Authors:

FLORIAN GACH

SIMON HOCHGERNER

EVA KIENBACHER

GABRIEL SCHACHINGER

Table of Links

- Introduction

- Mean-field Libor market model

- Life insurance with profit participation

- Numerical ALM modeling

- Phenomenological assumptions and numerical evidence

- Estimation of future discretionary benefits

- Application to publicly available reporting data

- Conclusions

- Declarations

- References

Introduction

This paper is about the market consistent valuation of life insurance with profit participation. These types of products are characterized by a minimum guarantee rate and a profit declaration mechanism that lets the policyholder participate in the company’s net profits. The task of assigning a market consistent value to profit participating life insurance liabilities is non-trivial for many reasons, major challenges in designing an appropriate (numerical) model are:

• Profit is defined in terms of locally generally accepted accounting principles (local GAAP) which implies that assets have to be modelled not only with their market values but also with their book values.

• Profit declaration is not completely regulated by legislature, thus management rules have to be taken into account.

• The above points mean that any such model will consist of many subroutines, and there is no realistic hope for a closed formula solution for market consistent valuation. Hence an economic scenario generator (consisting, in particular, of a choice of an interest rate model) has to be fixed, and the valuation procedure depends on Monte Carlo methods.

• Not least, life insurance is a long term business, and an an appropriate model may have a projection horizon of 60 years, or even more. In the present work we consider the market consistent value to be defined in accordance with Solvency II which is the relevant regulation for insurers operating in the European Economic Area.

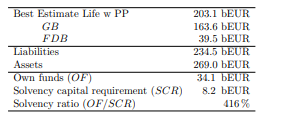

This means that the market consistent value is equal to the technical provisions as defined in [32, 33]. The technical provisions are a sum of a best estimate, BE, and a risk margin, RM. The best estimate, in turn, can be represented as a sum of guaranteed benefits and future discretionary benefits, BE = GB + F DB. All of these quantities are reporting items ([34]), meaning they are part of the Solvency II balance sheet. Moreover, these quantities are not only reported to national supervisory agencies but it is also mandatory to make these publicly available in the so-called solvency and financial conditions report (SFCR). A prototypical example consisting of partial balance sheet data is provided in Table 1. This table lists liabilities, of which GB and F DB, associated to profit participating business, are the two largest items, assets, and own funds, which are the difference between assets and liabilities. It is noteworthy that the future discretionary benefits are larger than the own funds, whence any error in F DB calculation translates to an even bigger error in the own funds, and further in the solvency ratio OF/SCR.

The goals of this paper are to, firstly, add to the general understanding of F DB-calculation, and secondly, provide tools for fast and reliable F DB-validation. In this regard the contributions are threefold:

(1) Advocating the mean-field Libor market model (MF-LMM) that was introduced in [7], we prove an existence and uniqueness result which allows us to use this model as an interest rate scenario generator. As shown in a numerical study in [7] the MF-LMM can be used to reduce the blow-up probability troubling the Libor market model, and is therefore well-suited for numerical valuation of long term guarantees. However, in [7] the authors were able to show existence and uniqueness of solutions only in a one-dimensional special case. In Section 1 we extend existence and uniqueness of MF-LMM to the multi-dimensional setting under rather general assumptions on the coefficients (Theorem 1.4). This result relies on a straightforward application of the L-derivative introduced by P.-L. Lions ([6]).

(2) Section 3 contains a description of a numerical asset-liability management (ALM) model that is capable of calculating a realistic F DB value in the Solvency II sense, and uses the MF-LMM as an interest rate scenario generator. The focus in this section is on a detailed description of modelled management rules. Some of the notation and concepts that are used in the numerical Section 3 are introduced in the previous Section 2 in a more abstract context

(3) In Section 4 we use the ALM model from Section 3 to provide numerical evidence for phenomenological assumptions concerning various quantities that are involved in the Monte Carlo based F DB-calculation.

These assumptions follow solely from heuristic ideas, and have no mathematical proofs, however the numerical evidence allows us to conclude that the assumptions are quite reliable – at least for the (rather wide) range of parameters that we have tested. These assumptions are used in Section 5 to derive algebraic formulas to estimate lower and upper bounds, LBd and UBd, for F DB. These bounds yield an estimate F DB \ = (LBd + UBd)/2 for F DB, which is useful when the potential error ε = (UBd − LBd)/2 is sufficiently small (e.g. compared to the market value of assets). This estimation is compared to the Monte-Carlo value of F DB in Table 2 using the numerical ALM and anonymized insurance data.

Finally, in Section 6.2 we compare the estimation result F DB \to publicly available F DB-figures, and show how to calculate F DB \ using only publicly available data. The estimation formulae for LBd and UBd are a continuation of the work begun in [19, 14] by two of the authors. Compared to [14] we have simplified the set of assumptions, improved and simplified the calculation of the lower bound, and, crucially, tested the assumptions on a numerical model (i.e. the ALM model of Section 3). Further background on market consistent valuation of life insurance products can be found in [26, 24, 9, 29, 17, 18, 2, 11, 12]). These works all address the interplay between asset and liability modelling but present strongly simplified versions of asset portfolios, in particular book values of assets are not modelled. Besides [19, 14], the case for a realistic representation of (asset) accounting principles is made in [8, 28, 1, 10].

The present paper follows this logic, and shows that accounting principles and management rules can be formulated in a manner amenable to mathematical analysis such that general formulae for lower and upper bounds of future discretionary benefits may be derived. As mentioned, these formulae depend on a number of assumptions. The overarching principle behind these assumptions is that the management strives to maximize the shareholder value while remaining a competitive player in the insurance market. This is reminiscent of an optimal control problem, and is formulated as such in Section 2.4. The logical next step would be to show that the assumptions of Section 4 define (or: are in an appropriate sense close to) the optimal strategy. However, this conclusion is outside the scope of this work, and is left open as a problem for the future.

This paper is available on arviv under CC by 4.0 Deed (Attribution 4.0 International) license

[story continues]

tags