Table of Links

-

Introduction

1.1 Periodic auction and continuous limit order book

1.2 Comparison and main flaws of limit order book

1.3 Optimal policies to cure auction’s inefficiencies and related works

-

Auctions market modeling with transaction fees and randomization

2.1 The market characteristics

2.3 Strategic Trader’s optimization and market quality

2.4 Data and numerical analysis

2.5 Strategic trader with full information: efficient but unfair market

-

Monitoring policies: transaction fees and clearing time randomization

3.1 Bilevel optimization between the exchange and the strategic trader

3.2 Randomization without fees

3.3 Optimal transaction fees indexed on time to improve price impact for the trader

A. Appendix: Numerical Methods

A.1 Problem of a Strategic Seller

A.2 Appendix: Problem of the Regulator

B Appendix: Illustrate Remark 2.4

A.1 Problem of a Strategic Seller

A.2 Appendix: Problem of the Regulator

By Disintegration Theorem [Kallenberg (2002)],

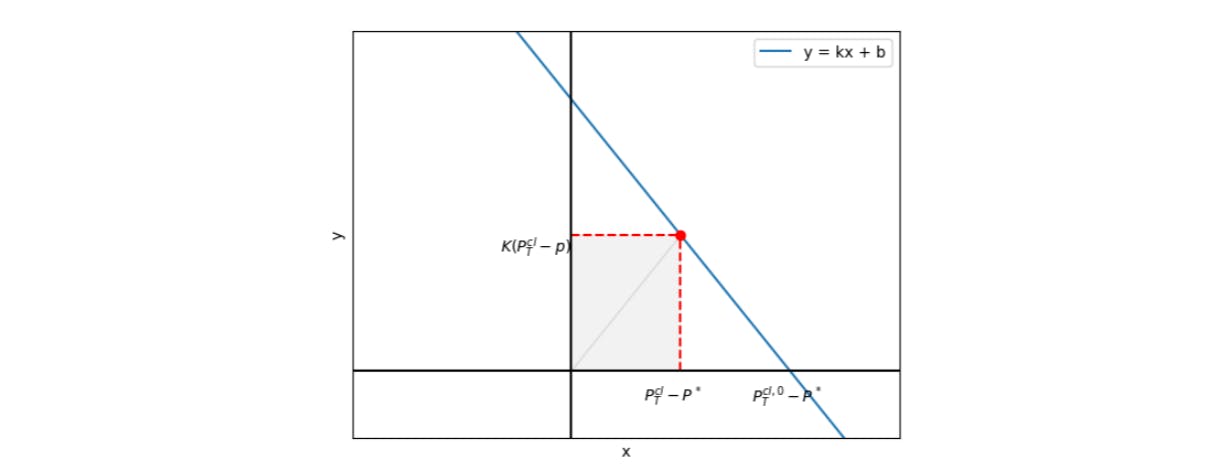

B Appendix: Illustrate Remark 2.4

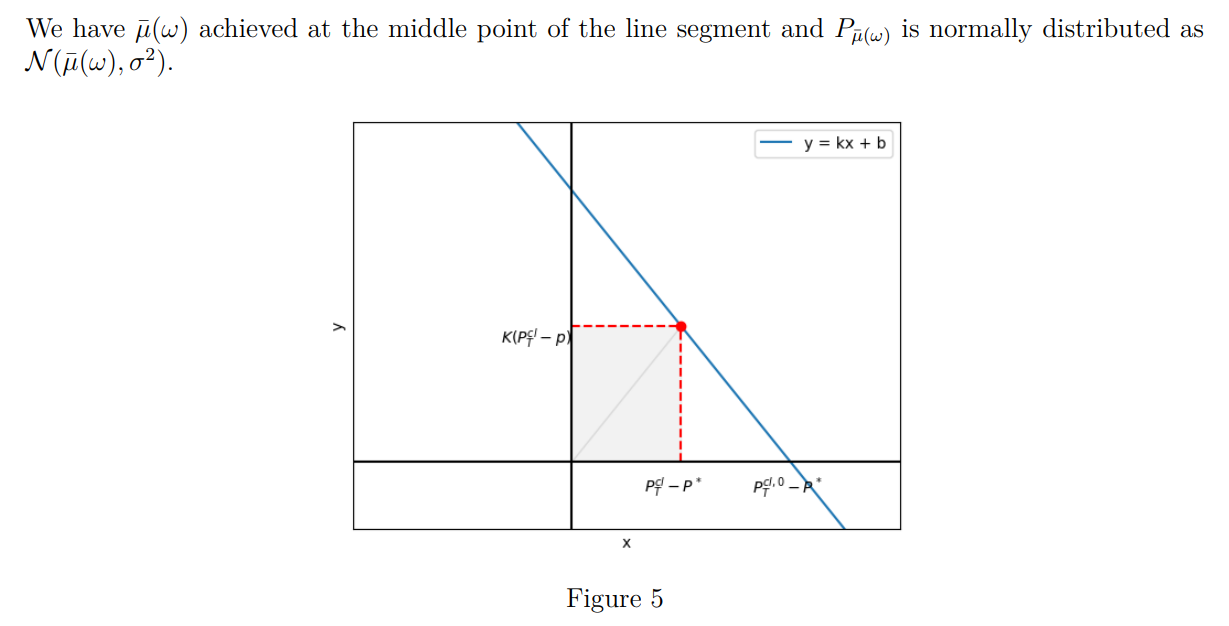

To better illustrate the proof, we draw a figure 5 of

For each point on the line, the x coordinate would be

and the y coordinate would be

where p is the price sent by the strategic seller. The shadow area is the trader’s gain.

References

[Abdi and Ranaldo (2017)] Abdi, F., and Ranaldo, A. (2017). A Simple Estimation of Bid-Ask Spreads from Daily Close, High, and Low Prices. The Review of Financial Studies, 30(12), 4437–4480.

[Alfonsi and Blanc (2016)] Alfonsi, A., and Blanc, P. (2016). Dynamic optimal execution in a mixedmarket-impact Hawkes price model. Finance and Stochastics, 20(1), 183–218.

[Aquilina et al. (2022)] Aquilina, M., Budish, E., and O’Neill, P. (2022). Quantifying the HighFrequency Trading “Arms Race.” The Quarterly Journal of Economics, 137(1), 493–564.

