracked on-chain. Lenders anywhere, even thousands of miles away, can fund those loans, knowing all repayment data will be recorded on-chain. This bridges the gap between global investors and local borrowers. And behind it all is Creditcoin’s public ledger. In short, Gluwa isn’t another bank; it’s building the plumbing that connects borrowers and lenders with code.

Africa’s Test Case: eNaira and Nigeria’s Push

Gluwa’s biggest pilot so far is with Nigeria, the biggest economy in the continent. In 2021, Nigeria launched its eNaira CBDC, but by early 2023, adoption was minimal. To boost usage, the Central Bank of Nigeria (CBN) signed an MOU with Gluwa. Now, Gluwa will plug its Credal credit platform into the eNaira system. The plan is big: every eNaira user, even someone with no bank account, can start building a “credit reputation” as they transact. Under this deal, Gluwa will integrate its Credal technology into the eNaira platform… to create ‘credit reputations’ for unbanked users, thus increasing financial inclusion.

In concrete terms, the integration will do everything from opening millions of eNaira wallets to embedding credit-scoring into loans and payments. Credal will streamline loan origination, management, settlement and credit assessment for local fintech lenders. It will solve the biggest problems: traditional banks exclude the unbanked and credit histories don’t travel beyond a country’s borders. Gluwa’s Credal addresses both by recording an individual’s entire eNaira transaction history, whether they live in Lagos or send money to Accra, on the blockchain.

In practical terms, this means a Nigerian farmer who gets a ₦10,000 loan via an app can have that repayment count on his record, even if he later moves or works in another country. Gluwa’s Credal technology … allows fintech clients to participate in global investment opportunities through pseudo-anonymous credit profiles, thus increasing financial inclusion and empowerment.

And Nigeria may not be the only one. Gluwa says it’s already in talks with other African governments (Liberia, Ghana, Sierra Leone) to roll out similar schemes. If those talks yield fruit, future credit histories could follow the African diaspora.

Regulation and the Road Ahead

For all the potential, blockchain credit also runs into on-the-ground challenges. EU and US regulators are still working out where immutable ledgers fit within privacy and fairness legislation. To take just one example, the CJEU's recent decision interprets a fully automated credit score as an "automated decision" under GDPR. That makes human review or positive consent necessary for any borrower. For what it's worth, blockchain transparency assists: all credit decisions can be encoded. Conversely, actual "erasure" is impossible on a public chain, so GDPR "right to be forgotten" is tricky. Sophisticated designers will keep personal data off-chain and utilize the blockchain to store proofs or hashes alone so that one can delete a user's on-chain pointer if necessary.

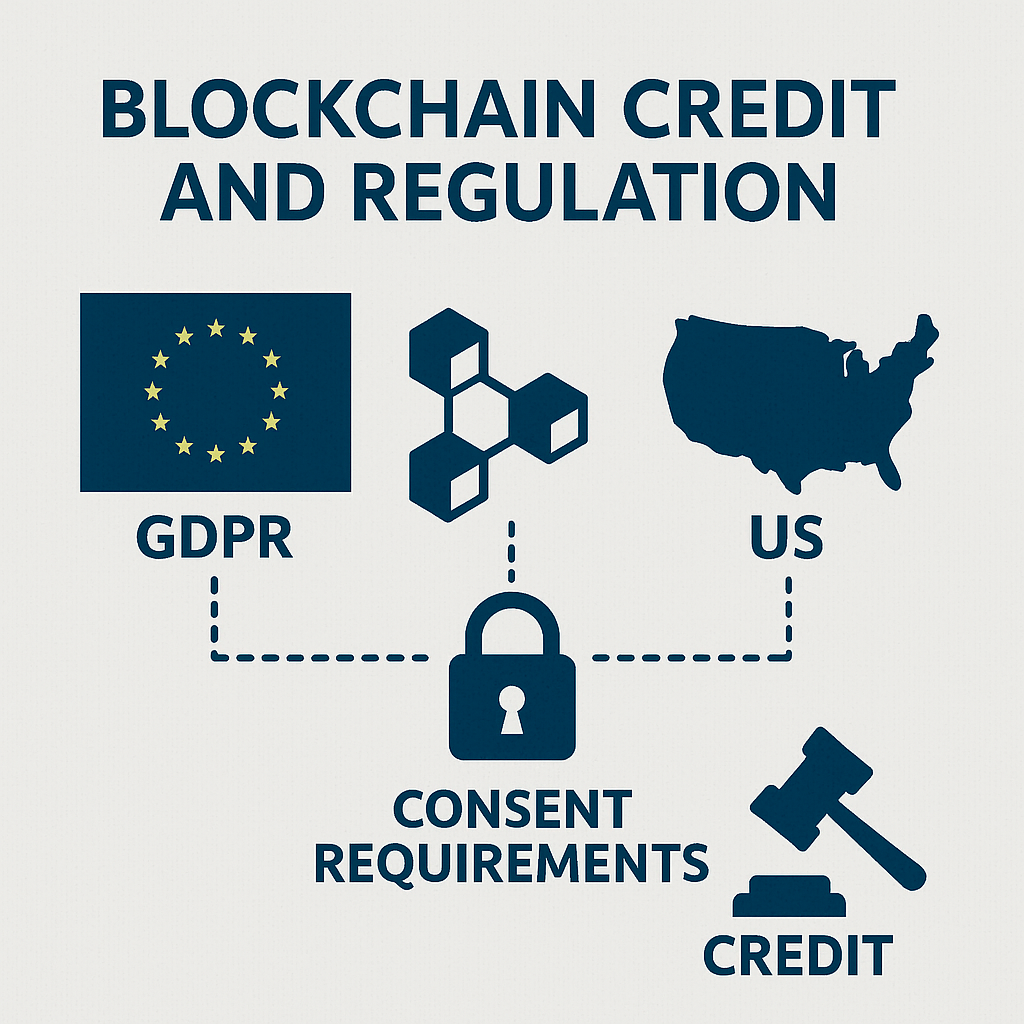

This infographic describes how decentralized credit systems meet global regulations. It illustrates the EU GDPR and US FCRA, mapped to blockchain technology with network, padlock and gavel symbols denoting consent requirements and legal governance in blockchain-based credit reporting.

In the US, the Fair Credit Reporting Act (FCRA) mandates accuracy and provides dispute rights to consumers. Any blockchain alternative would also need to provide borrowers the right to rectify inaccuracies. That implies on-chain dispute records or native arbitration. Curiously, blockchain credit can be built regulation-aware. For instance, Gluwa's platform demands permission from borrowers for anyone to access their record, handing back control to the consumer that is absent in today's bureaus.

Note that big central banks and regulators are indeed interested in these concepts. The existence of the eNaira contract itself is a fact of official endorsement. And partnerships with industry players (such as Microsoft's with Gluwa) indicate that even Big Tech is positioning its cloud and blockchain offerings to ensure these solutions are compliant and scalable. In a way, the early movers are demonstrating to regulators that decentralized credit can be as or even more secure than current systems.

It will not be overnight. Equifax will not be replaced by a single blockchain but its obsolescence is assured. Think of a world where credit histories are global public records (encrypted, of course), where a prudent small business owner in Nigeria or Bangladesh can receive a home loan in New York or Lagos on blockchain reputation alone. The likes of Gluwa are constructing the rails today. Their ledger isn't only going to bring down Equifax; it will bring the underbanked into the light. If so, someday the headlines will blare "Equifax Finally Blindsided by World's First Decentralized Credit Ledger, Unreplacement Confirmed.".

[story continues]

tags