Table of Links

Abstract, Acknowledgements, and Statements and Declarations

-

Background and Related Work

-

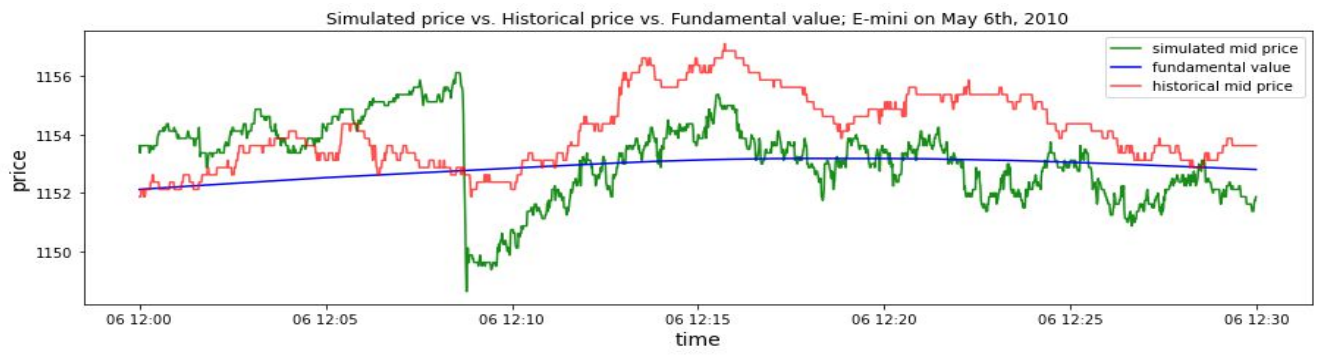

2010 Flash Crash Scenarios and 5.1 Simulating Historical Flash Crash

-

Mini Flash Crash Scenarios and 6.1 Introduction of Spiking Trader (ST)

-

Conclusion and Future Work

6 Mini Flash Crash Scenarios

The above section provides an analysis of the occurrence of flash crash events. The 2010 Flash Crash is so large that no following events have rivalled its depth, breadth, and speed of price movement (Paddrik et al. 2017). However, flash crashes on a smaller scale do occur more frequently. Johnson et al. (2012) identify more than 18,000 mini flash crash incidents between 2006 and 2011 in US equity markets. Those mini flash crashes are characterised to be abrupt and severe price changes over a short period of time. One natural question is how those mini flash crashes happened. As a second application for the proposed agent-based model, we investigate and analyse the causes of mini flash crashes in the framework of our agent-based financial market simulation. An innovative "Spiking Trader" is introduced to the market to mimic the trigger of mini flash crash events. A typical mini flash crash event in our simulation is analysed in detail, followed by experiments for exploring the conditions for mini flash crash events.

6.1 Introduction of Spiking Trader (ST)

In the current literature, there is a growing consensus that the mini flash crashes result from interactions between various trading algorithms that operate at or beyond the limits of human response times, such as the procyclical behaviours of high-frequency market participants. However, there are various triggers for mini flash crash events. According to Karvik et al. (2018), one specific trigger could be orders that are large relative to the supply of available limit orders, which bring price shocks to the market. To mimic the occasional price shock in the market, a type of trader agent called "Spiking Trader" is introduced to our agent-based artificial financial market.

6.2 Mini Flash Crash Analysis

To investigate mini flash crash events, there are some modifications to the simulation configuration. The number of market makers in the simulation is reduced. Our experiments show that this increases the probability of the occurrence of mini flash crash events. The reason is that less market makers will lead to thinner market depth, generating more mini flash crash events for scrutiny. The institutional trader is removed from the market; while two spiking traders are introduced to the market simulation. Other model parameters are the same as the simulation for the 2010 Flash Crash. Detailed model parameters for mini flash crash simulation are shown in Appendix D.