[Baldacci et al. (2023)] Baldacci, Bastien, Iuliia Manziuk, Mastrolia, Thibaut and Rosenbaum, Mathieu, (2023). Market making and incentives design in the presence of a dark pool: a Stackelberg actor–critic approach. Operations Research, 71(2):727-749.

[Brinkman and Wellman (2017)] Brinkman, E., and Wellman, M. P. (2017). Empirical Mechanism Design for Optimizing Clearing Interval in Frequent Call Markets. Proceedings of the 2017 ACM Conference on Economics and Computation, 205–221.

[Budish et al. (2015)] Budish, E., Cramton, and Shim, J. (2015). The High-Frequency Trading Arms Race: Frequent Batch Auctions as a Market Design Response. The Quarterly Journal of Economics, 130(4), 1547–1621.

[Canidiom and Fritsch (2024)] Canidiom A., and Fritsch, R. (2024). Arbitrageurs’ profits, LVR, and sandwich attacks: batch trading as an AMM design response. arXiv:2307.02074v5 [cs.DC].

[Derchu et al. (2020)] Derchu, J., Guillot, P., Mastrolia, T., and Rosenbaum, M. (2020). AHEAD : Ad Hoc Electronic Auction Design.

[Du and Zhu (2017)] Du, S., and Zhu, H. (2017). What is the Optimal Trading Frequency in Financial Markets? The Review of Economic Studies, 84(4 (301)), 1606–1651.

[Duffie and Zhu (2017)] Duffie, D., and Zhu, H. (2017). Size Discovery. The Review of Financial Studies, 30(4), 1095–1150.

[Fama (1970)] Fama, E. (1970). Efficient Capital Markets - Review Of Theory And Empirical Work. The Journal of Finance (New York), 25(2), 383–423.

[Farmer and Skouras (2012)] Farmer, D. and Skouras, S. (2012). Review of the benefits of a continuous market vs. randomised stop auctions and of alternative priority rules (policy options 7 and 12). Manuscript, Foresight, Government Office for Science, UK.

[Fricke and Gerig (2018)] Fricke, D., and Gerig, A. (2018). Too fast or too slow? Determining the optimal speed of financial markets. Quantitative Finance, 18(4), 519–532.

[Gayduk and Nadtochiy (2020)] Gayduk, R., and Nadtochiy, S. (2020). Control-Stopping Games for Market Microstructure and Beyond. Mathematics of Operations Research, 45(4), 1289–1317.

