On paper, 2025 was supposed to be the year when euro payments finally became instant by default. In practice, the picture is more nuanced.

As of 9 January 2025, banks in the euro area were required to receive instant euro credit transfers. By 9 October, they were expected to send them as well – 24/7, within seconds and without charging extra fees compared to standard SEPA transfers.

These milestones were set by the EU’s Instant Payments Regulation (IPR) and framed as a turning point for European payments. Now that the deadlines have passed, the questions are: did everyone actually make it on time and did euro payments really become increasingly instant? What does “SEPA Instant adoption” mean in practice, especially for third-party services that embed bank payments into their products?

We decided to dig into this and examine what has really changed – and where important gaps still remain.

Did all banks make the deadline?

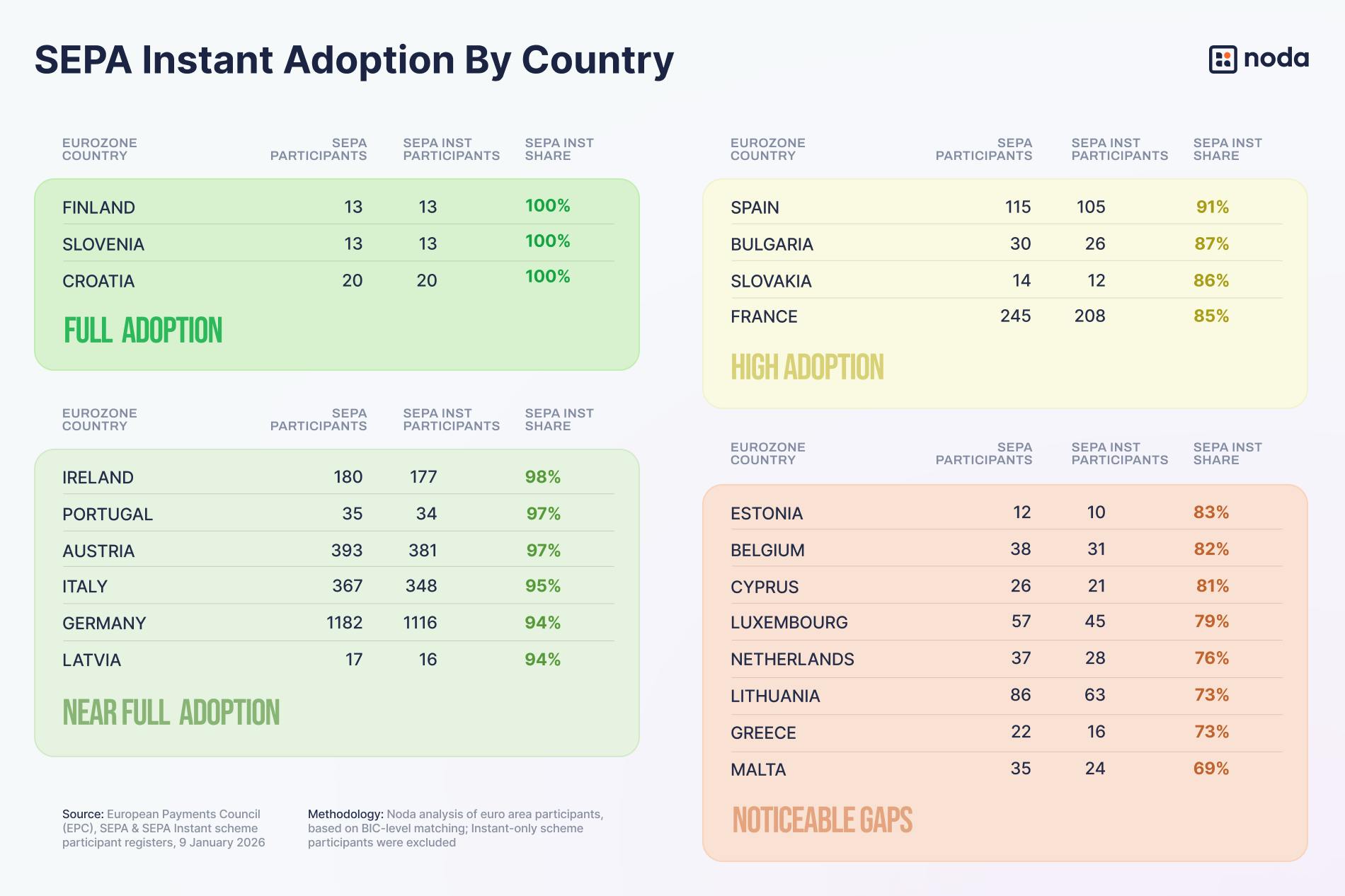

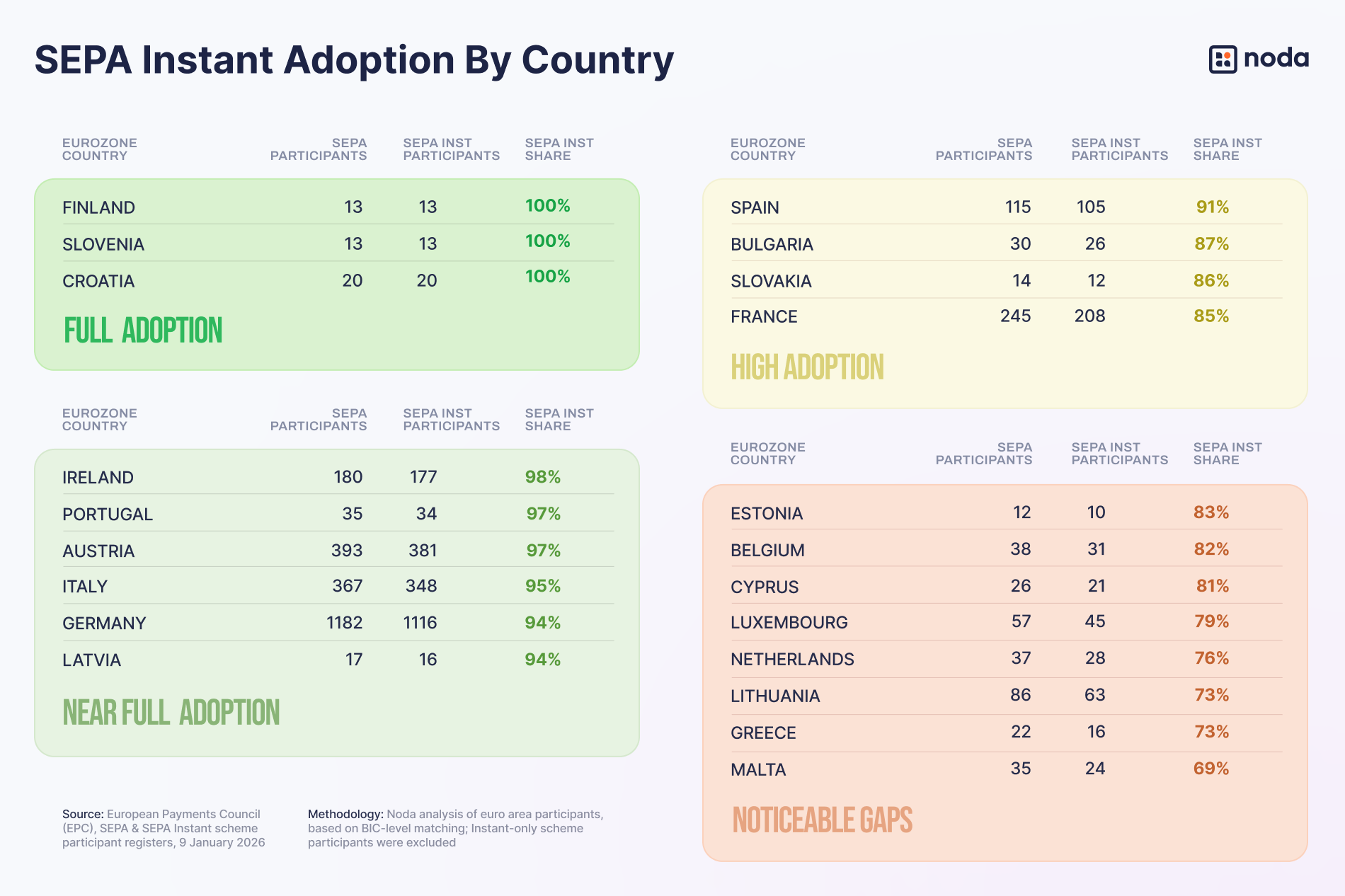

The short answer is mostly – but not uniformly. As of 9 January 2026, 88% of SEPA participants in the euro area were registered for SEPA Instant Credit Transfer, based on Noda’s analysis of EPC participant registers. Across countries where the euro is the national currency, around 9 out of 10 SEPA participants are already live on Instant Payments.

