Table of Links

Abstract, Acknowledgements, and Statements and Declarations

-

Background and Related Work

-

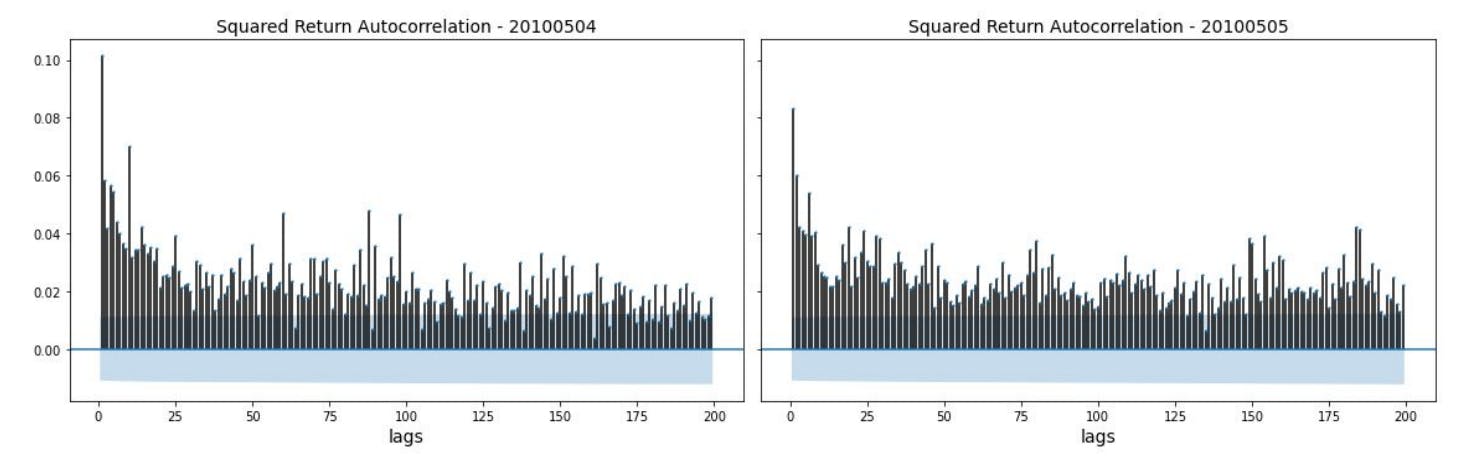

2010 Flash Crash Scenarios and 5.1 Simulating Historical Flash Crash

-

Mini Flash Crash Scenarios and 6.1 Introduction of Spiking Trader (ST)

-

Conclusion and Future Work

6.3 Conditions for Mini Flash Crash Scenarios

In Section 5.2 we explore how different conditions influence the amplitude of large flash crash events. Here we address the question that how those conditions influence the characteristics of mini flash crash events. Since the institutional trader is removed from the simulation, two conditions that are unrelated to the institutional trader are considered: market makers inventory limit and trading frequency of fundamental traders. Unlike the colossal flash crashes that happen extremely rarely, mini flash crashes occur more frequently in modern financial markets where high-frequency trading contributes to a vast portion of transactions. Consequently, the characteristic of mini flash crash events is twofold: the frequency for the occurrence of mini flash crash events and the crash severity once a mini flash crash occurs.

To explore the characteristics of mini flash crashes under different conditions, Monte Carlo simulation is carried out. For the purpose of consistency, the simulation also mimics the E-mini futures market on May 6th. The simulation spans from 8:00 to 12:30 on May 6th, 2010, excluding the afternoon trading session to reduce the influence of the large historical flash crash event. Except for the two model parameters that represent the two conditions that are of interest, other model parameters are assigned the same value as the calibration results and are strictly kept fixed12. For each parameter combination, which represents a specific condition, we run 60 simulations and calculate the average frequency for the occurrence of mini flash crash events and the average amplitude for the mini flash crash events.

The only remaining question to solve is how to count the mini flash crashes and how to measure the amplitude of a mini flash crash. Following Karvik et al. (2018), a mini flash crash is classified as a k standard deviation move in price, which reverses over a horizon that is less than certain time periods. The k has value 2, 3, 4 in our experiments. Note that because the spiking trader can create both upward and downward price shock, we also consider the upward "flare up" event as another form of mini flash crash[13]. Specifically, in our experiments a k-sd mini flash crash is defined to be the peak or trough price behaviour inside a 10-minute interval, where the price moves more than k standard deviations and then bounces back. The k standard deviation is calculated by reference to the minute-level return. Inspired by topography, the amplitude of the mini flash crash event is then defined to be the prominence of the peak or trough price trajectory. A specific method to calculate the prominence can be found in Virtanen et al. (2020).

We calculate the average number of the occurrence of mini flash crash and the average amplitude for the mini flash crash events under different conditions. The results are shown in Figure 12 and Figure 13.

Figure 12 presents how the average number of mini flash crashes per simulation changes when the inventory limit of market makers and trading frequency of fundamental traders vary. As shown in panel (a), increasing the inventory limit will decrease the average number of mini flash crashes in our simulation, indicating a lower frequency for the occurrence of mini flash crash events. This result is consistent with our intuition. The larger the inventory limit for market makers, the more selling pressure market makers are able to absorb. Thus the "hot-potato" effect is less probable to appear with a larger inventory limit for market makers, resulting in fewer mini flash crashes. As for the trading frequency of fundamental traders, however, the frequency of the occurrence for mini flash crash events barely changes when we vary the trading frequency parameter of fundamental traders. This is presented in panel (b) of Figure 12. One possible explanation is that mini flash crash events happen in an extremely short time scale and the amplitude is relatively small. Consequently, fundamental traders are hardly able to nor willing to participate during the course of the mini flash crash events.

Figure 13 presents how the average amplitude of mini flash crashes changes when the inventory limit of market makers and trading frequency of fundamental traders vary. As demonstrated by Panel (a) in Figure 13, the functional relationship between mini flash crash amplitude and market maker inventory limit is not monotonous. The average mini flash crash amplitude is an increasing function with regard to market maker inventory limit when the inventory limit is small, while it turns into a decreasing function when the market maker inventory limit is large enough. The logic here is very similar to the analysis in Section 5.2. While the market maker inventory limit is small, increasing the inventory limit will result in more selling pressure when the inventory limit is hit, leading to a larger crash amplitude. However, a large enough market maker inventory limit would absorb most shocks in the market, restricting the scale of the mini flash crash events. Moving on to panel (b) in Figure 13, we observe no obvious influence of fundamental traders trading frequency on the amplitude of mini flash crash events. This phenomenon once again demonstrates that fundamental traders hardly participate during the course of mini flash crash events.

Authors:

(1) Kang Gao, Department of Computing, Imperial College London, London SW7 2AZ, UK and Simudyne Limited, London EC3V 9DS, UK (kang.gao18@imperial.ac.uk);

(2) Perukrishnen Vytelingum, Simudyne Limited, London EC3V 9DS, UK;

(3) Stephen Weston, Department of Computing, Imperial College London, London SW7 2AZ, UK;

(4) Wayne Luk, Department of Computing, Imperial College London, London SW7 2AZ, UK;

(5) Ce Guo, Department of Computing, Imperial College London, London SW7 2AZ, UK.

This paper is available on arxiv under CC BY-NC-ND 4.0 DEED license.

[12] Due to no calibration results, the model parameters for the newly introduced spiking trader are given values heuristically.

[13] The definition for "flare up" and "flash crash" are symmetrical: "flare up" is a rapid price rise followed by a price drop.

[story continues]

tags