[Garbade and Silber (1979)] Garbade, Kenneth D and Silber, William L. (1979). Structural organization of secondary markets: Clearing frequency, dealer activity and liquidity risk The Journal of Finance, 34(3)577–593.

Goldberg and Tenorio (1997)] Goldberg, L., and Tenorio, R. (1997). Strategic trading in a two-sided foreign exchange auction. Journal of International Economics, 42(3–4), 299–326.

[Graf et al. (2024)] Graf, C., Kuppelwieser, T., and Wozabal, D. (2024). Frequent Auctions for Intraday Electricity Markets. The Energy Journal (Cambridge, Mass.), 45(1), 231–256.

[Griffin et al. (2010)] Griffin, J. M., Kelly, P. J., and Nardari, F. (2010). Do market efficiency measures yield correct inferences?: a comparison of developed and emerging markets. The Review of Financial Studies, 23(8), 3225–3277.

[Jegadeesh and Wu (2022)] Jegadeesh, N., and Wu, Y. (2022). Closing auctions: Nasdaq versus NYSE. Journal of Financial Economics, 143(3), 1120–1139.

[Jusselin et al. (2021)] Jusselin, P., Mastrolia, T., and Rosenbaum, M. (2021). Optimal Auction Duration: A Price Formation Viewpoint. Operations Research, 69(6), 1734–1745.

[Kalay et al. (2002)] Kalay, A., Wei, L., and Wohl, A. (2002). Continuous Trading or Call Auctions: Revealed Preferences of Investors at the Tel Aviv Stock Exchange. The Journal of Finance (New York), 57(1), 523–542.

Kallenberg (2002)] Kallenberg, O. (2002). Foundations of Modern Probability, second edition. Springer.

Liu and Chen (2020)] Liu, L., and Chen, Q. (2020). How to compare market efficiency? The Sharpe ratio based on the ARMA-GARCH forecast. Financial Innovation, 6(1), 1–21.

[Madhavan (1992)] Madhavan, A. (1992). Trading Mechanisms in Securities Markets. The Journal of Finance (New York), 47(2), 607–641.

[Malkiel (2003)] Malkiel, B. G. (2003). The Efficient Market Hypothesis and Its Critics. The Journal of Economic Perspectives, 17(1), 59–82.

[Melton (2017)] Melton, H. (2017). Market mechanism refinement on a continuous limit order book venue: a case study. SIGecom Exchanges, 16(1), 72–77.

[Shreve (2004)] Shreve, S.E. (2004). Stochastic Calculus for Finance II Continuous-Time Models. Springer 2004.

[Wah and Wellman (2013)] Wah, E., and Wellman, M. P. (2013). Latency arbitrage, market fragmentation, and efficiency: a two-market model. Proceedings of the Fourteenth ACM Conference on Electronic Commerce, 855–872.

[Wah et al. (2016)] Wah, E., Hurd, D., and Wellman, M. (2016). Strategic market choice: Frequent call markets vs. continuous double auctions for fast and slow traders. EAI Endorsed Transactions on Serious Games, 3(10), 1–10.

[West (1975)] West, R. R. (1975). On the Difference between Internal and External Market Efficiency. Financial Analysts Journal, 31(6), 30–34. https://doi.org/10.2469/faj.v31.n6.30

[Ye (2024)] Ye, L. (2024). Understanding the impacts of dark pools on price discovery. Journal of Financial Markets (Amsterdam, Netherlands), 68, 1–39.

[Ye (2011)] Ye, M. (2011). A Glimpse into the Dark: Price Formation, Transaction Cost and Market Share of the Crossing Network. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1521494

[Zhang and Ibikunle (2023)] Zhang, Z., and Ibikunle, G. (2023). The market quality effects of subsecond frequent batch auctions: Evidence from dark trading restrictions. International Review of Financial Analysis, 89, 102737.

[Zhu (2014)] Zhu, H. (2014). Do Dark Pools Harm Price Discovery? The Review of Financial Studies, 27(3), 747–789.

Authors:

(1) Thibaut Mastrolia, UC Berkeley, Department of Industrial Engineering and Operations Research (thibaut.mastrolia@berkeley.edu);

(2) Tianrui Xu, UC Berkeley, Department of Mathematics (tianrui.xu@berkeley.edu).

This paper is

[story continues]

tags