Several countries have already reached complete coverage, while the majority lag slightly but still show high adoption. Finland, Slovenia and Croatia have reached 100% SEPA Instant participation, while Ireland (98%), Austria (97%), Portugal (97%), Italy (95%) and Germany (94%) are now close to full coverage. These outcomes are not accidental. Countries with simpler banking ecosystems and strong national coordination tended to reach high coverage faster, even in markets with large numbers of PSPs.

Countries lagging behind typically have cooperative banking structures, more legacy core systems and a large number of non-retail or cross-border participants. These are often financial hubs or jurisdictions with many passporting institutions. In these markets, a significant share of entities participate in SEPA only in a limited capacity.

Why participation rates don’t tell the full story

On paper, SEPA Instant participation rates of around 80–90% can look lower than expected given the regulatory deadlines. In practice, this does not translate into a similar gap in consumer coverage.

The largest consumer banks are already connected, so if you pick a random consumer in a eurozone country, the odds are very high that they can already send and receive instant payments. The remaining gaps mainly affect smaller or non-consumer institutions.

Is missing a deadline “normal” – and are there consequences?

In theory, failure to comply with the Instant Payments Regulation can result fines of up to 1% of annual turnover for serious violations.

In practice, enforcement tends to be more pragmatic:

- Regulators focus on systemic risk and consumer impact

- Large banks and high-volume PSPs are prioritised

- Institutions with clear remediation plans are often given leeway

Notably, the European Payment Council’s public update of June 2025 reported no national PSP communities in “red” (not ready) status. This suggests that most institutions met minimum regulatory expectations, even if not all capabilities were fully rolled out across every channel yet.

Has Europe really gone instant?

SEPA Instant is now broadly available across euro area banks – but it has not yet become the dominant way payments move in Europe.

By mid-2025, instant payments represented around 25% of SEPA credit transfers.

However, SEPA credit transfers themselves account for only part of Europe’s overall payment activity. Cards, cash, direct debits, local instant schemes, high-value rails such as TARGET and non-euro payments still represent the majority of transactions across the region.

Growth in instant payments is being driven mainly by P2P and consumer use cases, while B2B adoption remains limited due to liquidity, approval and reconciliation constraints.

Looking ahead, instant payments are expected to grow steadily rather than explosively. According to ACI’s 2024 Prime Time for Real-Time report, they are forecasted to account for around 13% of all electronic payments in Europe by 2028, up from 8% in 2023 – still well behind other regions, where instant payments are projected to reach nearly 30% in Asia-Pacific, around 50% in Latin America, and over 55% in Africa.

Europe has made strides to make instant payments a regulatory standard but actual usage is still catching up, especially beyond core banking channels.

Does bank-level instant adoption make third-party payments instant too?

This is where expectations and reality diverge most sharply.

The Instant Payments Regulation ensures that banks can move money instantly between themselves. It does not ensure that:

- Payment initiation via PSD2 APIs is instant

- Third parties receive real-time confirmations

- APIs expose clear “instant vs standard” payment options

- Documentation, testing, and certification are updated on time

For third-party payment providers like open banking companies or embedded finance platforms this means that “SEPA Instant-enabled banks” do not automatically translate into instant user experiences.

In practice, instant payments remain most reliable inside banks’ own channels. Outside of them, payments initiated via open banking APIs may default to standard SEPA rails or provide delayed and incomplete status feedback.

"Whilst SEPA Instant creates the opportunity for instant payments, the end user only sees its benefits once these infrastructure capabilities are surfaced to retail customers by payment providers," says Alex Batlin, Executive Advisor at Noda, an open banking platform.

As a result, delivering truly instant payments beyond bank channels remains a shared challenge between banks and third-party providers.

What “instant” really means going forward

The SEPA Instant deadlines marked an important step forward but they're really just the beginning. Banks across Europe have largely built the infrastructure needed to move money in seconds – and that's no small achievement. But making instant payments work seamlessly in everyday life will require banks, payment providers and platforms to keep working together on the practical details: better APIs, clearer payment options and real-time confirmation systems that actually work. The regulation established the baseline. Whether instant payments become the norm depends on what gets built on top of that foundation in the months and years ahead.

[story continues]

tags