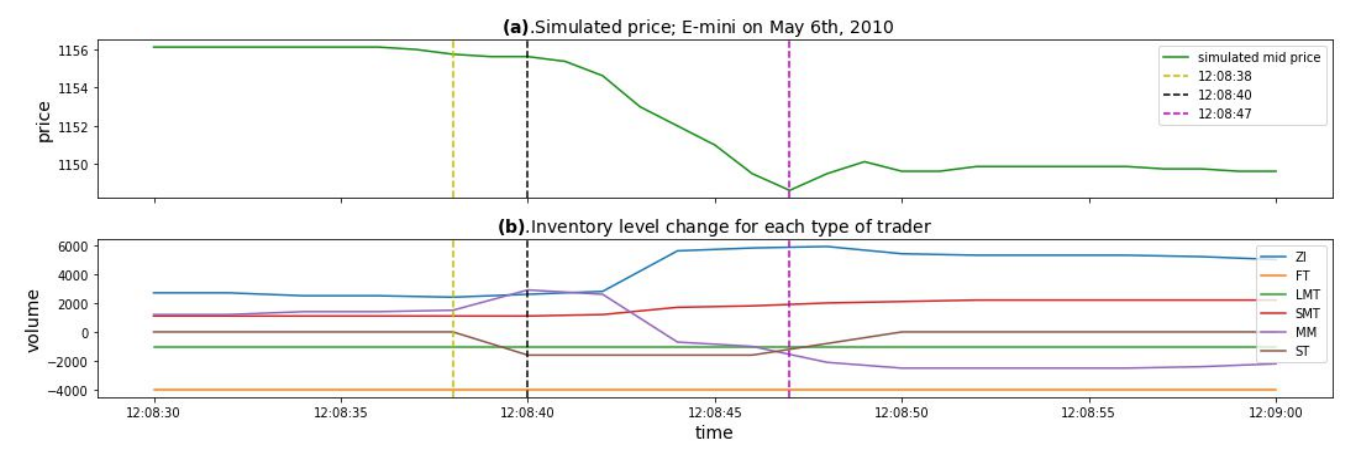

Figure 10 presents a typical mini flash crash scenario in our simulation. The price drops nearly 80 basis points in just several seconds, and then bounces back towards the fundamental value. Figure 11 shows the inventory level for each type of trader against simulated price during the mini flash crash scenario. According to Figure 11, the trigger and dynamics for that specific simulated mini flash crash are very straightforward:

• At 12:08:38, a spiking trader is activated to bring downward shocks to the market. The spiking trader submits sell orders to the market in the next 2 seconds. Those sell pressure in the 2-second interval is mainly absorbed by market makers.

• Having absorbed the sell orders from spiking trader, one market maker accumulates a relatively large inventory at 12:08:40 and the inventory limit is reached. For risk management purposes, the market maker decides to reduce the position and then temporarily withdraw from the market. The sell orders from this market maker are digested by other market makers.

• The same high-frequency dynamic happens between 12:08:40 and 12:08:42. During this small time period, the same positions transfer between different market makers, creating the "hot-potato" effect on a smaller scale. Several market makers withdraw from the market temporarily after emptying their inventory.

• At 12:08:42, only 4 seconds after the spiking trader is activated, the market suffers from the liquidity loss because of the withdrawal of some market makers. The sell orders from the remaining market makers create dramatic market impacts due to thin liquidity, dragging the price down for more than 60 basis points in 5 seconds.

• At 12:08:47, the price has dropped 80 basis points compared to the price level at 12:08:38. The price then stops dropping and then gradually bounces back to the original level.

Note that in the above simulation, the fundamental traders are configured to have a trading interval of 100 steps, which is the calibrated value from Section 4. The specific simulated mini flash crash event happens in a time horizon that is shorter than the horizon over which lower frequency fundamental traders observe the market. This is shown in Figure 11, where the inventory for fundamental traders hardly changed during the mini flash crash event. The analysis shows that the mini flash crash events result from the procyclical behaviours among high-frequency market makers, precipitated by price shocks that are created by spiking traders or other market participants.

Authors:

(1) Kang Gao, Department of Computing, Imperial College London, London SW7 2AZ, UK and Simudyne Limited, London EC3V 9DS, UK (kang.gao18@imperial.ac.uk);

(2) Perukrishnen Vytelingum, Simudyne Limited, London EC3V 9DS, UK;

(3) Stephen Weston, Department of Computing, Imperial College London, London SW7 2AZ, UK;

(4) Wayne Luk, Department of Computing, Imperial College London, London SW7 2AZ, UK;

(5) Ce Guo, Department of Computing, Imperial College London, London SW7 2AZ, UK.

This paper is available on arxiv under CC BY-NC-ND 4.0 DEED license.

[story continues]

tags